“You cannot separate knowledge with contact from the ground.”

-Nassim Taleb

From everything you learned in “school” to risk managing markets in the real world, isn’t that the truth. Taleb isn’t all about the truth, but the man makes you think about what is the truth.

The aforementioned quote comes from his latest smack-down on the establishment called Skin In The Game where he reminds us of the Greek giant, Antateus (the son of the Mother Earth and Poseidon)…

“Anateus was deemed to be invicible., but there was a trick. He derived his strength from contact with his mother (Earth). Physically separated from contact with the Earth, he lost all his powers.” (pg 7)

Back to the Global Macro Grind…

Can we separate large parts of the Global Economy that are slowing right now (China and Europe) from what’s been nothing short of a fantastic, multi-quarter, US Earnings Cycle?

I guess that depends on your investment duration, from here…

Because this morning Mother Earth delivered a massive power-load to one of her precious FAANGs, Netflix (NFLX). Yep, when year-over-year revenue growth ramps from +35% last quarter to +43% this quarter, that’s called an #acceleration.

When growth accelerates (top down US GDP growth and/or NFLX revenue growth), “expensive” gets more expensive.

But those of you who have contact with the ground rules of bull markets already know that. They don’t teach that Mucker one-liner on “valuation” at the Graham & Dodd school of short selling anything with a big multiple.

I’m focusing on Netflix (NFLX) this am because it’s a big story within the broader market story. Here’s why:

- NFLX was 1 of the first 6 Tech companies to report their Q118 earnings and Q1 is a tough “comp” for EPS

- So far 34 of 500 SP500 companies have reported aggregagate year-over-year EPS growth of +31%

- So far 6 of 68 Tech companies have reported aggregate year-over-year EPS growth of +63%!

No, that +63% is not a typo. Neither is the pre-market quote on NFLX re-testing its all-time closing highs from March. Is this “as good as it gets” for one of the best looking stocks in our @Hedgeye Risk Range product?

Let’s see if it can make higher-highs… and I’ll let you know after that.

May the stock market Gods have mercy on any FAANG component that shows a deceleration in revenue growth… because now the bar has been set high – or as one of your fav politicians might say, “very, very, hugely, high!”

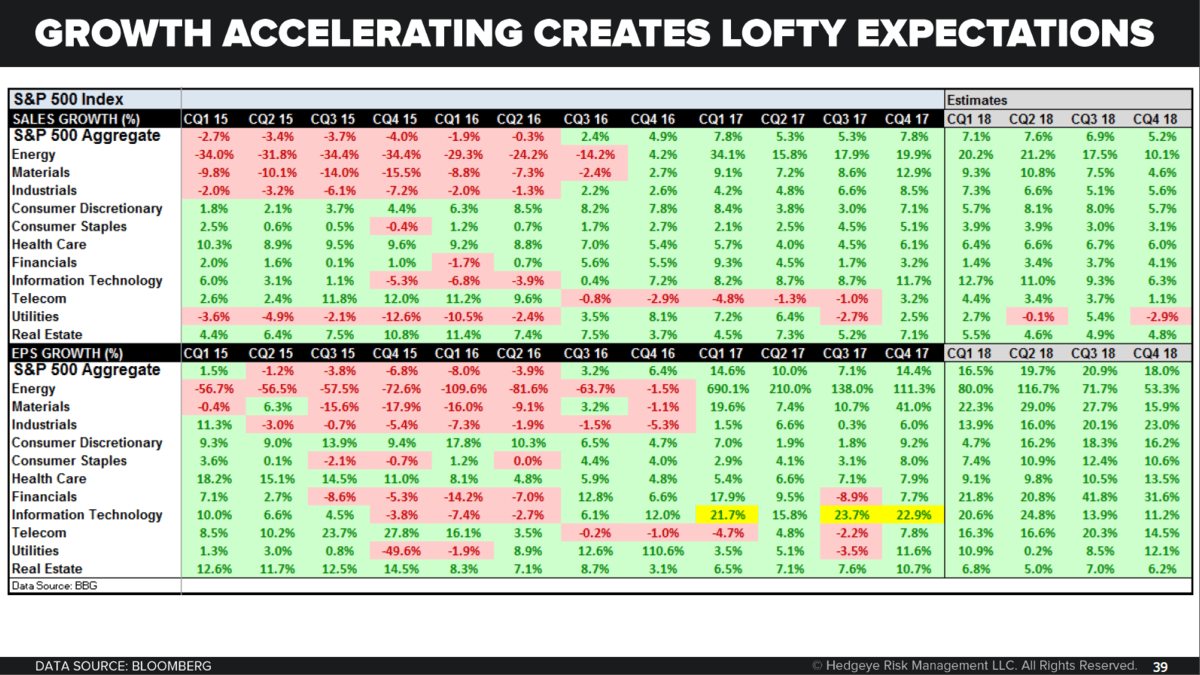

Back to the top-down view of the US Profit Cycle, as you can see in The Chart of The Day (where we highlight the “tough comps”, or comparative growth rates from last year, in yellow):

A) Q1 of 2017 (last year) saw aggregate year-over-year EPS growth for the SP500 #accelerate to +14.6% from +6.4% in Q416

B) Q1 of 2017 saw Tech EPS growth decimate “valuation” bears accelerating to +21.7% from +12.0% in Q416

C) The rest of our growth and profits accelerating call throughout 2017 is history #timestamped

But it ain’t over ‘till it’s over. Again, as you can see in that same chart of SALES and EPS growth data, if the SP500 and Tech were to hold these Q1 2018 to-date growth rates, US stocks can indeed go a lot higher. If they don’t, they can go a lot lower too!

“So”… we will remain in touch with our mama’s on this and update you throughout EPS Season. She taught us to be data dependent.

Mother Earth also taught us to not be US navel gazers. That would be very selfish and narrow-minded of us. It would put is in part of the Macro Tourist crowd (not children of Poseidon) of clown acts too. Two relevant updates on that front this morning:

- #ChinaSlowing

- #EuropeSlowing

While the Chinese tried to make up another headline GDP # of +6.8% for Q1 of 2018 (in line with Q4 of 2017’s +6.8%, despite most of the major components of GDP having been reported as #slowing), the locals in Shanghai didn’t believe it.

The Chinese stock market closed down another -1.4% to fresh YTD lows, taking Shanghai’s draw-down to -14.0% since JAN alone. We reiterated the short China (FXI) call on last week’s low-volume rally to lower-highs (see Real-Time Alerts for skin in the game).

In other news that the Old Wall and its media will not focus on today, ZEW (real-time sentiment/expectations readings) reports #slowed again in both the Eurozone and Mother Germany:

A) Eurozone ZEW slowed to +2 in APR vs. +13 in MAR

B) German ZEW slowed to -8 in APR vs. +5 in MAR

Surely, if asked, Tourists will tell you that this is because of Trump and Trade Wars… or something like that.

We, the data dependent Jedi of the revolution, on the other hand will remind you our #EuropeSlowing call is 6 months old and has mostly to do with both the Chinese and European Industrial cycles slowing vs. their 2016-2017 China Stimulus highs.

You can separate rate of change growth, inflation, and profit cycle knowledge from fake news.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.74-2.86% (bullish)

SPX 2 (bearish)

NASDAQ 6 (bullish)

VIX 16.04-22.94 (bullish)

USD 88.80-90.15 (neutral)

Oil (WTI) 62.01-68.55 (bullish)

Copper 2.99-3.11 (bearish)

NFLX 289-331 (bullish)

TSLA 260-308 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer