"Any change is resisted because bureaucrats have a vested interest in the chaos in which they exist."

-Richard M. Nixon

From a MACRO perspective there were a number of undercurrents that put a bid under the market yesterday.

(1) Getting past the Greek contagion issue improved the RISK AVERSION trade

(2) A below-consensus January CPI print out of China buoyed the REFLATION trade

(3) Initial jobless claims fell sharply in the first week of February helping the RECOVERY trade

(4) The earnings season is supportive of the RECOVERY trade

That said the S&P 500 rallied by 0.97% yesterday, albeit on light volume. The VIX declined 5.67% yesterday and has now declined 9.9% over the past three days. The VIX remains positive on TREND at 22.43. The Hedgeye Risk Management models have the following levels for VIX – buy Trade (22.43) and Sell Trade (28.28). Yesterday, both the Consumer Discretionary (XLY) and Industrials (XLI) joined Healthcare (XLV) as positive on TREND.

As we are waking up today, equity futures are currently trading below fair value as China's Central Bank raises reserve requirements by 0.5% and Germany Q4 GDP data was disappointing. This has the Dollar index up by nearly 1% in early trading. The Hedgeye Risk Management models have levels for DXY at – buy Trade (79.69) and sell Trade (80.69).

On the MACRO calendar today are retail sales and the University of Michigan consumer confidence. In a post yesterday we suggested that the confidence number is likely to be disappointing, given an independent survey we look at that tracks closely the more widely disseminated University of Michigan.

Yesterday, initial claims fell 43,000 to 440,000 to the lowest level in a month and compared with consensus expectations for a decline to 465,000. This brings the 4-week rolling average down 1.5k to 468.3k from 469.8k last week. This is an important print as it reverses the negative trend of the last three weeks, and keeps the trajectory in-line with the data trends since March 2009.

The two best performing sectors yesterday were those that benefited from the REFLATION trade - Materials (XLB) and Energy (XLE). Commodities and commodity equities benefitted as the dollar index gave back all of its earlier gains and ended down slightly. Steel stocks led the XLB; US Steel was the standout in the group after a sell side upgrade. Coal stocks and an outsized rally in natural gas were the bright spots in the XLE.

The Financials (XLF) are like Dr. Jekyll and Mr. Hyde. Over the last three days the XLF has gone from worst, to best, back to the worst performing sector yesterday. There was no overriding catalyst behind the underperformance, as the Insurance names were mixed following earnings from Prudential and the big investment banks were moving in opposite directions.

As we look at today’s set up the range for the S&P 500 is 53 points or 2.9% (1,046) downside and 1.9% (1,099) upside.

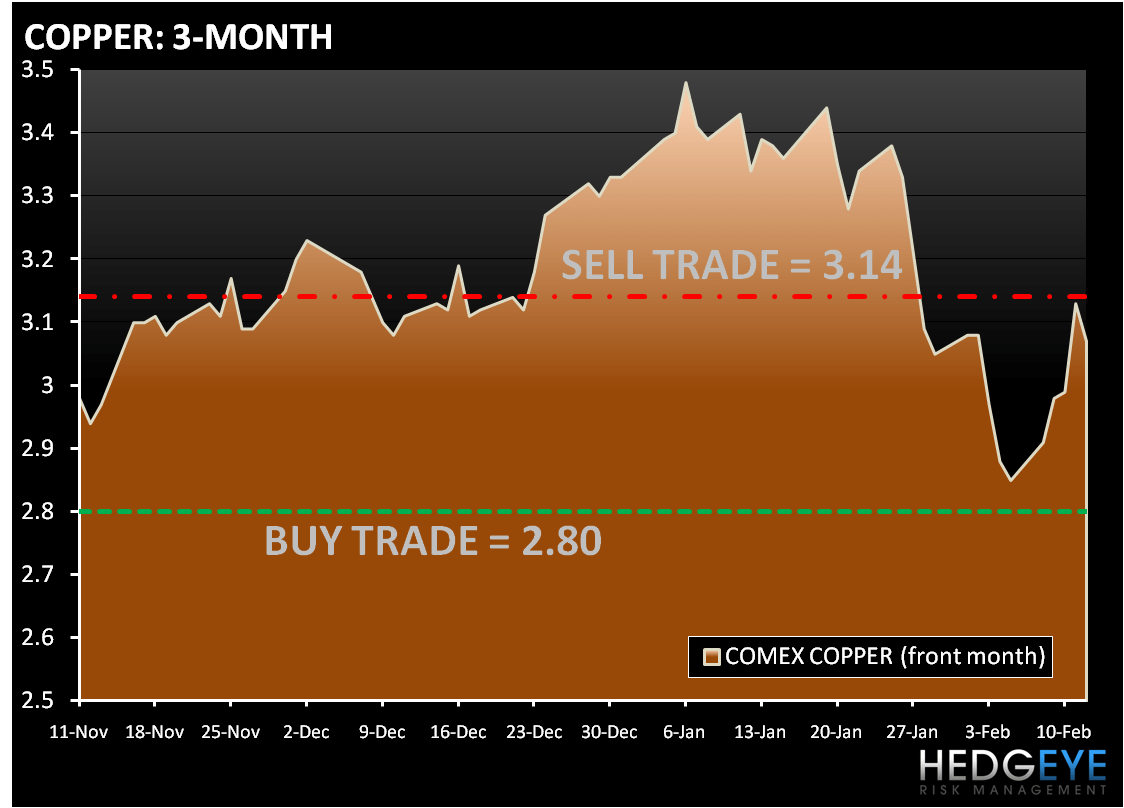

In early trading, copper dropped in London after the biggest weekly rise in more than a year, on concern that a surge may have been overdone. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (2.80) and Sell Trade (3.14).

In early trading gold fell in London with a stronger dollar and China’s move to cool its economy. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,045) and Sell Trade (1,112).

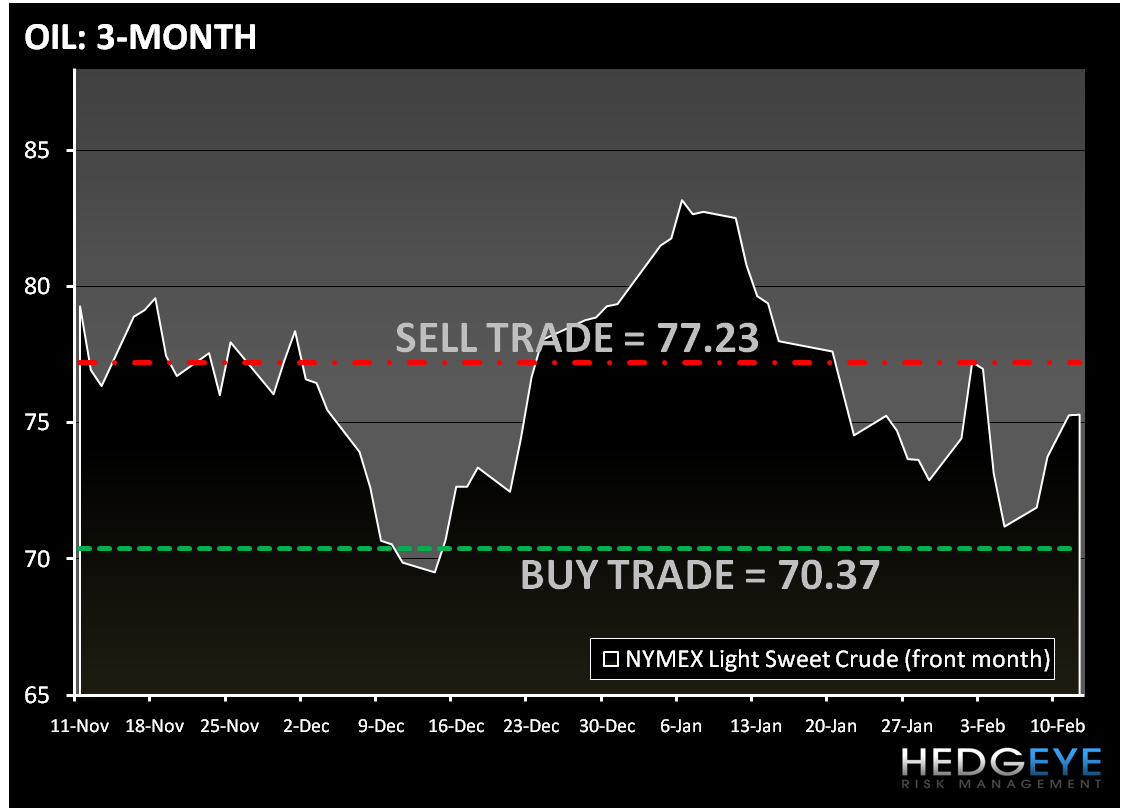

Oil is trading down with the rest of the commodity complex and a stronger dollar. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (70.37) and Sell Trade (77.23).

Howard Penney

Managing Director