I never had a policy; I have just tried to do my very best each and every day.

~Abraham Lincoln

Some might say that the positive bias in the S&P 500 on Tuesday was driven by the dampened RISK AVERSION trade following some positive news regarding the European sovereign credit contagion. Yesterday was really all about the FEEL GOOD trade. With the Dollar index and the VIX comfortable above the TREND and TRADE and not doing much of anything yesterday, the 1.3% rise in the S&P 500 is all about the New Orleans Saints winning the super bowl (it just took a day to sink in.)

Seeing Bourbon Street come alive last night was amazing to watch. I have never watched a super bowl parade until yesterday. Four years after being ravished from hurricane Katrina, New Orleans is back and is a small metaphor for the USA. It makes you FEEL GOOD knowing that someday the US recovery story will be well grounded under the right leadership! Unfortunately, it still feels like the USA is in training camp.

Sovereign credit contagion concerns have been among the strongest macro headwinds facing the global markets over the last few weeks, and while there no explicit EU backstop for Greece, the market had a more positive tone on the belief that there will be. To use the line that Jerry Maguire made famous and Drew Brees is thinking - “show me the money.”

Yesterday’s performance made you FEEL GOOD about the global RECOVERY trade. While some of the more defensive leaning sectors such as Healthcare (XLV) and Utilities (XLU) lagged the market, the two best performing sectors are leveraged to a global recovery - The Materials (XLB) and Energy (XLE). A sell-side upgrade of the Industrials (XLI), rounded out the three top performing sectors.

The Materials (XLB) sector was the best performing sector yesterday, on the back of dollar weakness. The Dollar index has now declined for the past two days, declining 0.55% yesterday. The Hedgeye Risk Management models have levels for DXY at – buy Trade (79.48) and sell Trade (80.64). Within the XLB the Steel and Ag chemicals names were some of the strongest performers.

Yesterday, the Consumer Discretionary (XLY) was the second sector to turn positive on TREND. Helping the XLY was the above-consensus January global comps from MCD and some fairly upbeat commentary on the retail space. A headwind for the XLY yesterday was the Homebuilders. The strength is the housing recovery story is government sponsored and that sponsorship will start to disappear in 2Q10. We remain very cautious on the housing recovery story!

The two notable underperformers yesterday were Technology (XLK) and Financials (XLF). The banking group was a slight laggard, with both money-center and regional’s underperforming. Yesterday we shorted CIT. Josh Steiner wrote a great research note on CIT Monday after the media got too excited about John Thain entering the building. In short, the cost of capital is a major issue that will not go away anytime soon.

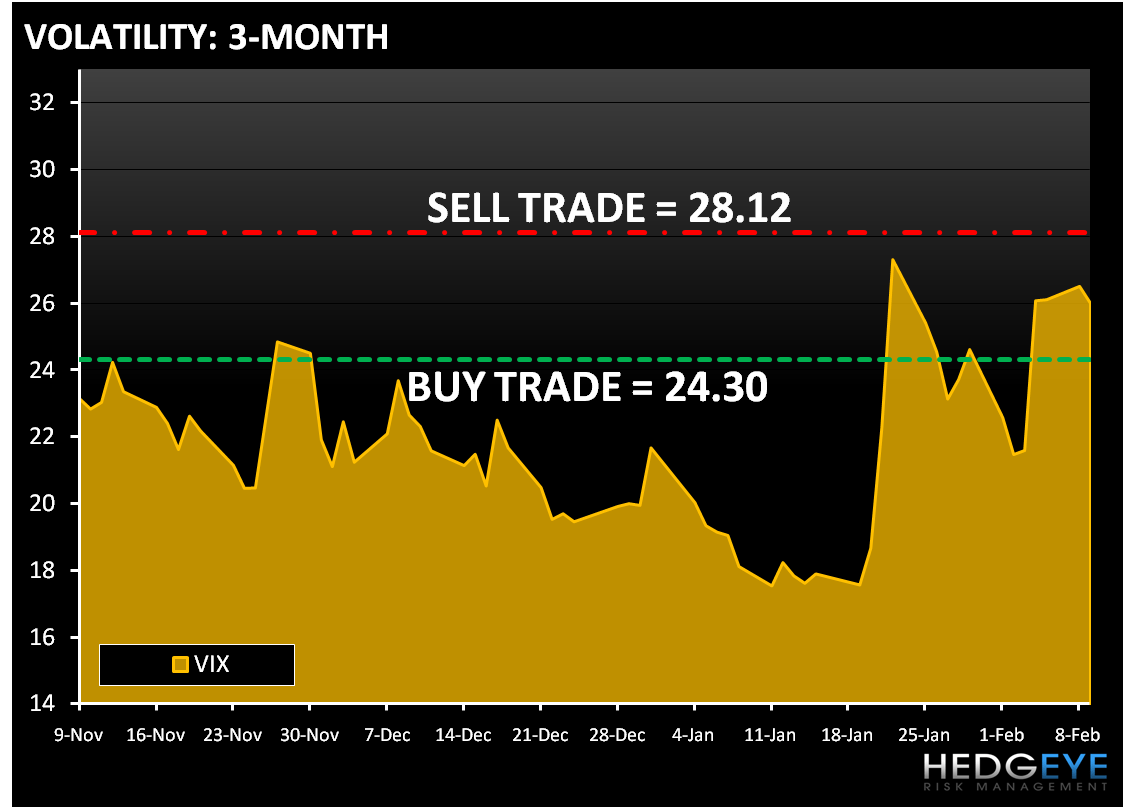

As we look at today’s set up the range for the S&P 500 is 36 points or 2.0% (1,048) downside and 0.74% (1,078) upside. Equity futures are currently trading above fair value, rallying on news Germany said to consider Greek aid beyond loan guarantees. News about Europe (or Germany) offering Greece some life support continues to be a significant driver of the RISK AVERSION trade. I still FEEL GOOD that the party in New Orleans will continue into Mardi gras next week. The Hedgeye Risk Management models have the following levels for VIX – buy Trade (24.30) and Sell Trade (28.12).

Copper is trading higher for a third day as January imports by China rebounded from last year. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (2.81) and Sell Trade (3.14).

The correlation for gold continues - gold is trading higher on the back of a weaker dollar. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,047) and Sell Trade (1,111).

The American Petroleum Institute reported that crude inventories rose to the highest since October last year and gasoline supplies reached the highest since March 1999. Currently Oil is trading up slightly on the day! The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (70.02) and Sell Trade (77.27).

Howard Penney

Managing Director