The guest commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

Watching the continuing trials of HNA Group, we are reminded that the side effect of years of central bank largess will be an arithmetic reckoning when it comes to credit. The massive liabilities accumulated by the likes of HNA, Anbang Insurance and even Softbank will eventually come back to haunt these ambitious Asian debtors. And behind them stands the world’s most indebted state, namely China, governed by the paramount leader Xi Jinping.

“And so castles made of sand, fall in the sea, eventually.” So wrote Jimi Hendrix in 1967, but he was talking about love not global investing, right?

Our friends at Grant’s Interest Rate Observer recently cataloged China’s debt overhang in a comment appropriately titled for the Easter season: “Xi Jinping’s poisoned chalice.” They noted with typical understatement: “The whole world lives at the end of the whip of China’s credit growth.”

Ditto. Especially when that growth is driven by an authoritarian state and makes no sense in economic terms. And yes the size of China’s financial pyramid is extraordinary, as befits a system where political concerns trump all other questions. The Chinese communists have taken the progressive model of money creation from the US and doubled down several times over!

Everyone expressed surprise when the Trump Administration announced the imposition of tariffs on China. But readers of The Institutional Risk Analyst know that last November Leland Miller of China Beige Book pretty much called the start of the trade war down to the day. We asked author and intelligence analyst Jim Rickards what he thought of the timing and substance of the trade actions by Washington.

|

"Many observers are shocked by the new trade wars. They shouldn’t be,” Rickards notes. “Trump has been talking about unfair trade and lost jobs for decades; long before he launched his political career. Unfair trade was a pillar of his speech announcing his presidential candidacy in June 2015 along with immigration and 'The Wall.' “Trump continued hitting the unfair trade issue hard throughout the campaign in 2016, and during the transition after he won the presidential election on November 8, 2016. He intended to make trade his first order of business upon being sworn in as president on January 20, 2017. But then the trade agenda was put on hold. Trump refrained from imposing tariffs in 2017, his first year in office, based on the advice of his national security team including National Security Advisor General H. R. McMaster, Secretary of State Rex Tillerson, and Secretary of Defense James Mattis.” “The national security team urged President Trump not to start a trade war because the U.S. needed Chinese help to avoid a war in North Korea. However, China did not do all it could to apply pressure on North Korea. Once China’s lack of cooperation on North Korea became clear by late 2017, Trump saw no harm in confronting China on trade. Now the gloves are off.” |

But even with the astounding numbers on China’s bad debt pile assembled by Grant’s and the sage political judgment of Jim Rickards, we remain unsatisfied in our search for an explanation of the behavior of Chinese dictator Xi Jinping. Sure, the country’s debt (aka the entire banking system) is enormous, the biggest of any industrial nation on earth. And yes, the political stars seem aligned for a trade war with the Trump Administration. But that still does no explain the level of disarray and haste seemingly driving the consolidation of political power in China.

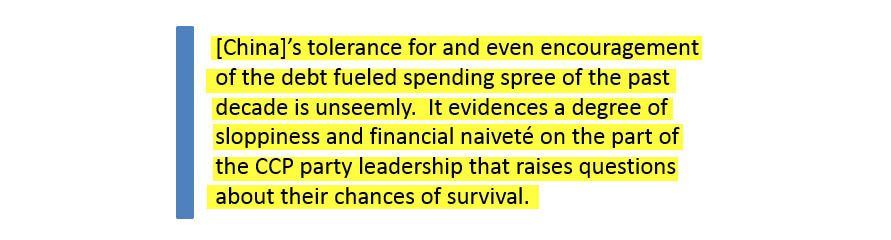

Uncle Xi is a man in a hurry. His moves to eliminate rivals in the Chinese Communist Party have come swiftly, as have belated moves to seize insurer Anbang and extend credit to the apparently insolvent HNA. But more to the point, the CCP’s tolerance for and even encouragement of the debt fueled spending spree of the past decade is unseemly. It evidences a degree of sloppiness and financial naiveté on the part of the CCP party leadership that raises questions about their chances of survival. Viewed in this light, Xi’s moves to consolidate power may be seen as defensive and reactionary.

The thing western analysts have trouble accepting is that the Chinese economy is actually far weaker that the state-approved statistics suggest. Unemployment and massive bad debts are just part of an increasingly unstable situation in some Chinese provinces. China’s "One Belt, One Road" plan, for example, is a bad copy of the New Deal that is doomed to fail in terms of generating real, sustainable growth. But it will certainly add to China's debt.

A trade war with the US will only exacerbate an already bad situation, where the CCP tries to manufacture internal economic demand via subsidies for dead companies and infrastructure projects that produce little or no return. The failure of Xi and the CCP to build a stable, sustainable economic system is the root of the political fear evidenced by Xi and his cronies. James Palmer wrote in Foreign Affairs in February ’18:

|

“[T]he most recent change signals something far deeper than the party’s primacy over the law; it spotlights the essential instability of the entire political system… During Lunar New Year this month, traditional fireworks were banned from Beijing — even down to the firecrackers thrown joyfully by small children. By itself, that could be passed off as a legitimate health and safety measure. But such was the worry about public gatherings that there were not even any organized displays of fireworks. For the first time in decades, the sky over China’s capital as spring arrived was dead, black, and silent.” |

Thus the trade war moves by the Trump Administration, to position for the 2018 and 2020 elections by focusing outward in the daily search for new antagonists, comes at a bad time for China and the financial markets. With Mike Pompeo at the State Department, John Bolton as National Security chief and Peter Navarro as trade czar, you have an almost Reagan era formulation that may try to use trade disputes to provoke a political crisis in China.

Yes, the Trump White house may even think regime change in Beijing is possible given sufficient pressure. Ponder the effect of a 21st Century version of the Taiping Rebellion with nuclear weapons in the mix. China's version of the US Civil War lasted for some 14 years (1850–64), decimated 17 provinces, took an estimated 20 million lives. And this type of unrest is precisely what Xi and China's communist rulers fear.

Financial markets need to anticipate that the tariffs announced by the White House are only the first steps in a much broader retaliation against China for decades of theft and deceptive trade practices. Again, Rickards:

|

“What the market is missing is that all of the tariffs on steel, aluminum, solar panels and the rest are small beer compared to the mother of all trade sanctions coming soon in the form of a “Section 301” report that will land on the President’s desk any day. Section 301 of the Trade Act of 1974 is the “nuclear option” when it comes to trade wars. It does not involve tariffs and subsidies by trading partners. It involves the theft of intellectual property. The damages from Chinese theft of U.S. intellectual property will add up to trillions of dollars.” |

He continues:

|

“The remedies available to President Trump are much broader than those permitted by other provisions of the trade act. Trump does not have to retaliate against a specific good or industry. He can impose penalties on any part of the Chinese economy that arguably benefited from the theft of intellectual property. When it comes to electronics, computer code, and the 'internet of things,' that can be almost anything. When the Section 301 report reaches Trump’s desk he has 90 days to make decisions on penalties on Chinese goods. But, those decisions have already been made. Trump is just waiting for the report. When he gets it, he won’t wait 90 days to respond. He’ll respond almost immediately. So, these opening salvos are just the beginning. There's a lot more trade war damage to come." |

As the markets react to the moves by Xi Jinping and Donald Trump, it is important to remember that there is a wonderful co-dependence between the governments in Beijing and Washington. Both leaders need a new enemy to distract their restive populations from other issues.

In the case of President Donald Trump, he needs enemies to distract attention from the increasingly erratic and scandal prone nature of his government. We note, in this regard, that our colleagues at Kroll Bond Rating Agency just assigned a "AAA" rating to the United States even as we stare at $1 trillion plus annual fiscal deficits. Really?

For Uncle Xi, he seeks to focus attention away from the growing tyranny and insecurity evidenced by China’s return to 1950s style authoritarianism. With growing concerns about the political stability of China, including unflattering comparisons of Xi with Romanian dictator Nicolae Ceaușescu (1918-1989), it will be increasingly difficult for corporate cheerleaders in the West to sell the China growth story.

In the case of both Uncle Xi and President Trump, we should remember the words of George Orwell in his 1944 classic, “Animal Farm: A fairy story.”

|

“Twelve voices were shouting in anger, and they were all alike. No question now, what had happened to the faces of the pigs. The creatures outside looked from pig to man, and from man to pig, and from pig to man again; but already it was impossible to say which was which.” |

Happy Easter.

EDITOR'S NOTE

Christopher Whalen is Chairman of Whalen Global Advisors LLC, a Wall Street insider who understands the intersection of politics and finance, and says what he means. He has worked in politics, at the Federal Reserve Bank of New York and as an investment banker for more than 30 years. He is the author of three books Inflated (2010), Financial Stability (2014) and Ford Men (2017).

In 2017 he resumed publication of The Institutional Risk Analyst and contributes to many other publications and media outlets. He just launched the first volume of The IRA Bank Book, a review of the operating and credit performance of the US banking industry written for institutional investors.