There is a chart and there is a catalyst.

President Obama has already put the calendar catalyst for Republicans and Democrats to break bread on the table. That’s set for February 25th.

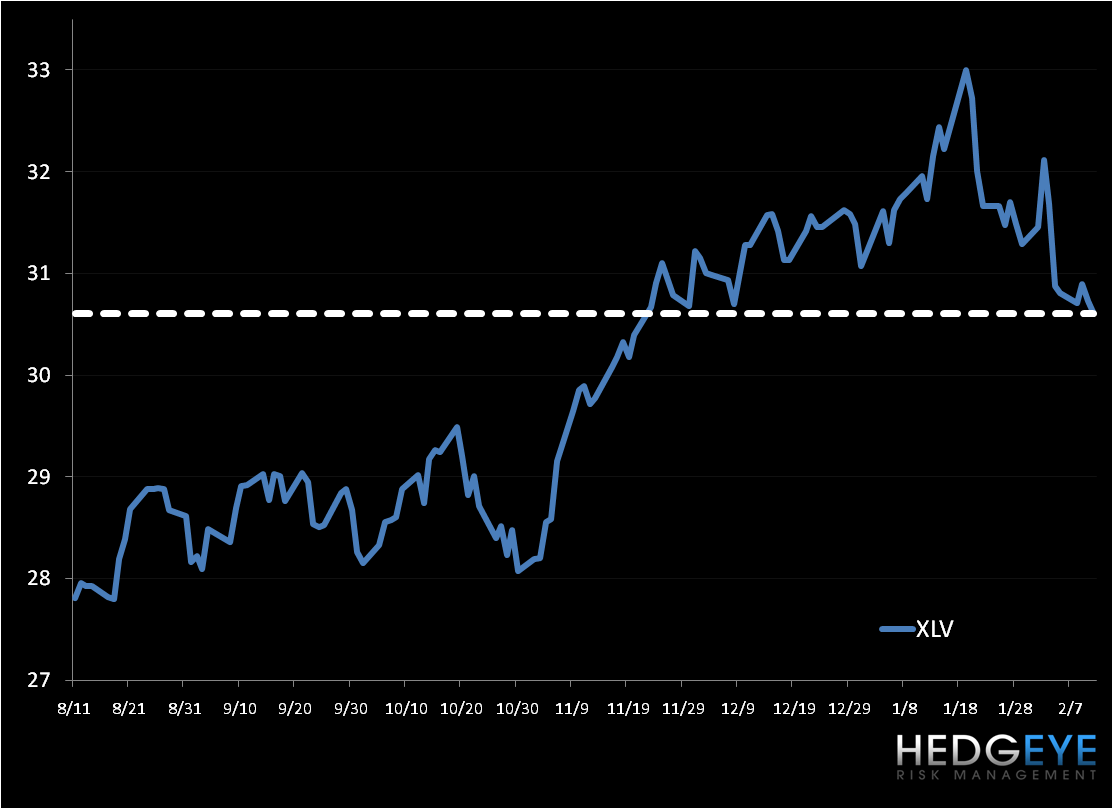

In the chart below, we outline what my Hedgeyes call the Shark Line. That’s the line where those shorting the Healthcare Sector ETF (XLV) either eat or get eaten. We are dancing on the water’s edge of that line today. For the XLV that’s $30.63. Either way, the next move from here should be big.

Importantly, in our 9 sector S&P Sector Risk Management Model, the US Healthcare Sector is the only holdout. This is the only sector that has yet to break its intermediate term TREND line.

Watch this line closely, and beware of the shark.

KM

Keith R. McCullough

Chief Executive Officer