“We don’t know what we’ll be doing a year from now. It’s a mistake to try and get too precise ….you can’t expect the Fed to spell out what it’s going to do...because it doesn’t know."

- Stanley Fischer

So, decent delivery and solid Q&A turnover rate for Powell in his virgin run at threading the policy equivocation needle as he saw Draghi’s double-talk dexterity and raised him a Fischerian quantum of non-prevarication.

Anyway, we’ve detailed the evolving inflation narrative extensively over the past 3+ months alongside our expectation for a cresting and rollover in Reflation trends as we moved through 1Q18.

To quickly set the contextual stage, here’s how we (again) reduxed the prevailing setup most recently:

For most of 2017 equities and rates were positively correlated as rising yields were viewed as a reflection of an improving growth outlook.

That narrative reversed alongside (among other things) the hourly earning print in the February NFP report as accelerating inflation, the prospects of a steeper monetary policy trajectory and growing Treasury supply angst (Fed balance sheet run-down in combination with diversification away from U.S. dollar reserves and debt financed fiscal stimulus) supplanted Goldilicks as protagonist and markets transitioned to trade in directional lockstep with real rates.

Speculative net short positioning in treasuries subsequently ramped to >2 Standard Deviations and the yield on the 10Y UST peaked at 2.95%. At the same time, coordinated, hawkish rhetoric out of the BOJ and ECB aimed at transitioning expectations towards QE cessation only perpetuated the moves in rates and volatility.

Importantly, remember, the build in consensus macro positioning and the collective Central Bank rhetorical shift was largely predicated on extrapolating rearview conditions forward – specifically, the expectation for a continuation in the harmonized global growth and inflation trend …. Skillfully or fortuitously, shorting the low in bonds and extrapolating a continuation of synchronistic global growth were/are not our calls.

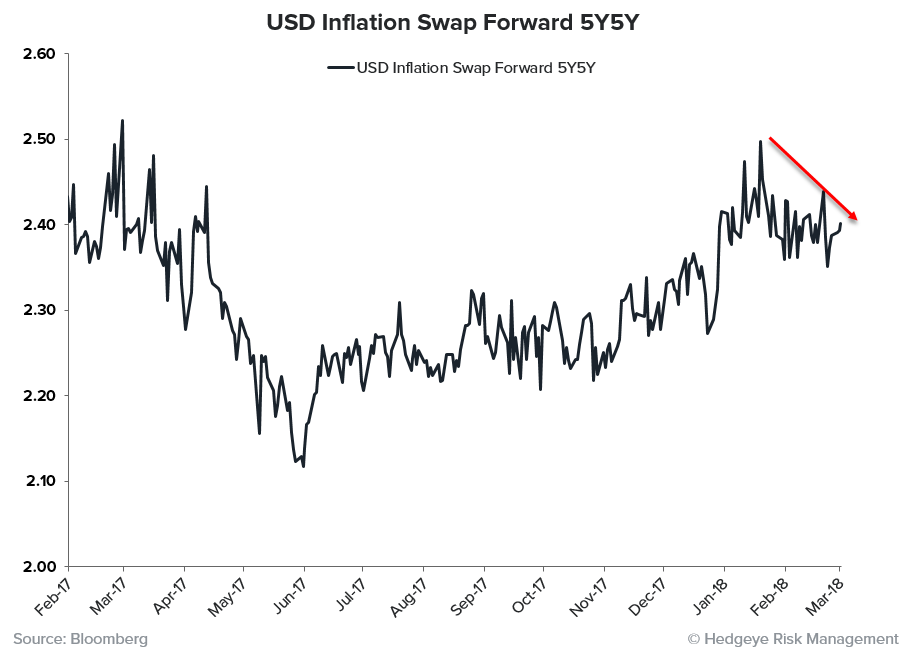

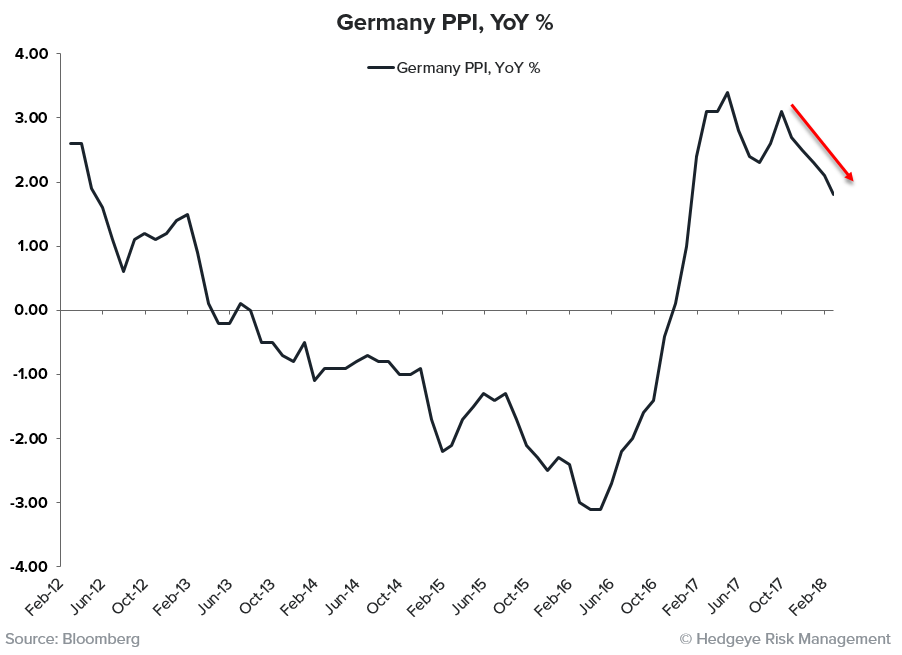

As an update to our Reflation’s Rollover Theme and in the wake of a rash of disinflationary wholesale price growth data out of the Eurozone, we thought it worthwhile to simply update and catalogue the prevailing trend across a meaningful selection of global inflation metrics.

Indeed, the specter of accelerating price growth may be slowly intensifying domestically and “harmonized” may still be an apt descriptor of global inflation expectations …. but, as it stands, that harmonization is now largely a disinflationary chorus. And if our #GlobalDivergences call begins to manifest more acutely with growth decelerating across China and significant swaths of the Eurozone (alongside a pending inflection in domestic growth), disinflationary pressure is more likely to build than ebb over the near-to-intermediate term.

The cross-section of charts below is necessarily non-exhaustive but the emerging, negative 2nd derivative synchroneity should be fairly conspicuous.

Christian B. Drake

@HedgeyeUSA