Huge month with some share shifts, mostly related to hold. Feb promises to be a big month again but there are warning signals ahead.

January marked the sixth month of big y-o-y growth in Macau. Total revenues grew 63% y-o-y, with VIP leading the charge up 77%, followed by Mass revenues growing 42%, and slot revenues growing 20%. Melco was the clear share taker in the month, while WYNN was the clear share loser. Luck was a primary factory for Melco's fortune and Wynn's misfortune. MGM also gained back what it lost last month in market share while Galaxy did just the opposite.

As we've written about in several recent notes, February promises to be bring another hot month with the calendar shift of the Lunar New Year and an easy comparison with Feb 2009 seeing a 14.5% revenue drop. We expect a deceleration of growth in March and balance of the 2010 has comparisons become more difficult and the effects of bank tightening start showing some impact on the broader Chinese economy and trickling down to Macau. The other issue may be more a big VIP market share battle initiated by SJM. More on that in an upcoming post.

Y-o-Y Table Revenue Observations:

LVS table revenues up 64% with most of the growth coming from 103% increase in VIP revenues and 21% growth in Mass

- Sands was up 73%, driven by a 137% increase in VIP and 19% growth in Mass

- VIP growth was largely driven by easy hold comparisons. Sands suffered weak hold in January 2009 of around 1.7%, assuming 10% direct play. If we assume 12% of total VIP play was direct in Jan '10, this implies hold of 3.36%

- Junket VIP RC increased 28%

- Venetian was up 41.5% with VIP increasing 58% and Mass increasing 20%

- Most growth in VIP was driven by easy hold comparison. Hold was weak, roughly 2.6% assuming 17% direct play in Jan 2009, vs. an estimated 3.65% hold assuming 20% direct play in Jan '10

- Junket VIP RC increased 12.6%

- Four Seasons was up 259% y-o-y driven by 531% VIP growth and 39% Mass

- Junket VIP RC increased more than five-fold to $858MM vs $137MM. In 3Q09 FS also derived 50% of its RC from direct play versus having almost no direct play in 1Q09. Therefore, if the direct play is material, volumes could be up even more y-o-y than the junket numbers imply

Wynn table revenues were up 27%, almost entirely driven by a 35% increase in VIP, while Mass revenues were only up 2%

- Junket RC increased a massive 115%, however weak hold coupled with difficult hold comparisons, masked Wynn's share gain on the VIP side. Assuming 12% direct RC play in Jan 09, Wynn's hold rate was 4.1% vs. 2.6% in Jan 2010 assuming 13% direct play

- Wynn is battling the the impact of the loss of a VIP operator in mid-December and the departure of property's #2 marketing individual

Crown table revenues grew 144%

- Altira was down -0.6% (the only property in Macau with lower January revenues) due to challenging hold comparisons

- VIP RC was up 28% and hold was normal at 2.8%, however, hold was 3.7% last January

- Mass win was very strong, up 58% y-o-y

- CoD table revenue was up 83% sequentially, benefiting from better volumes and much better sequential hold

- Mass ramped 25% m-o-m to $31MM

- Junket VIP RC grew 24.5% sequentially.

- If we assume 20% direct play at CoD (in line with what MPEL said on their earnings call), then total VIP RC would be $3.5BN and hold appears to be quite high, at 3.7%, meaning any extrapolation of the $40MM of EBITDA MPEL did in Jan would result in a gross overestimation of the company's earnings power for 2010 and coming quarter. If direct play was 20% in December, then the hold would only have been 2.2%.

SJM continued its hot streak, with table revenues up 78%

- Mass was up 53% and VIP was up 96%

- SJM is being very aggressive on junket pricing

Galaxy table revenue was up 32%, driven by a 34% increase in VIP win and a 19% increase in Mass

- Starworld's table revenue was up 60%, driven by 67% growth in VIP revenues and 21% growth in Mass win

MGM table revenue was up 61%

- Mass revenue growth was 30%, while VIP grew 72%

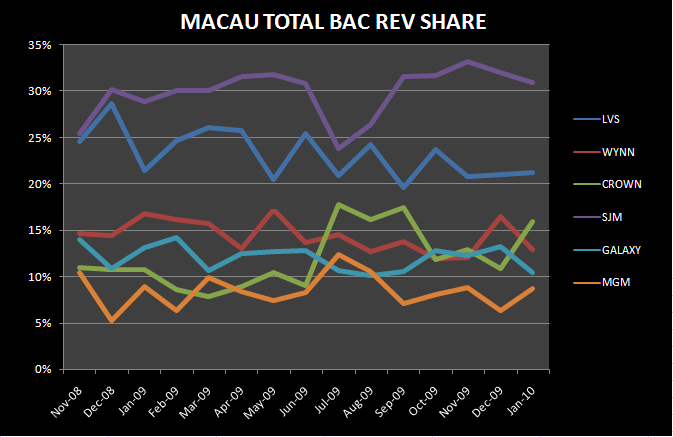

Market Share:

LVS share's was up 20bps sequentially at 21.23%

- Sands' increased 10 bps to 7.1% sequentially

- Escalators and walkways from Ferry Terminal to competitor Oceanus are not yet complete

- Venetian & FS share increased 10bps to 14.13%

WYNN's share dropped to 12.9% from 16.5% share in December

- We attribute the market share change mostly to luck. In January we estimate that hold was only 2.6% while we estimate that December was roughly 3%. Wynn has suffered from poor hold in 3 of the last 4 months, which explains why their average share has been below prior averages

- Departures discussed above probably hit VIP turnover a bit

Crown's market share increased by 5% from 10.9% in December to 15.9%

- Like Wynn, hold was largely responsible for the massive share shifts here

SJM's share decreased to 30.9% from 31.9% in December

Galaxy's share dropped slightly to 10.4% from 13.3% last month

- Starworld's market share fell to 8.15% from 10.4% in the previous month

MGM's share increased to 8.65%, from 6.3% in December

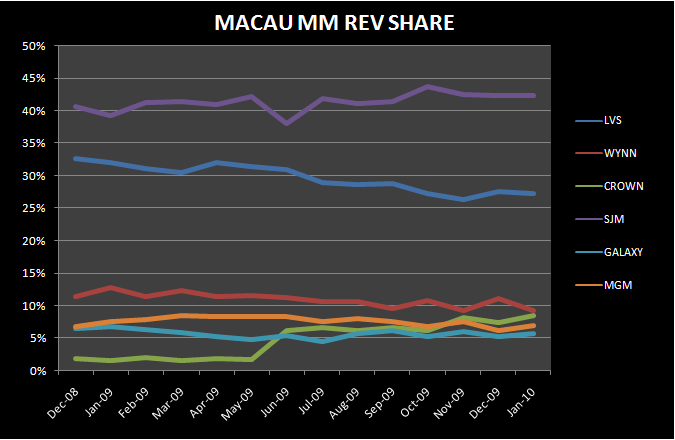

Slot market commentary:

- Slot win grew 20.7% y-o-y to $80MM

- Melco's slot win grew 87% y-o-y with the addition of CoD, LVS's slot win grew 21% y-o-y, and MGM's slot win grew 43% y-o-y

- The other 3 concessionaires had paltry growth in slot win y-o-y, with Wynn's actually decreasing 5% and SJM's only increasing 1%, while Galaxy's increased 9.4%