Editor's Note: Click the play button to listen to a recently released conversation between hedge fund manager and MacroVoices podcast host Erik Townsend and Hedgeye Senior Macro analyst Darius Dale.

Erik and Darius discuss our Macro team’s top 3 themes for 2Q 2018: USA #Peak Cycle; Global Divergences, Reiterated; and U.S. Dollar #Bottoming?. Below is an excerpt transcribed from the conversation.

* * *

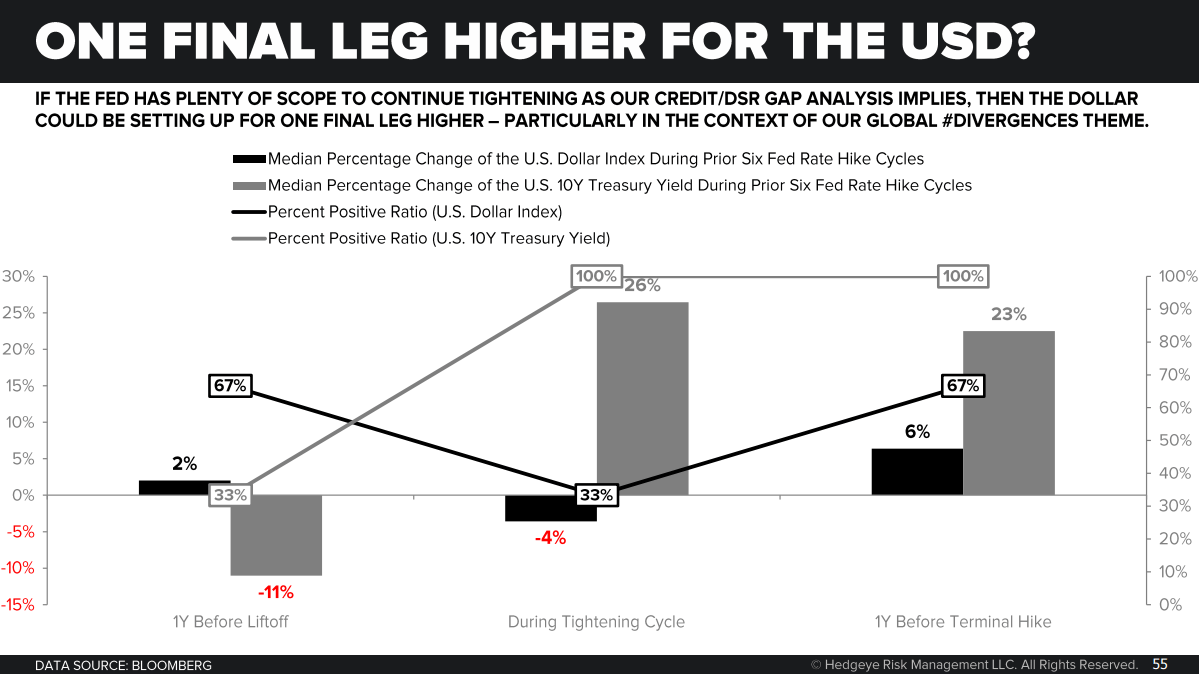

Erik: I noticed that you used the words “one final leg higher” for the US dollar on Slide 55. Is that a prediction that it’s all over for the dollar after that? That this really is the final leg? Or do you just mean a final leg this year? What are you referring to there?

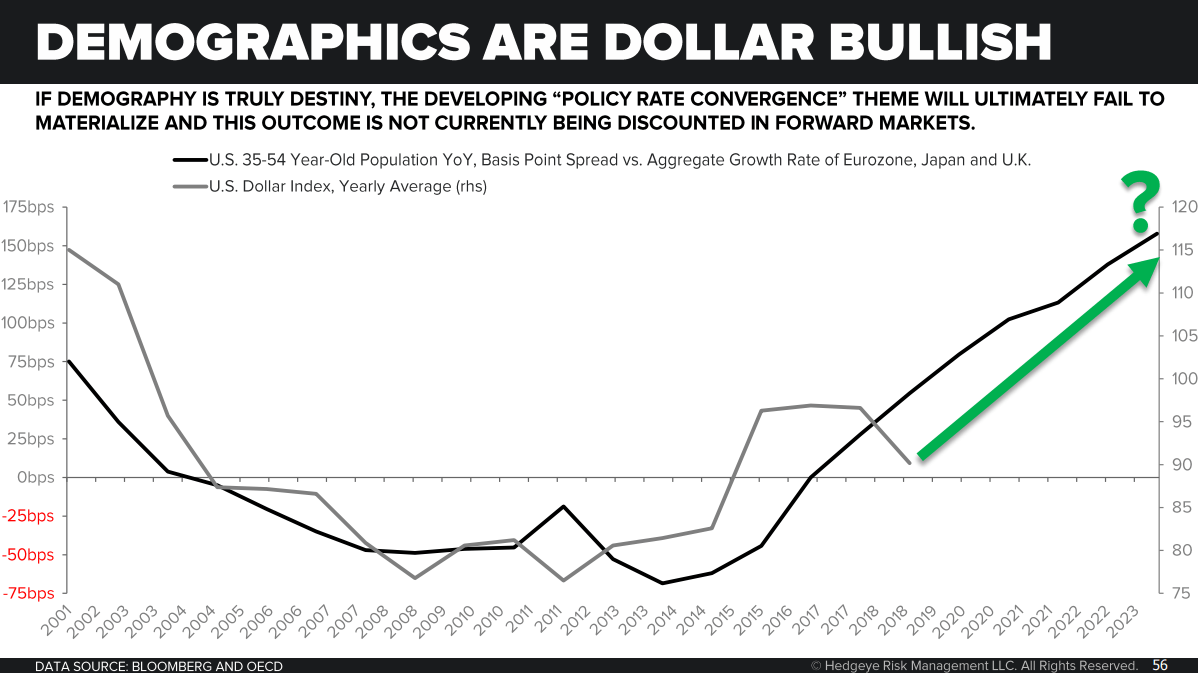

Darius: From a structural perspective, we actually have a fairly positive bias on the dollar. If you look at Slide 56, actually, what we’re showing is the summary of our demographic analysis. On the left side is the spread between the growth rate of the US’s 35–54 year old population. What our demographic analysis has found out is that, if you track that cohort, what that tends to be is the highest income earners and the highest spenders in any given economy, in advanced economies.

If you track that cohort as a proxy for potential growth in inflation pressures, what you learn is that, as we progress from 2017, 2018, and into 2020–2021, the US is increasingly positively disposed – or, saying it more succinctly, the dollar has increasing tailwinds. These would be these aging European economies that actually could potentially be in a fairly precarious spot from the perspective of their potential growth and inflation. Certainly with central bankers that are leaning hawkish in these economies, potentially at precisely the wrong times.

Erik: So your view, at least based on the information available today, is that the backdrop is dollar bullish for at least the next five to ten years to come?

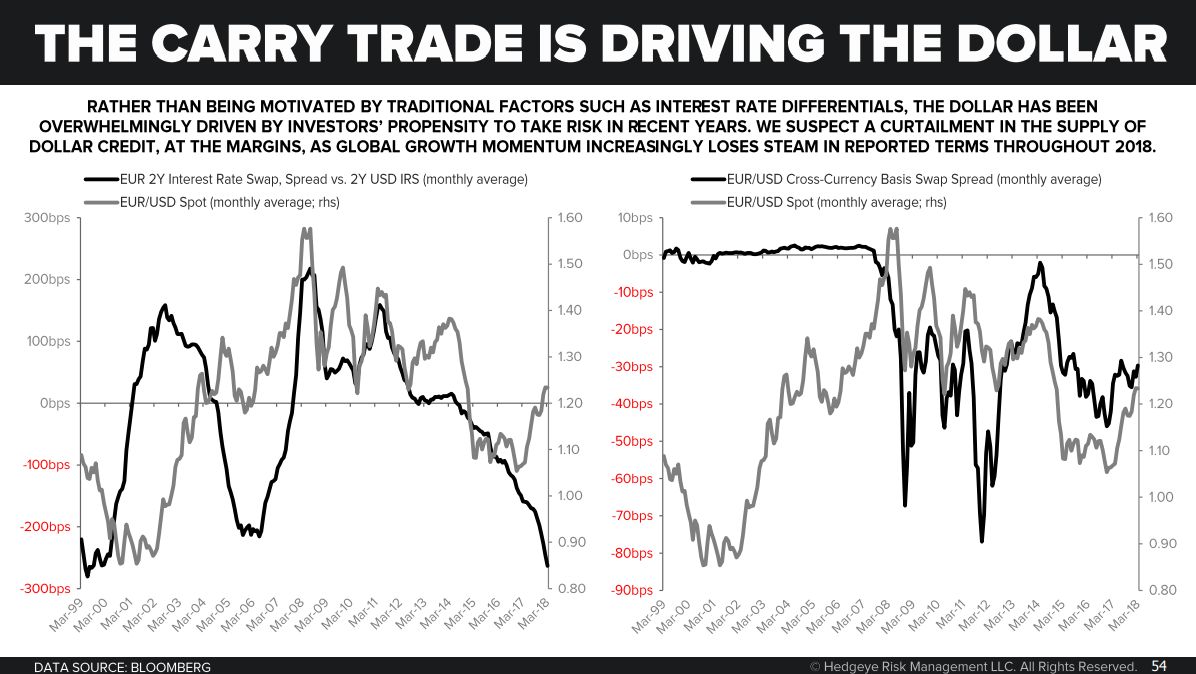

Darius: If you isolate demographics as a factor. Now, again, we would be remiss to isolate any factor on the world’s reserve currency and on a market that trades 4 and a 1/2 trillion dollars in daily liquidity. I think there’s a myriad of factors that shock currencies. One of the factors – and, in fact, going back to this globally synchronized recovery narrative, we show this on Slide 54 – one of the things that I think confounded investors and even confounded us at the beginning of 2017 was the fact that the dollar wasn’t responding to traditional interest rate spread analysis.

What it had been responding to the entire time is something you guys have discussed at great length here on MacroVoices, this alleviation of global dollar funding pressure that we see in Eurodollar markets. And, as a proxy for that, we’re showing cross-currency basis swap spreads trending back towards covered interest parity over the past 12 to 18 months. And that’s something that’s been very negative for the dollar.

Because all that means is investors are increasingly comfortable speculating, carry trading, taking risks on the global economy as a function, again, of the globally synchronized recovery. We would expect the deviation from covered interest rate parity to resume, we would expect the global dollar funding pressures to resume, and we would expect the dollar to trend higher from here.

Erik: Darius, you just referenced the traditional macro conventional wisdom that says that as the interest rate that can be realized on Treasuries in any country improves over its competition – in this case it would be US Treasury yields are offering a better return than something like German Bunds – that’s supposed to create an inflow.

And that, for probably the last year or so, that normal effect that should have been dollar bullish actually seemed to be operating in reverse. What do you guys make of that breakdown in the usual relationship between the currency and interest rate differentials?

Darius: Again, we would never isolate any one factor. I think at any given time you have to have a keen eye on all of the factors that affect currencies. So, obviously, changes in policy expectations, interest rate differentials, the supply and demand for dollars in global capital markets, demographics, deficits, debts – all these things can matter at any given moment. And it’s our job as investors to identify what’s driving returns at any given moment and how likely that is to persist.

What we’ve identified in this analysis is that investors are no longer seeking just the traditional carry pickup and more – it’s more advanced economy markets. What we’ve learned is that investors are very keen to go speculate in more risky securities and riskier assets abroad. Probably as a function of the recovery in global growth and domestic growth. And also as a function of having to move further out on the risk curve to take advantage – or at least to protect their portfolios from Fed tightening.

At some point – which we highlight on Slide 55 – at some point that all ceases to be the case. So, historically, what we’ve seen during Fed tightening cycles is that the dollar tends to trade down during that cycle, I think for some of the reasons I just identified. But as you get to the latter parts of the cycle you start to see some degradation in the global economic scenario. You start to see some capital calls and whatnot. The system really starts to reverse on itself. So that’s the number one risk we’re calling out is that, as you progress throughout 2018 and the globally synchronized recovery is no longer intact, you could actually start to see reflexive covering and closing of these carry trades that investors have been keen to chase over the past couple of years.