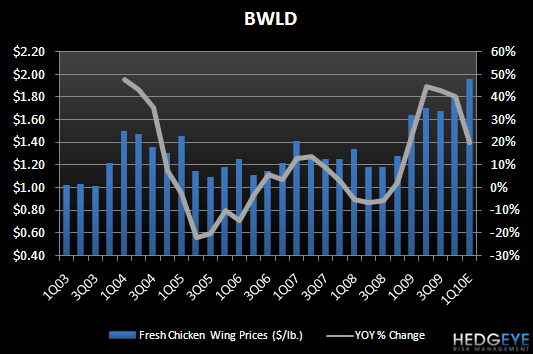

Sanderson Farms stated today on its earnings call that the 36.4% increase in fiscal 1Q10 average jumbo wing prices was driven largely by continued strong demand for wings in both the food service and retail grocery channels. BWLD’s same-store sales slowed throughout 4Q09 and restaurant level margin declined 90 bps YOY. Sanderson Farms’ comment does not bode well for BWLD from a top-line or margin standpoint.

Increased Competition:

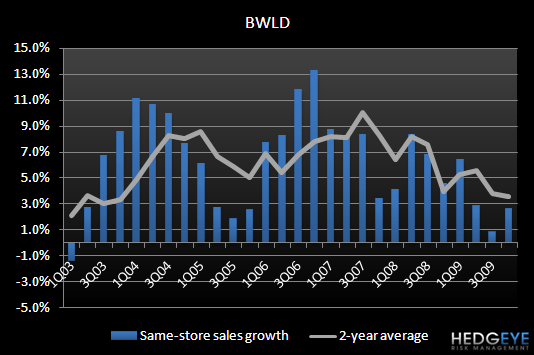

BWLD’s 4Q09 same-store sales came in +2.6% after being up nearly 6% in the first four weeks of the quarter, implying a significant slowdown in November and December. Comparable store sales trends in the first six weeks of 1Q10 are only up 0.5%. The company is lapping a +8% number from the same six week period in the prior year, but regardless, the +0.5% is soft relative to expectations. Management attributed the soft start to the quarter to weather.

Sanderson Farms does not appear to be seeing this same fall off in wing demand, which could signal that BWLD is losing share. BWLD did comment that it will be promoting a Boneless Wing Thursday during the first quarter, in addition to its long-standing Wing Tuesday, in order to stay competitive as the value equation is top-priority for its guests.

Increasing Costs:

During 4Q09, the cost of traditional wings increased 40% YOY to $1.78 per pound. Through the first two months of the first quarter, this cost has moved up to $1.95 per pound. Assuming this $1.95 level for the entire first quarter implies a nearly 20% increase YOY (wing prices started to move relatively higher in 1Q09). Management guided to 50 bps of YOY cost of sales pressure in 1Q10. It is important to remember that traditional wings accounted for 22% of BWLD’s restaurant sales in 4Q09, up 100 bps from the prior year.

When asked specifically about its full-year outlook on traditional wing prices, management stated, “We always would like to think there's an opportunity for wing prices to move lower. The average of the first five months was $1.95. We did see it go up from December through just shortly before Super Bowl and then there actually was a little bit of weakness in the market about that time, which typically you don't see. So I mean we'll still watch it and I'm sure everybody else will as we go through the month of February. But knock on wood, you'd like to think that it will start to trail off here as we get into the second quarter.”

Sanderson Farm’s comments about continued strong wing demand will have the biggest impact on the BWLD story from the cost side. If demand continues to be strong, it is unlikely wing prices will start to trail off during the second quarter, putting increased pressure on BWLD’s margins.

Howard Penney

Managing Director