Editor's Note: Below is a complimentary Early Look (our morning market newsletter) written by CEO Keith McCullough on March 27, 2018 telling Hedgeye subscribers to "sell the bounce" in U.S. equities. Here's the backstory...

Heading into 2018, we had been telling subscribers to "buy the dip" in stocks. U.S. #GrowthAccelerating had been firm backstop for domestic equity investors for six consecutive quarters.

By early March though, we were warning subscribers that the stock market was signaling lower-highs. It was beginning to price-in our call on slowing U.S. growth, decelerating earnings growth and declining inflation expectations.

Yes, timing matters.

(Get the Early Look today and save 25%.)

Key Takeaways

|

The Big Picture

The reasoning as to why my answer to the question in the title of this note (Sell The Bounce?) is YES has multiple-factors across multiple-durations. For many Global Equity markets we’ve been selling the bounce for 3-6 months.

While I’m grateful knowing that my answers on “what to do right now” in macro markets has an audience, I’m also cognizant of the short-termism in our profession being as intense as it has ever been. Performance pressure is real. There’s opportunity in that.

The aforementioned quote comes from a great, longer-cycle, research book that I’m in the middle of reading right now called Deep Work – Rules For Focused Success In A Distracted World, by Cal Newport. I highly recommend it.

Macro Grind

Do network tools distract you? How about stock markets that whip back and forth with 14-40 vol? Did it matter that vol (volatility) used to be TRENDING in a range of 9-12? Even if you didn’t know that wasn’t normal – now you know.

Not knowing is actually the point about volatility. What do you really know about what is going to be the macro market “news” for the next 3 months? For me, on growth and inflation, I can tell you, unapologetically, that those answers change every day.

But I don’t confuse what’s happening within that “shorter-term” Bayesian Inference #Process with the context of the longer-term economic and market cycles. That’s the whole point about zooming in and measuring and mapping now vs. then.

The “then” gives us the context of cycles. They are time-series. You can also call them base effects.

What Trump did or did not do with Stormy Daniels … or what tariffs could or could not do to the economy doesn’t matter in our sequencing tools (nowcasting predictive tracking algorithms) until they matter. If they don’t matter, so be it.

Are you ok with that? Not everyone is. And I’m super happy about that.

This is a very competitive game with very intelligent players. The more they are distracted, jumping from headline-to-headline, instead of from time-series to time-series, the better. That’s what gives us our Research Edge.

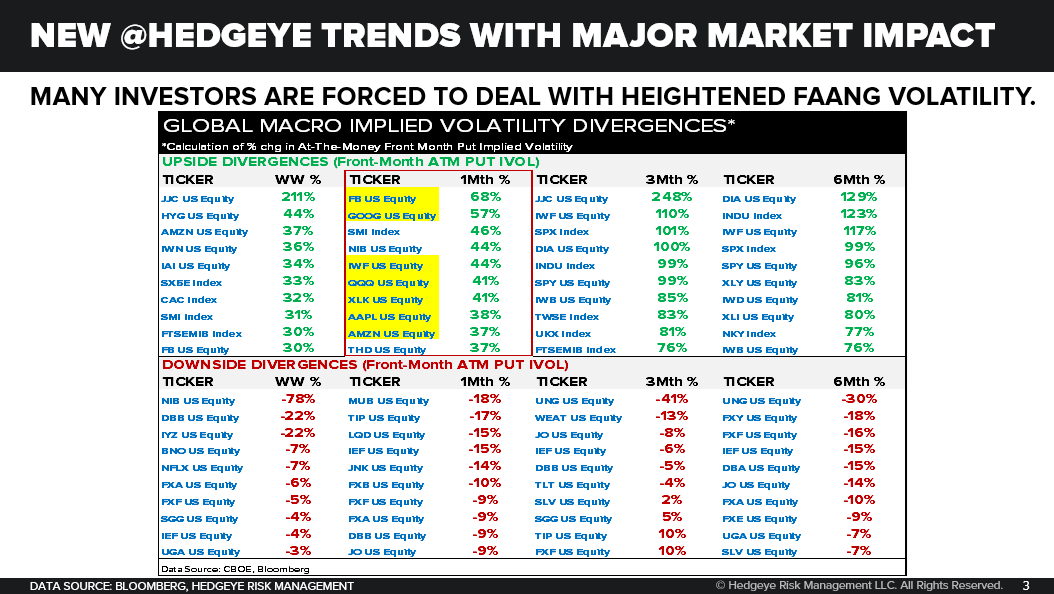

What are the Top 5 (non-tariff) Hedgeye Reasons why Global Equities (including the SP500) are signaling lower-highs?

- Headline US GDP Growth is setting up to surprise to the downside for the 1st quarter in the last 6

- #GlobalDivergences continue to manifest vs. a consensus of a “Globally Synchronized Recovery”

- #ChinaSlowing vs. its mid-2017 acceleration (post the largest stimulus in the history of China)

- #EuropeSlowing vs. its late-2017 cycle peak

- Mr. Market is a leading indicator – cross asset class volatility is breaking out to the upside

If you’d like I can give you plenty of signals within Mr. Market’s signal, but some of these big ones were breaking down well ahead of any Trump tariff tirades by politicized pundits:

- US 10yr Yield signaling lower-highs within its Bullish @Hedgeye TREND

- European 10yr Yields breaking down within its Bearish @Hedgeye TREND

- Nikkei, Shanghai Comp, and most EM Asia Equity markets breaking bad to Bearish @Hedgeye TREND

- Most European Equity markets remaining Bearish @Hedgeye TREND

- Copper, Aluminum, Iron Ore, Nickel, Rubber, etc. all breaking bad to Bearish @Hedgeye TREND

Sure, there are some more recent US ones that have had big equity market impact like:

- Facebook (FB) breaking bad to Bearish @Hedgeye TREND

- Google (GOOGL) breaking bad to Bearish @Hedgeye TREND

- Tesla (TSLA) remaining Bearish @Hedgeye TREND

But none of those break-downs have to do with tariff-talk. If you’d like, my analysts (Jay Van Sciver on TSLA and Neil Howe on FB/GOOGL, who are bearish on all 3) can give you a break-down on why they think those stocks are, well, breaking down!

“So”… when I say “Sell The Bounce”, there’s a much more specific answer to:

A) What, precisely, I’d sell on a bounce… and

B) When I’d sell (see Real-Time Alerts for every #timestamp since 2008)

Timing matters.

Answering the what and when parts of The Question remain critical components of my risk management #process. Timing helps me focus on the bigger picture and longer-term cycles while the crowd is distracted by short-termism too.

OUR LEVELS

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.78-2.90% (bullish)

SPX 2590-2697 (bearish)

RUT 1510-1563 (bearish)

NASDAQ 7002-7421 (bullish)

Nikkei 20562-22003 (bearish)

DAX 11770-12291 (bearish)

VIX 16.31-25.30 (bullish)

Oil (WTI) 59.98-66.90 (bullish)

Copper 2.95-3.07 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer