I am getting a lot of questions on the subtle shift I made this morning in my US stock market view. Subtle is as subtle does but, on the margin, it matters…

On this morning’s market weakness I made the following moves in US Equities:

1. Covered my short position in the SP500 (SPY)

2. Covered my short position in US Energy (XLE)

3. Bought a long position in US Technology (XLK)

This doesn’t make me the bull, but it definitely signals my moving from bearish on the SP500 to neutral. On the margin, that’s a bullish shift.

I can make this move without changing my view on our Top 3 Macro Themes in Global Macro:

1. Buck Breakout (bullish on the US Dollar)

2. Rate Run-up (bearish on US Treasuries)

3. Chinese Ox in a Box (bearish on China)

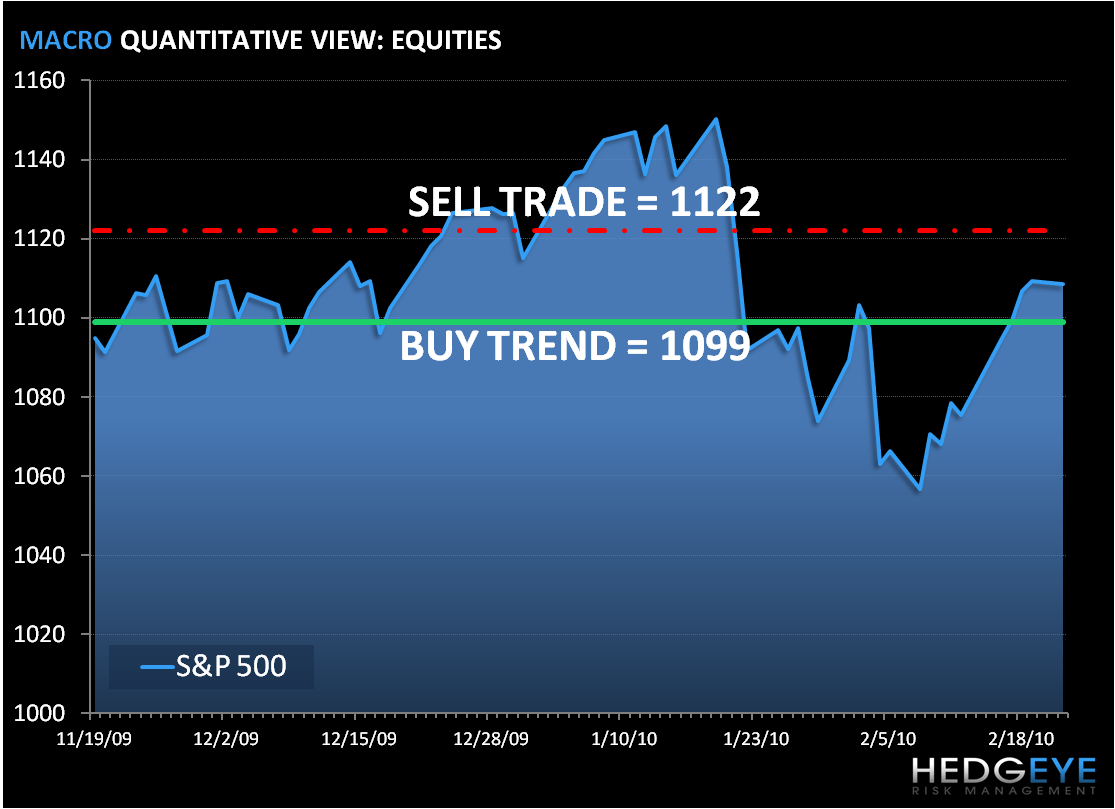

I have been managing risk around my US Equity long and short positions throughout Q1 as my conviction bobs and weaves in and around the SP500’s intermediate term TREND line (in the chart below at 1099). While price momentum is only one factor in my multi-factor risk management model, it is weighted heavily alongside volume and volatility factors.

As the VIX breaks down further today (no support to $18.11), the probability heightens that we’ll see a near term upside test of the dotted red line in the chart below (1122). I have added 3% to the US Equity side of our Asset Allocation Model so that I can capitalize on some of this potential upside. Remember, risk management works both ways. Markets can work higher when consensus is leaning too bearish.

KM

Keith R. McCullough

Chief Executive Officer