The S&P 500 declined 0.55% yesterday on decelerating volume. Yesterday’s theme seemed to focus on the fact that sovereign debt issues will not go away. While the European Commission backing of Greece's deficit reduction plan may have put that country concerns on the back burner, sovereign credit concerns shifted to Spain and Portugal. As a result there was a pick up in the RISK AVERSION trade. The dollar Index was up 0.45% yesterday and VIX was marginally higher too.

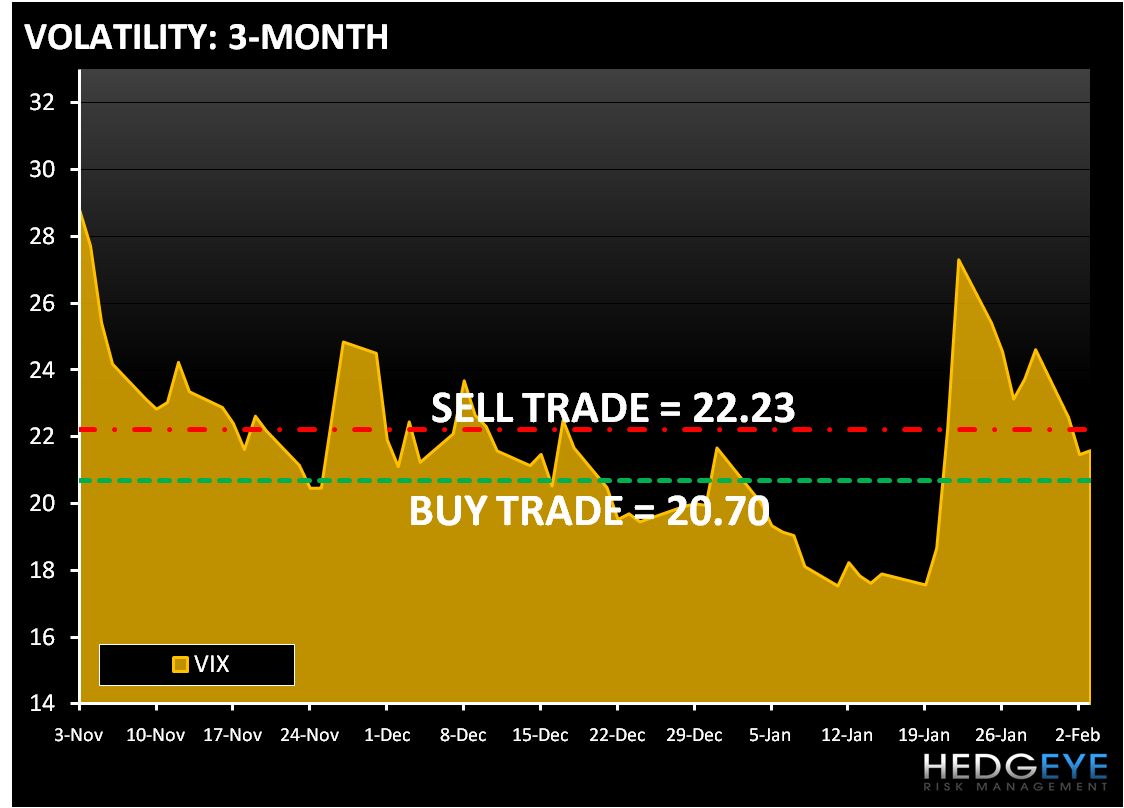

The Hedgeye Risk Management models have the following levels for VIX – buy Trade (20.70) and Sell Trade (22.23).

Given the sovereign debt issues, we do not want to be net long Latin America (Brazil), and as a result we shorted Mexico. Mexico short is a solid compliment to our short position on oil and our concerns about sovereign debt risks. The Hedgeye Risk Management models have the following levels for DXY – buy Trade (78.01) and sell Trade (79.73).

On the MACRO front the ISM non-manufacturing index rose to 50.5 in January from 49.8 in December. However, the headline reading came in below the 51 consensus. The data highlighted the extent to which the services sector continues to lag the recovery in manufacturing. This was made clear in the employment component, which increased to 44.6 from 43.6, a slowing rate of improvement.

Also on the MACRO front the ADP employment fell 22K in January vs. consensus expectations for a drop of 30K, marking the smallest decline since January 2008.

Yesterday, the worst performing sector was Healthcare (XLV); the XLV also broke TRADE. The earnings miss from Pfizer (PFE) and scaled back financial targets for 2012 was not received well. The managed care group also came under pressure with the HMO’s down 1.6% following reports that House Democrats plan to revive a small piece of their healthcare reform agenda that would repeal the HMO antitrust exemption.

The Financials (XLF) was one of the worst performing sectors yesterday. While the insurance space was in focus following a number of earnings reports, the banking group provided a meaningful headwind with the BKX index down 2.4%. The regional’s remained on the defensive amid concerns about the extent of their run-up on the back of the largely favorable takeaways from Q4 results. Money center names held up better on the day, as the group has been a beneficiary of recent thoughts that regulatory concerns may be overdone.

Consumer Discretionary (XLY) was one of two sectors that finished up on the day. Media names were a big driver of the strength following better-than-expected December quarter earnings. MCD also outperformed after the stock was added to the Conviction Buy List at Goldman, while YUM was down 1.3% before it reported mixed results after the close.

As we look at today’s set up the range for the S&P 500 is 33 points or 2.0% (1,075) downside and 1.0% (1,108) upside. Equity futures are trading below fair value following yesterday's decline. Earnings remain in focus and markets may try to draw some benefit from Cisco System's (CSCO) Q2 earnings reported after the close.

In early trading Copper looks to be headed lower for the 2nd day in a row. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (2.89) and Sell Trade (3.14).

In early trading Gold also looks to be lower on the strength in the dollar index. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,076) and Sell Trade (1,113).

Crude oil is headed lower on inventory gains and a stronger dollar. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (72.04) and Sell Trade (78.32). We remain short the US Oil Fund (USO).

Howard Penney

Managing Director