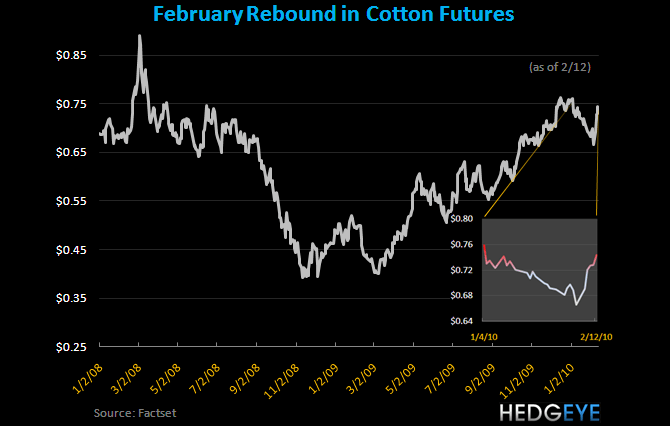

Following a breather in early 2010, cotton futures reversed sharply last week up $0.08/lb or 12%. Futures prices are now back up over $0.74/lb, nearing the highs of December (~$0.76/lb.). On recent earnings calls, both Hanesbrands and Gildan noted that their cotton costs were either locked in or hedged through 3Q. However, each of these manufacturers had a different view on what cotton costs may mean for pricing.

While GIL noted that its plan was to not to pass through cost increases, HBI suggested that at a mid-$0.70 range in cotton prices gives the company an option to pass through increases given its success in passing on costs in the past. One thing to note is that HBI still has the benefit of using factory consolidation savings as an offensive weapon to offset commodity costs and by offering a better value proposition to consumers. GIL is out of gas. In addition, with GIL far more exposed to cotton than HBI (~33% of COGS for GIL vs. ~6% for HBI - or ~$0.13 in EPS for each 5 cent move in cotton), the negative implications for rising cotton prices are considerably greater for GIL. Recall that favorable y/y cotton and energy costs accounted for a 950bps increase in gross margins in Q1 for GIL. As a point of reference cotton contributed only 180bps to HBI’s most recent quarter. Needless to say, this will be one of many topics of discussion at HBI’s analyst day next week, which we’ll be commenting on real-time.

The bottom-line here is that while the setup continues to look favorable for both companies over the near-term, either a rebound in consumer demand or a decline in commodity prices will be needed 2-3 quarters out to sustain intermediate-term outperformance – neither of which were supported over the past week.