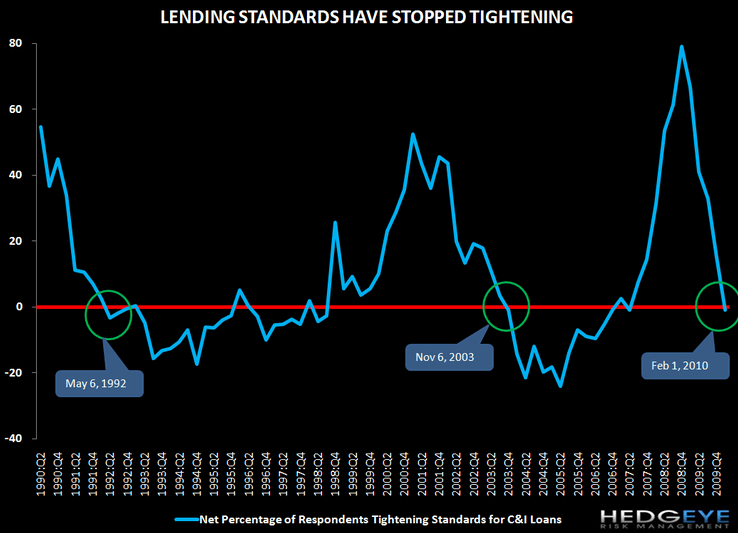

The Federal Reserve Senior Loan Officer Survey came out on Feb 1. There was no material change in trend from the last few surveys. That said, this survey did mark an inflection point of sorts in that the net percentage of banks tightening vs. last period was actually zero (for C&I loans). In other words, on average, banks have finally stopped tightening their lending standards on C&I. The following chart demonstrates. For reference, the chart shows a blend of the large, medium and small bank survey data.

The below chart looks back to 1992 and 2003 as the prior two instances when the banks stopped net tightening. Financials traded higher over the two-year periods following the point at which banks stopped tightening. However, we should point out that in both 1992 and 2003 Financials were relatively range-bound for the first 4-5 months thereafter, for the most part staying within a +/- 5% band. We use an equal-weighted basket of 20 mid-cap and large-cap banks that traded back to 1990 for our benchmark.

Banks are still tightening in some asset classes, however, such as CRE loans. The following chart shows that 30% of banks put the brakes even harder this quarter on the CRE front. That said, the trend clearly shows we're closer to the bottom than the top on CRE - an important read through to credit quality for the regional banks.

At the consumer level, banks continue to tighten on residential real estate loans.

Meanwhile, consumer demand for mortgage loans fell materially in the fourth quarter. The increase in prime residential mortgage loan demand dropped from +28% to -8% linked quarter, while the change in demand for nontraditional mortgages fell from -4% to -35%. Subprime data hasn't been recorded for 4 quarters now.

What we find really interesting is the fact that banks are now finally more willing to lend, but consumers are pulling back at a growing rate, even as unemployment is leveling off and starting to decline.

Conclusion. We think the conclusions are four-fold. First, Financials have historically risen in the wake of banks reaching the zero-line with respect to net tightening on C&I loans. The caveat is that they haven't done much for the first 4-5 months of that two-year period, which would correspond to Feb 2010 - June 2010. Second, commercial real estate tightening, while still underway, has fallen from 87% to 27% in the last 5 quarters in, more or less, a straight line. We think this bodes positively for regional banks with CRE exposure. Third, residential mortgage loan demand dropped in both the prime and nontraditional categories. We think this bodes poorly for future home price trends. Fourth, demand for non-mortgage consumer loans continues to drop at an increasing rate in spite of banks actually now easing their standards for such loans. This tells us that the consumer's demand for incremental credit continues to abate - a near-term negative for lenders, but probably a long-term positive for the country.

Joshua Steiner, CFA