We think Feb table revs will be at least HK$11BN, up at least 54% YoY and down 15% or less sequentially. Market share gainers should be SJM and Wynn while LVS and MGM probably lost share.

After a slow start to the month, the Chinese New Year celebration kicked February into high gear. Based on HK$9BN in table revenues through 2/21/10, we think the month could exceed HK$11BN.

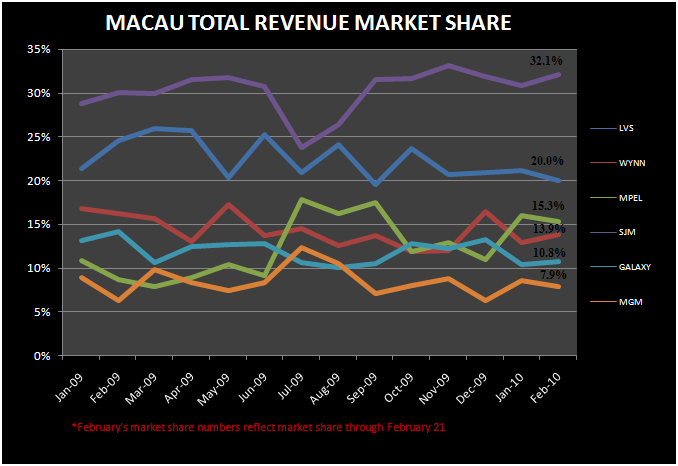

Despite a Rolling Chip hold percentage below significantly below January, both Wynn Macau and SJM managed to increase market share through the Chinese New Year Celebration by about 100bps each from January. LVS and MGM gave up about 100bps of share each from January.

The following chart shows the market share trends by company including February through 2/21/10: