The Winter Olympics is traditionally a big blown-out non-event in the world of sports marketing. Yes, brands make noise about their innovations and new product. But let’s face some facts, most people don’t walk the Streets wearing those luge unitards.

Under Armour is the exception as it relates to brand impact, however. Why? Three of the many holes in its portfolio it has yet to fill are 1) International, 2) Higher-end cold weather outerwear, and 3) Women. This event gave a lay-up opportunity to show the world that it’s not just a US football brand, and UA soared over a few defenders’ heads and jammed it.

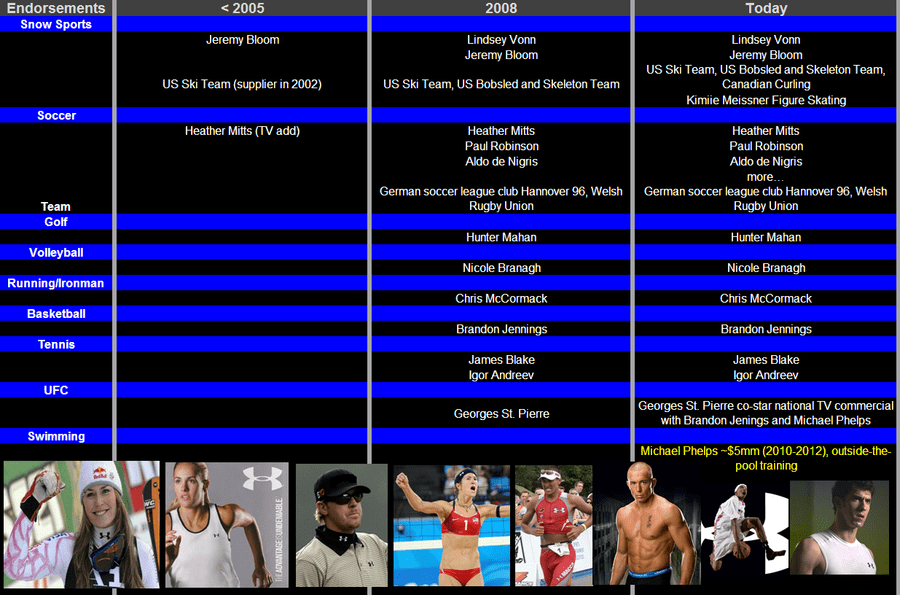

Under Armour is taking full advantage of the 2010 Vancouver Winter Olympics through its official, unofficial, and individual sponsorships. The ground work was laid in 2002 when UA joined the U.S. Ski Team as a supplier and has blossomed into high profile coverage through official sponsorships of the U.S. Freestyle Ski Team (aerials, moguls, and ski cross), U.S. Bobsled Team, U.S. Skeleton Team, and the Canadian Curling Teams (as an FYI, Curling in Canada is second only to Hockey as a National pastime).

UA’s unofficial sponsorship can be seen underneath the outerwear with its performance base layers that are worn by most of the US athletes on the slopes. If you’re watching the games, chances are that you noticed. I’d argue that this trumps individual sponsorships in this instance. But Under Armour has also invested around cross-over athletes like Lindsey Vonn. UA compared Vonn’s potential at the Winter Olympics of winning 5 gold medals to Michael Phelps amazing accomplishments of 8 gold medals at the 2008 Summer Games. That’s a bit of a stretch, but heck, UA endorsed Phelps last week last week, so even if they are wrong that still have the Big Man.

Why Vonn and Phelps? In the end, the athletes need to either win, but really, they need to capture the hearts and minds of viewers around the world. One of the more powerful ways to do this is by partnering with athletes with broad crossover appeal. By ‘crossover appeal’ I mean Vonn making it into the swimsuit issue of Sports Illustrated (see below), and Phelps endorsing UA’s product for purposes nothing having to do with water – but simply the training apparel/footwear to help him build form. This is also akin to someone like Maria Sharapova for Nike (who has been on the cover of SI and Vogue in the same month), where no one can justify the investment on tennis sales alone, but across a much broader product set.

Under Armour downplayed the impact of the Winter Olympics on their 4Q call and only mentioned it as a small opportunity to be seen as a global player. Our sense is that they fully baked this in to their SG&A guidance, but lowballed revenue opportunity as well as the longer-term brand implications.

See stats below for the market opportunity for UA in the Ski/Snowboard outerwear market. Its current share is sitting between 1-2%. Yes, that’s almost as small as its footwear market share. Big opportunity.

On a related note…Under Armour won the seventh Doc DesRoches Award (other winners include Rossignol, Spyder, and SmartWool) for recognition as an SIA member and U.S. Ski Team supplier for its promotion of the Team's brand and athletes. Under Armour was acknowledged for the national print and TV campaign around World Champion Lindsey Vonn. Check out the commercial: http://www.theskichannel.com/news/skinews/20100131/Lindsey-Vonn-Under-Armour-commercial-wins-Doc-DesRoches-Award-at-SIA.

Zach Brown

Analyt

Hedgeye Retail