THE HEDGEYE EDGE

We believe AMN Healthcare Services (AMN) shares have been supported by tax reform and the obvious benefit from lowering a ~39% tax rate to 21% and a view that 2018 will bring stability and an easy compare to the hospital industry. While the tax rate change will impact earnings positively, AMN's fundamental performance correlates most strongly with EV/Sales, not P/E. At 1.2x, the current EV/Sales is at the high end of the long-term range. Fundamentals are likely to deteriorate further in our view as the U.S. Medical economy slows in 2018. This is an obvious negative for a temporary nurse staffing company such as AMN.

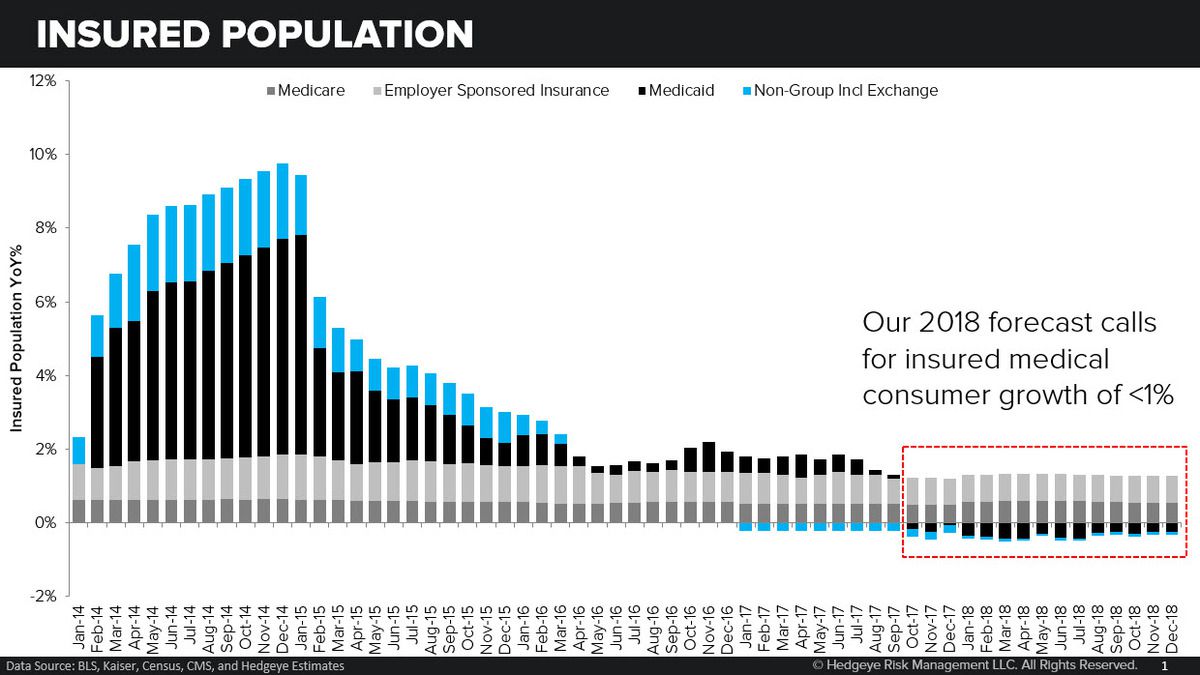

Open enrollment ended on December 15th with 8.8M federal signups, a -4.1% YoY decline. We estimate overall attrition in state and federal exchanges combined to be ~4M. Medicaid enrollment in October was -0.7% and we expect continued income determinations and falling federal matching funding levels to lead to disenrollment of Medicaid overall. According to official estimates, Medicaid is currently ~10% over-enrolled. There continues to be a host of other negative pressures including Exchange declines, HDHP, and rising out of pocket expenses.

In total, our Insured Medical Consumer model now forecasts growth of less than 1% through 2018. Medicare will be the fastest growing segment of the insured population at ~3%, continuing the steady mix shift toward this lower margin payer. While employer sponsored insurance (ESI) will expand modestly, there are several headwinds to individual spending such as co-payments, deductibles, and co-insurance which continue to impact per capita spending. Altogether, these trends have caused an increase in the uninsured population and significant volume and margin headwinds across the US Medical Economy.

Meanwhile, the Current Population Survey (CPS) contains data on employment status by occupation, including registered nurses, and the most recent data available from October 2017 shows a -3.6% decline year over year in the number of "Employed - At Work" registered nurses compared to 4Q16 average.

The implication for a temporary nurse staffing company such as AMN is negative. Declining employment of registered nurses in the CPS data agrees with the decelerating trend in Health Care Employment broadly and Hospital Employment specifically. Consensus' 2018 revenue growth for AMN's Nurse and Allied segment (63% of total) ranges from 5% to 6% throughout 2018, a target we believe will be significantly challenging in what is likely to be a declining market. We also expect a negative industry trend is likely to put pressure on the Other Workforce Solutions.

Price and volume trends continue to reflect weakening demand. 2% pricing along with low single-digit volume results and guidance, and weakening margin trends, all put the long-term view at risk. AMN is not a reliable double-digit growth and margin expansion story.

ONE-YEAR TRAILING CHART