The S&P 500 finished modestly lower (-0.1%) yesterday on extremely light volume and slightly negative breadth. The lack of volume is likely a result of the lack of earnings, economic, and political news. On the global MACRO front, the lack of data suggests that that the MACRO remains a slight headwind, although the RISK AVERSION trade continues its current momentum.

Overall the markets continue to shrug off the potential negative impact of the recent discount rate hike on the favorable liquidity backdrop. Yesterday, from a sector performances standpoint, most sectors with outsized exposure to the risk/recovery trade put in mixed performances.

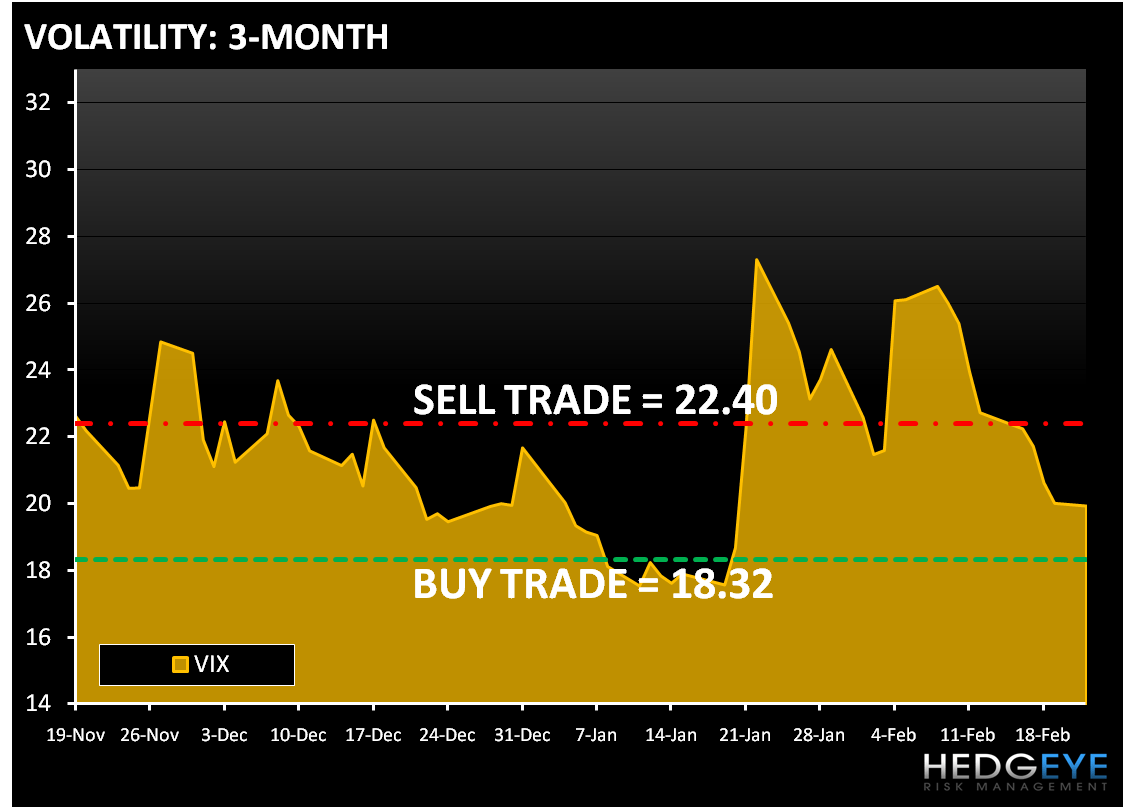

Confirming the risk aversion trade the Russell 2000 finished higher for a ninth straight day and the VIX is broken on all three durations - TRADE, TREND and TAIL. Now having 6 of 9 sectors positive on TRADE, a bearish VIX really does make sense from a contrarian perspective. With bearish sentiment mounting and the S&P500 still down YTD (plus our bearish calls on China and US Treasury bonds freaking people out alongside the sovereign debt worries), the VIX looks like it wants to suck back down to the mid-teens. The VIX remains positive on TREND at 22.43. The Hedgeye Risk Management models have the following levels for VIX – buy Trade (18.32) and Sell Trade (22.40).

The best performing sector yesterday was the Financials (XLF), with upside largely a function of the continued strength in the banking group, with the BKX +1.9%, and up for a third straight session. There did not seem to be anything specific behind the outperformance, other than some sell-side upgrades in the larger-cap regional space. The sector also benefited from the high-profile hedge fund buying note in Barron’s over the weekend.

Heading into the retail earnings season, the Consumer Discretionary also outperformed yesterday. Overall, retail held up a bit better than the broader market with the S&P Retail Index unchanged, after finishing higher over the past six days.

As I mentioned above the RECOVERY trade took it on the chin as Energy (XLE) and Materials (XLB) were 2 of the three worst performing sectors yesterday. Within Energy, E&P stocks were among the worst performing sub-indices. The oil services group also finished lower on the day, but M&A was in a highlight after SII agreed to be acquired by SLB.

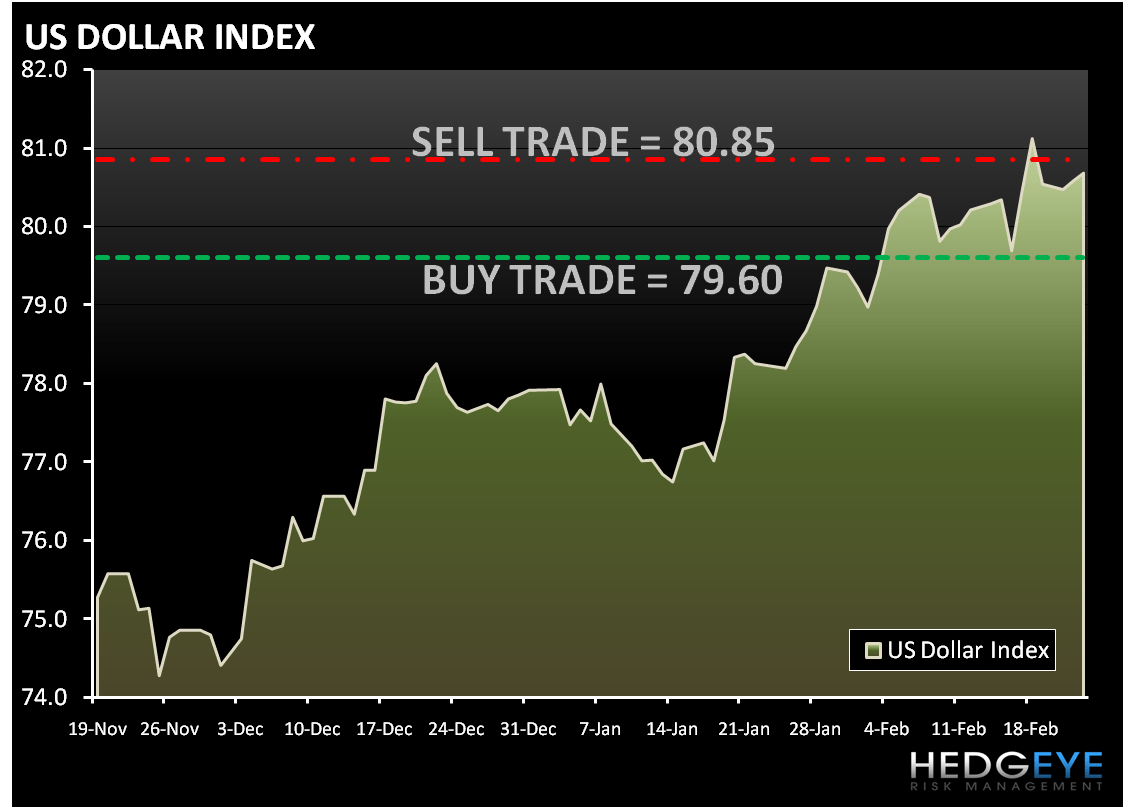

Equity futures are trading above fair value following yesterday's slow day, as the market awaits further news on Greece's forthcoming bond issue and tomorrow's testimony to Congress by Fed Chairman Bernanke. This has the Dollar index up by nearly 0.3% in early trading. The Hedgeye Risk Management models have levels for DXY at – buy Trade (79.60) and sell Trade (80.85).

As we look at today’s set up the range for the S&P 500 is 23 points or 0.9% (1,099) downside and 1.2% (1,122) upside.

In early trading, copper is higher in London on a positive demand outlook. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.17) and Sell Trade (3.46).

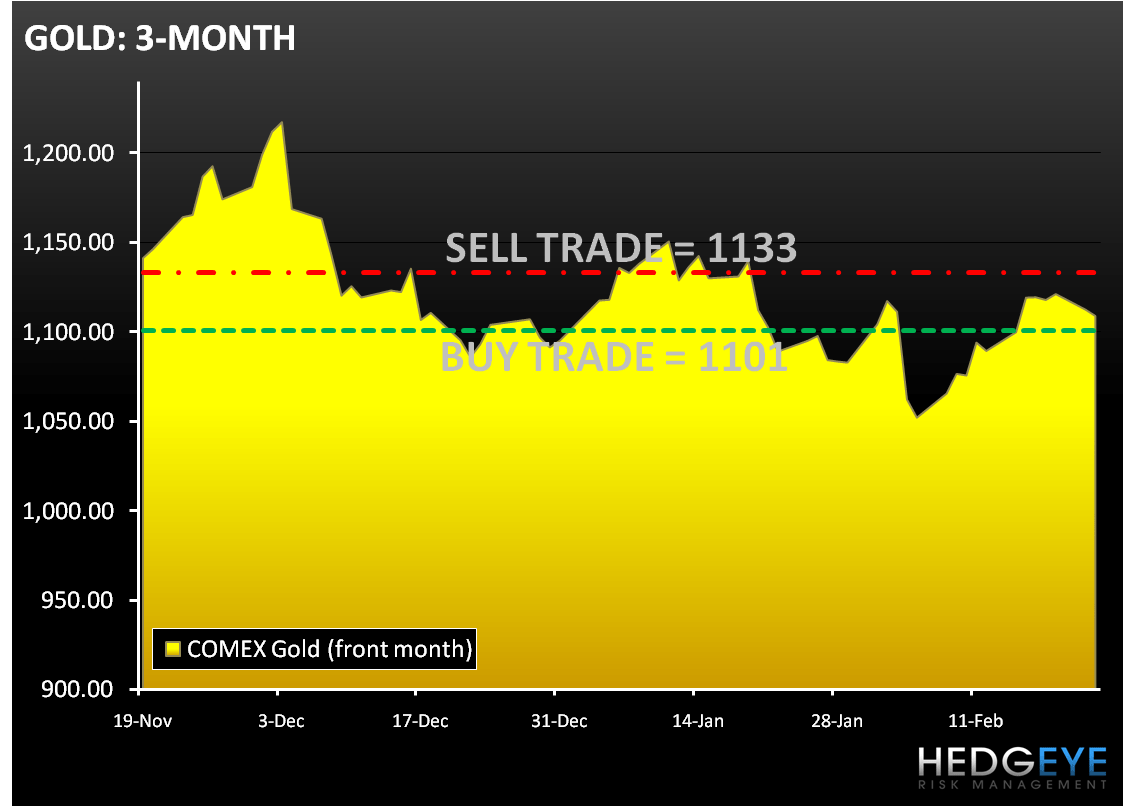

In early trading gold fell in London on a stronger dollar. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,101) and Sell Trade (1,133).

Oil is trading down for the first time is six days on increased supply. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (77.08) and Sell Trade (81.83).

Howard Penney

Managing Director