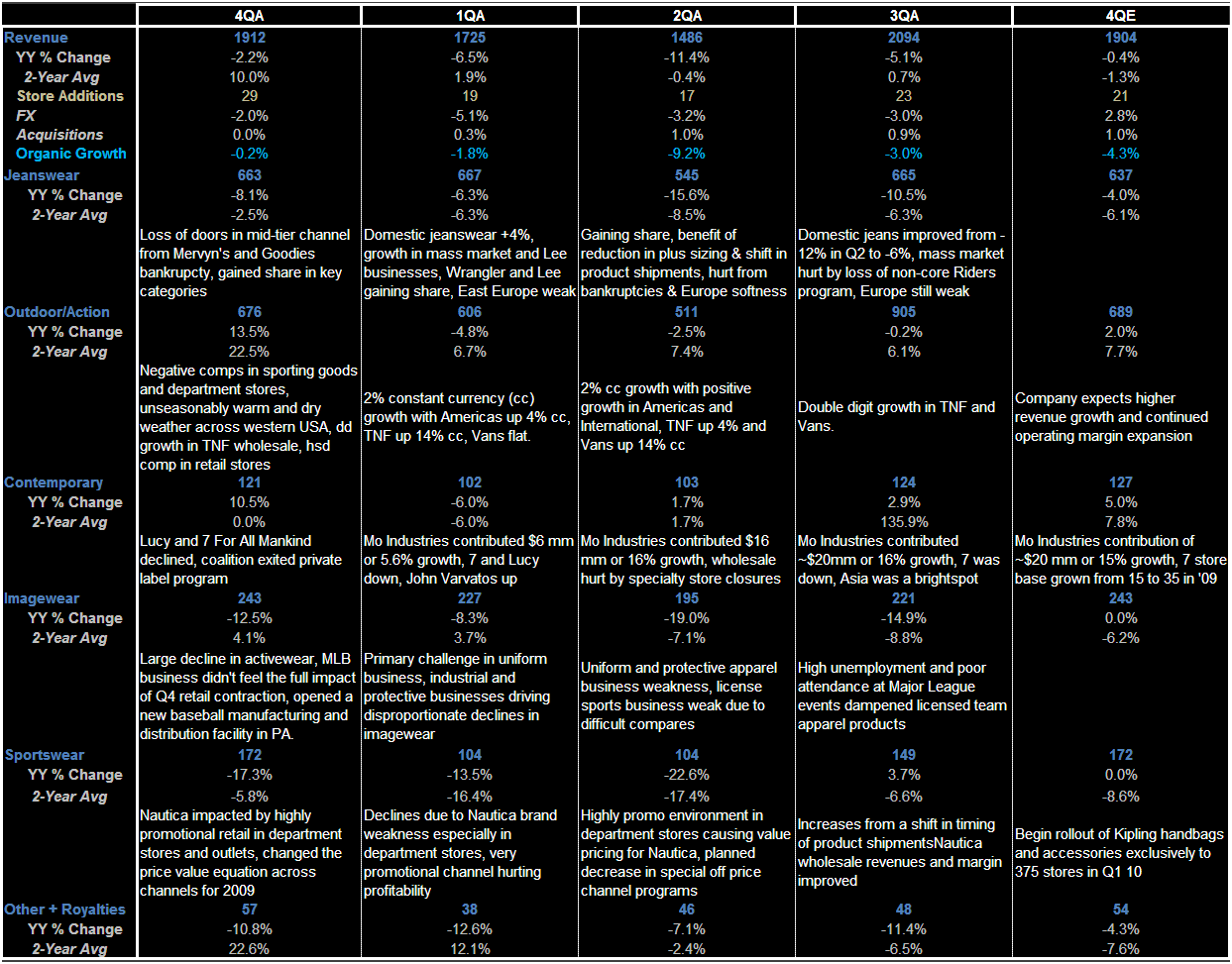

VFC likely has enough gas in the tank to make numbers on Thursday, but we think that the consensus is right for the wrong reasons. We are in line with the street at $1.46 for Q4, and would not be surprised to see a beat (in typical VFC style). Next year they HAVE TO do a deal in order to hit estimates, which they are likely to do. Both forward trends and yy compares look decent for 2 quarters until then. These guys are wizards at financially engineering their way out of a negative growth scenario, and managing expectations accordingly. I don’t have any ammo to suggest that this will break fundamentally.

Revenue: Should print a flat to slightly down top line vs. a -2.2% last year. Then they go up against a -6.5% and -11.4% in 1Q and 2Q, respectively. This happens at the same time a 3-5% FX drag turns into a 2-3% tailwind. Also, VFC has accelerated store growth and added almost 90 retail stores over the past 4 quarters, which naturally boosts sales as mix shifts to fully captured-retail sales instead of shared wholesale. Putting it into numbers, VFC grosses about 1.5mm annually per store, with about $400k in the fourth quarter. All said, we’re looking at a 1.5%-2% boost in revenue simply from the addition of VFC retail. So we’re looking at a boost from retail and FX and even a point in growth from acquisitions – which is in consensus numbers. I’m not sure that the consensus knows why it’s right. But that might not matter.

Margins: Gross Margin compares are easy in 4Q and ridiculously easy in 1Q. And yes, both retail and FX will start to help. The consensus numbers only have a 1pt GM rebound in 1Q – even though they face a -3pt compare vs. last yr. Considering how FX was blamed for a good portion of 1H 08’s declines, it alone should get them a point in recovery. As guided, nothing major on SG&A, though higher retail costs will pinch a bit. I actually like how they’ve been investing in SG&A despite downturn over past 6 quarters. This makes them either careless, or good, proactive managers. They’re the latter.

Balance Sheet/Cash Flow: Inventories have been tight in 2009 and should continue in Q4 and 2010. Capex coming down this year to 1.5% of sales. Good near term. But can’t go any lower. It will need t go up next year, which will pinch cash flow later in the year. For now it’s a wash.