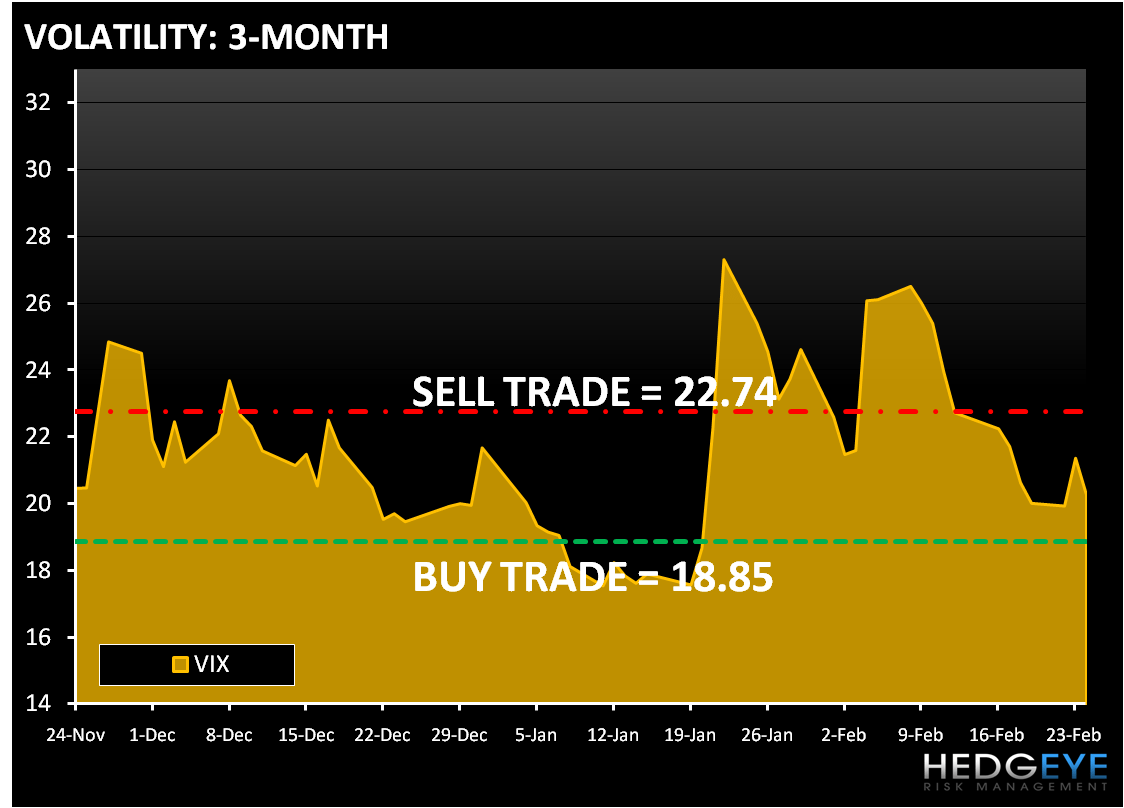

Thanks to the FED the S&P 500 finished higher by 0.97% on Wednesday. Fed Chairman Bernanke intimated that the “Piggy Bankers” will be feeding at the trough of free money for an extended period of time. This put the Financials (XLF) back on top of sector performance, rising 1.7%. Taken together, the need for extended period of low interest rates, China’s current tightening monetary policy and declining global consumer confidence present evidence to challenge an extended rally.

The pullback in the dollar following yesterday's spike also offered some support for the stocks, but not the RECOVERY trade. Two of the three worst performing sectors yesterday were Materials (XLB) and Energy (XLE). The Hedgeye Risk Management models have levels for the Dollar Index (DXY) at – buy Trade (79.60) and sell Trade (81.16).

On the macro calendar, new home sales plunged 11.2% month-to-month to a 309,000 unit annualized pace in January, marking a record low. Sales were weak across much of the country last month, with a 35.1% decline in Northeast leading the way. The decline in sales pushed the month’s supply of new homes to 9.1 from 8.0 in December, while the inventory of new homes for sale rose 0.4%, the first increase since April of 2007. Not surprisingly, homebuilders were weaker on the news, with notable decliners including RYL, DHI and PHM. We remain short TOL and are concerned about housing going into 2Q10.

The banks led the market higher yesterday, with the Bank Index (BKX) up 2.28% after declining 2.36% the day before. With little hard news, the FED is behind the rally. Money-center and Large-cap regional’s were among the standouts in the group with C, BAC, KEY, STI and MI leading the way. We are currently long the XLF.

The Technology (XLK) continues to be the worst performing sector year-to-date, but slightly outperformed yesterday. Semis were a key driver of the outperformance yesterday, with the SOX up 1.9% after falling 2.8% on Tuesday. Yesterday, ADSK was up 8.7% following its earnings release. We are currently long the XLK.

Consumer Discretionary (XLY) is the best performing sector over the past month and continued its strong relative performance yesterday. The strength is centered in Retail, with the S&P Retail Index up 2% yesterday and is up seven of the last eight days. The sector continues to benefit from a strong earnings season.

On the MACRO calendar today we will see initial Jobless Claims and January Durable Goods, while Fed Chair Bernanke gives a second day of pandering before the Senate. As of the time of writing equity futures are trading below fair value. As we look at today’s set up the range for the S&P 500 is 26 points or downside (1,094) and upside (1,120).

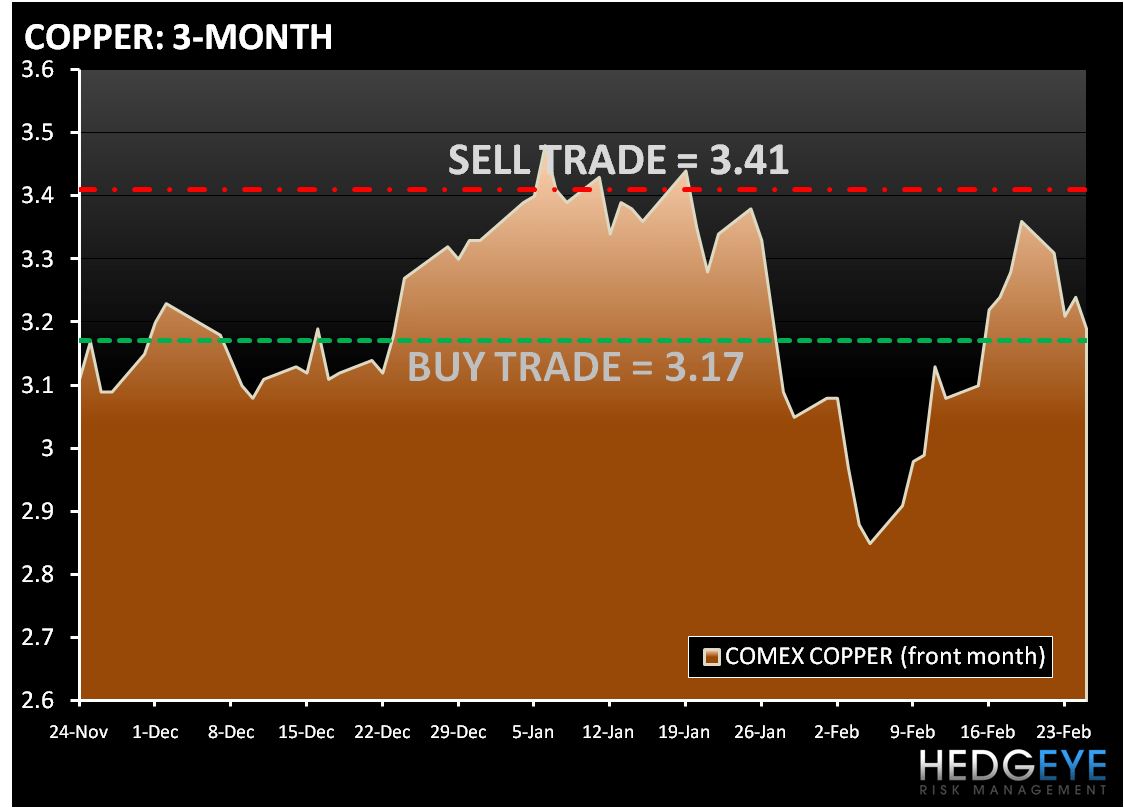

Copper closed up 0.5% yesterday, but is looking lower in early trading today. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.17) and Sell Trade (3.41).

In early trading gold is trading down to the lowest price in the past two weeks. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,087) and Sell Trade (1,117).

Oil is trading down on a higher dollar and a lack of momentum behind the RECOVERY trade. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (77.09) and Sell Trade (82.10).

Howard Penney

Managing Director