While Healthcare and Biotech Capital Raises have had a historic run through the back half of 2009, the IPO calendar, particularly for speculative biotech, has been notably light.

In yesterday’s morning note we suggested you keep the pricing of the Ironwood Pharmaceuticals IPO on your radar as a potential lead indicator for CRO’s and measure of remaining risk appetite as market momentum & sentiment have rolled in the past couple weeks. The offering, which was expected to price 16.7M shares at $14-16, ended up pricing at $11.25/share – a 30% haircut and the biggest reduction for a U.S. IPO YTD.

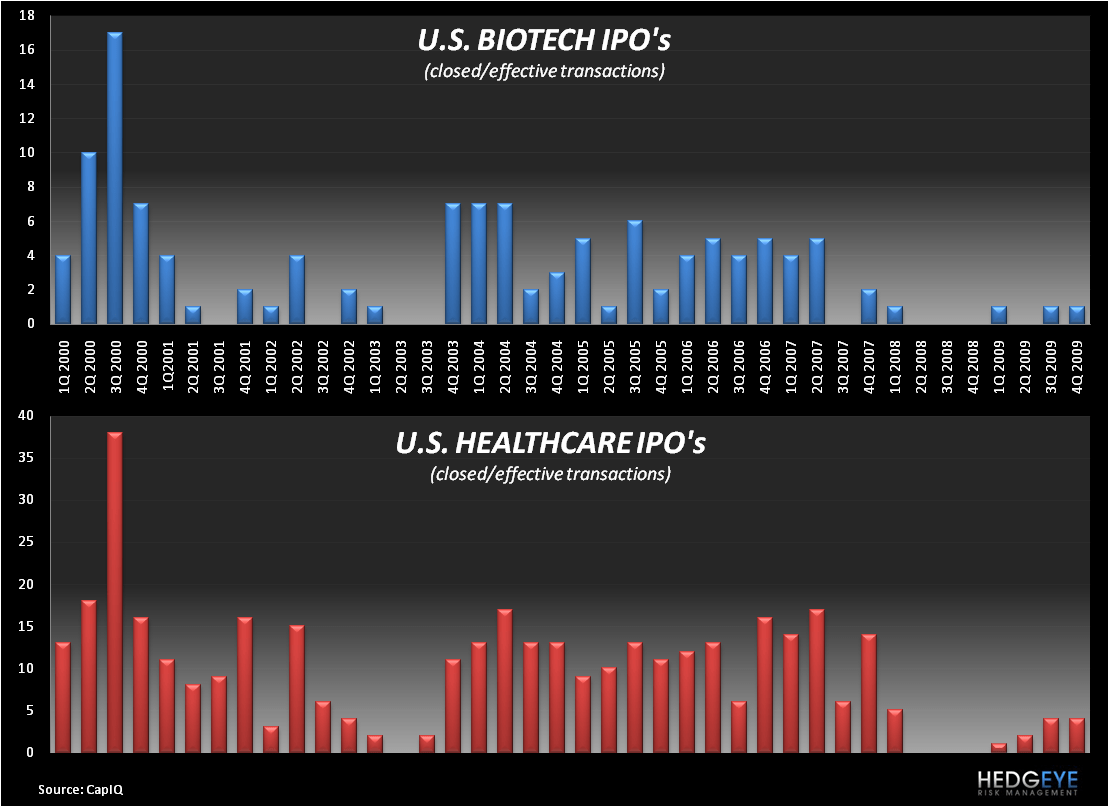

The pricing of IRWD is an extension of the 2009 trend in U.S. Healthcare IPO’s which were both infrequent and uninspiring. Of the nine Healthcare IPO’s debuting in 2009, six have turned in negative absolute performance while underperforming both the XLV and the S&P500.

Coming out of the 2001 recession, Biotech IPO’s didn’t see a meaningful, more sustained uptick until 4Q2003. While the deluge of offerings in the 2000, pre-recession period likely exacerbated the drought in the post recession period it's at least noteworthy to point out the lag between the recovery of the market and ^NBI Index and the recovery in the IPO market. Presently, the success or failure of Ironwood may serve as a Go or No-Go signal for the IPO market and the growing list of prospective offerings backed up in the pipeline.

Biotech has been on a tear of late, capital raising has continued unabated, and a successful return of the IPO market would serve as an important confirmationary indicator of resurgent investor interest and pending capital investment to the industry. The outcome here holds important consequences for Drug Development Service companies who need biotech allocations to drive growth as the Large Pharma outsource story loses juice.

IRWD shares were set to begin trading at 11am and we’d like see at least 3 days of volume & price action before vetting the result. Our next look at the health of the IPO market may come compliments of Anthera Pharmaceuticals who, notably, amended their S-1 this morning to reduce the size of the intended offering.

Christian B. Drake

Analyst