The guest commentary below was written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.

|

This is the first of three essays motivated by John Williams’ estimate of the natural rate of interest. Williams, the President of the Federal Reserve Bank of San Francisco, has been picked to replace William Dudley as the President of the Federal Reserve Bank of New York. He is also an advocate of using a statistical measure of the natural rate of interest (r-star) to determine the stance of monetary policy. |

Specifically, Williams believes that policy is expansionary (easy) if the short-term real rate is below r-star and contractionary (tight) if the real short-term rate is above r-star. In this essay, I show that there is nothing natural about Williams’ estimate of the natural rate of interest. The behavior of his r-star is due entirely to the monetary policy of the Federal Open Market Committee (FOMC).

My next essay will show that Williams’ estimate of the natural rate suggests the FOMC’s monetary policy of the last nearly 30 years has hindered rather than promoted economic growth and employment. My third essay will show that even if, for some reason, you like Williams’ estimate of the natural rate, his estimate is so imprecise that it is useless as a guide for policy.

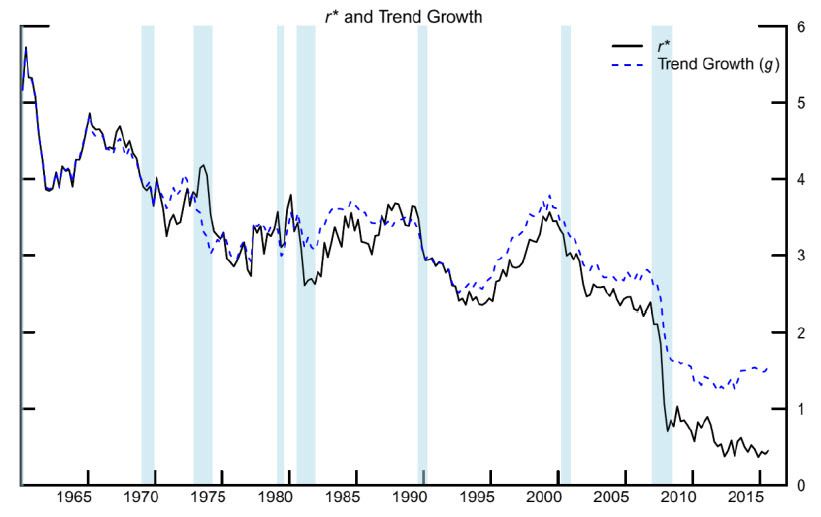

The natural rate of interest is a concept suggested by Swedish economist Knut Wicksell in 1898. Wicksell suggested, “there is a certain rate of interest on loans which is neutral in respect to commodity prices, and tends neither to raise nor to lower them.” The figure below, from Holston, Laubach, and Williams, shows Williams’ r-star.

The figure also shows Williams’ estimate of the trend growth rate of potential output. Williams’ estimate of the trend growth of potential output is essentially a smoothed short-run trend in actual output. This is shown in the figure below which shows the year-over-year growth rate of real GDP quarterly and Williams’ estimate of the trend growth of potential output. The figure shows that Williams’ estimation technique does little more than produce a smooth trend in actual output growth by significantly dampening the cycles in actual output growth. By the way, this is true for all estimates of potential output as I point out in The Myth of Potential Output.

Note that Williams’ r-star tracks trend output growth closely. That’s because Williams’ defines it this way. His models allows r-star to deviate from trend output growth because of “random shocks” that have permanent effects. Consequently, a string of positive or negative shocks can cause r-star to wander above or below trend growth. The figure shows that a string of negative shocks caused r-star to be persistently below trend growth of output since the early 1990s.

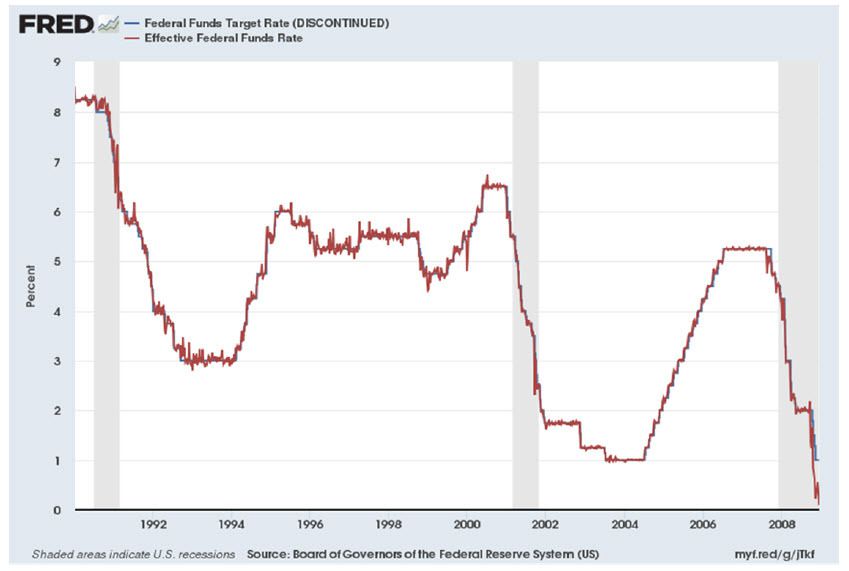

“What caused this remarkable string of negative shocks to r-star?” The FOMC! The FOMC is responsible for the string of “negative shocks” found because Williams used the federal funds rate as his “short-term lending rate.” The FOMC began using the federal funds rate as its policy instrument in the late 1980s. Since then, the federal funds rate has tracked the FOMC’s target closely. This is shown in the figure below, which shows the FOMC’s federal funds rate target and the federal funds rate from January 1990 to December 2008. As the FOMC became more open about targeting the funds rate and increasingly explicit about its funds rate target, the federal funds rate tracked the FOMC’s target more closely. The FOMC began announcing the specific target for the federal funds rate in June 1999. Prior to that date, the target was inferred. After December 2008, the FOMC began controlling the federal funds rate using interest paid on excess reserves (IOER) and executing reverse repurchase agreements in U.S. Treasuries. Since then, the federal funds rate has moved with FOMC changes in the IOER. Consequently, the funds rate was determined by the FOMC during this period.

The fact that the FOMC controlled the behavior of the federal funds rate since 1990 means that the decline of rstar below Williams’ estimate of the trend in the growth of real GDP is due entirely to the FOMC: The FOMC is the source of the string of negative “shocks” that caused r-star to be persistently below Williams’ estimate of trend output growth. Hence, there is nothing natural about Williams’ estimate of the natural rate. Its behavior was solely and completely determined by the FOMC’s monetary policy over the past nearly 30 years.

My next essay shows that it is possible, I believe likely, that the FOMC’s interest rate policy contributed to the slow growth in output and employment that occurred over this period.