This is a seasonally weak quarter, and we’re likely to see EPS +/- 5%. We’re modeling the latter. Would not fall out of my chair to see see better revs due to earnings opacity from acquisitions and FX benefit. Organic sales, however, should be down by lsd. We’ll likely see a full point revenue drag due to the Bon Ton filing, another 1% due to losing the Just My Size contract at WMT, and note that KSS been talking down the quarter due to weather (CRI just supported that in its print). Both of these factors are new since the last earnings report. Cotton costs are stealthily grinding higher -- up 25% since the trough 9 months ago (and costs take 9-12 months to flow from the balance sheet through to the P&L due to FIFO accounting). So back half we lap an acquisition, rely more on organic revenue which should be down 2-3%, and see GM pressure due to cotton and increased competitive pressure from GIL and upstart competitors. Any way I look at this model, I view 2H expectations as completely undoable. We’re 15% below consensus in the back half.

This stock has acted like death – underperforming by 20% since the last print, and there is absolutely no incentive for HBI to take down guidance this quarter given it has its seasonally strongest quarters to come and it will keep hope alive – ie a balloon underwater while it stretches to hit its targets – not unlike what happened in 4Q16). I’m mildly concerned that the SI% is sitting at peak 17%, but the stock is hitting lower highs and lower lows, and I’m comfortably short it even at a 4-year low. The good thing about 4-year lows is that you could have made the ’12-month low’ call in the past three year and been wrong every time).

I haven’t seen a company so stuck between a rock and a hard place since Jones Apparel Group a decade ago. That didn’t end well, and the company was broken up into obscurity. But the difference here is that HBI is a vertically integrated company with little take out risk. Utilization is sitting at 95% (unsustainable), margins are near peak (14%), and it has no more balance sheet leverage upside to conduct meaningful acquisitions. That means no more special charges, and a 500bp reversion to peer margins of 8-9%. Then the space sees another 200-300bp hit due to secular/structural challenges.

I’ve said it before and I’ll say it again. This should prove to be the best short of my career (until I find a better ‘best short of my career’). I’m not overstaying my welcome – despite the 36% hit to the stock since our call (underperformaed the S&P by 64%). Unless McLean’s model is completely off (usually not the case – his track record on this one is solid), consensus EPS and cash flow assumptions are too high by 12% this year (15-20% in 2H), 35-40% next year, and nearly 60% by 2020. There’s a clear path to a dividend cut, and ultimately a covenant breach at a time when the stock is trading at 13x EBITDA. When revalued on our earnings, CFFO and FCF numbers, I get to a $5-$6 stock.

-- McGough

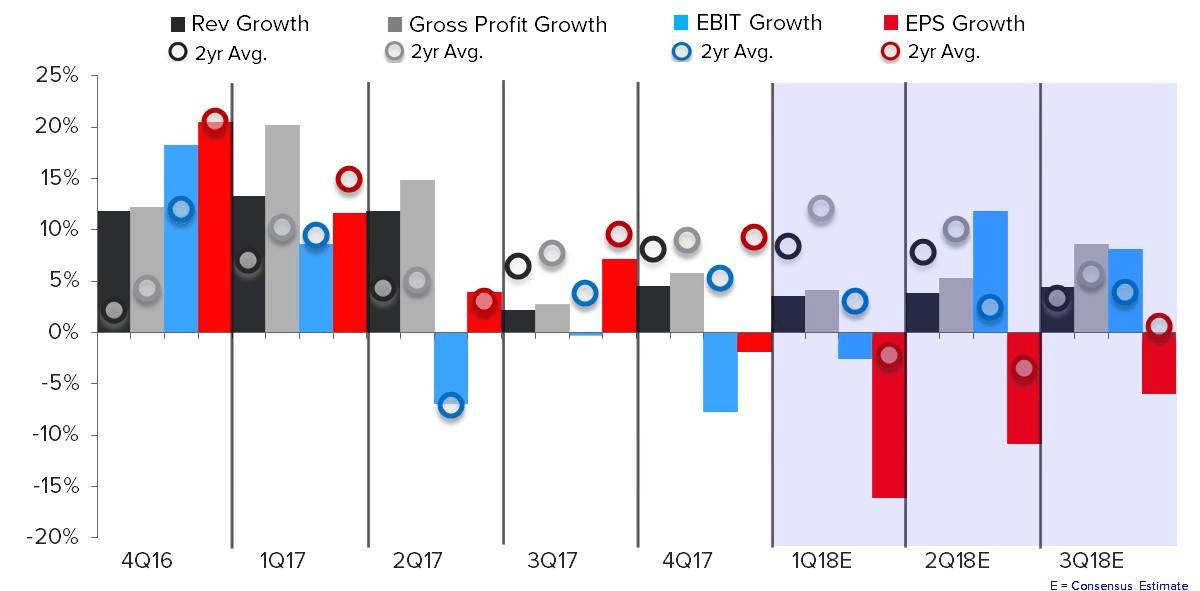

KEY CHART: Earnings growth hitting lower highs and lower lows. That should continue. It’s also when the sandbag game fails to work.

McLean’s Model Tear Down

Revenue:

Acquisitions

- The magic acquisition (just because the deal price/multiple implies a 28% EBITDA margin) Bra’s & Things closed 2/13/18 so its contributing about half a quarter of revenue. That should be about $19mm or ~4pts of growth for the international segment.

- Alternative apparel closed 10/13/17 and should add about $17mm, or a 5pt boost to the Activewear segment.

Champion

- Champion Makes up about 16% of sales. The brand has been growing in the high teens, but Activewear has not been reflecting that entire upside, implying cannibalization or weakness in other brands.

- We expect to see a mid to low teens growth rate in 1Q, but believe the brand is likely to slow later in the year against tougher compares and over-distribution in mid to late 2017.

Innerwear Pressure

- 2 notable announcements should mean increased pressure on HBI’s innerwear growth, which has already been in decline.

- WMT announced that the Just My Size brand would be replace within its doors. That should be about a point headwind to HBI’s total topline or about 3pts pressure on the Innerwear Segment.

- Then the Bon-Ton store closings are another headwind. Reduced sales to BONT was likely in HBI’s plan, but we doubt it planned a reduction to zero. The total lost sales should be about another point headwind to total revenue distributed between Innerwear and Activewear.

- These rev losses may not turn up in 1Q, but will be a drag on top line for 2Q and beyond.

- We still expect share loss in the core basics business to the likes of GIL and private label within mass channel.

FX

- FX is a big help in 1H for HBI. This quarter should be the peak benefit with total topline to see a 250-300bps help from FX.

- That’s about 8-9pts of help for the international segment, on top of the 4pts from Bra’s & Things.

- With the tailwinds, International should grow at least low DD. If it doesn’t, something is up.

Australia

- HBI has the highest exposure to Australia as any US based company we track, as HBI is approaching a low teens % of sales from down under.

- Hedgeye Housing/Financials are very bearish on the housing market and banks of Australia as it’s at the peak of a housing bubble starting to see some cracks.

- We applaud HBI for diversifying away from a US core business that is structurally set up for long term share loss, however we don’t think paying big multiples to increase exposure to Australia is a smart play given the macro set-up.

- The threat here is slow moving, but we have high confidence it will be a significant negative event for HBI fundamentals in the next 2-3 years.

Gross Margin:

- HBI will get some mix benefit with newly acquired businesses being essentially all retail. It should be 25-50bps.

- Cotton prices should be a headwind. HBI signaled the increases of 2016/17 wouldn’t hit 'til this year, now it should start flowing through. Cotton prices have risen higher recently, so there is risk to margin in guidance as well as we don’t think retail will allow HBI to pass on rising input costs.

- FX should be a help to margin this quarter, we noted about the 250-300bps help to total topline.

- Company lapping the Nanjing plan closure this Q. There may be some higher margin inventory still in the pipe, but any utilization margin help HBI saw should be fading in the first half of this year.

SG&A:

- We expect some SG&A deleverage in 1Q, about 50bps. The acquired businesses should come with high GM but also higher SG&A. Also, the FX tailwind on the topline is a headwind on the SG&A line.

- Expect some big one time charges as usual.

Cashflow:

- Capex is guided up about 15% yy, to 1.5% of sales while HBI is still acquiring businesses ($400mm worth so far this year).

- Working capital will likely look good as HBI will use purchase accounting to boost cash flow from its latest deals.

Segments:

- Expect a re-alignment of segments without historicals as we have seen that in the last 2 first quarter earnings releases.