MARKET WATCH: What’s Happening? Last week Google investors got jittery after an earnings report showed rising “TAC”—and last month Facebook investors were spooked by the company’s announcement that it will be de-emphasizing ads in its News Feed. Are these chinks in the armor of digital ad-dependent media, or merely bad news blips? Plenty of investors remain bullish: Spending on digital advertising is growing at a meteoric rate, and the primary beneficiaries have been Google and Facebook, who have seen their share prices shoot up even faster than the overall market in the past year.

Our Take: Investors are pricing in years of steep revenue gains that may not occur. They expect that these firms’ market share expansion will accelerate even while their profit margins never revert to mean. They make the historically dubious assumption that total ad revenue will grow faster than the economy. Some are even waiting for the Internet giants to conquer whole new continents and invent whole new technologies—while taking little heed of worsening social and political headwinds, recently summarized by The Economist as the perception that these companies are “BAADD”: big, anti-competitive, addictive, and anti-democracy. The bulls, we believe, will likely be disappointed.

Are investors seeing some wobbling wheels on the runaway freight train known as the Internet economy?

Last week, Google’s shares dropped over 5% overnight after its Q4 earnings report showed higher-then-expected traffic acquisition costs (TAC). Some investors wondered if this titan of Silicon Valley could be huffing and puffing to get its ads out there.

A couple of weeks earlier, Facebook’s shares dropped more than 4% after the company announced it will be cutting back on ads and sponsored content in its News Feed, wiping out $23 billion of market cap in a matter of hours. While most traders took this as an opportunity to “buy the dip,” others expressed nagging concerns about the company’s long-term future. Here’s a firm whose revenue growth is totally dependent on screen-time growth: Hey, a mounting “tech-lash” against screen time might just be a problem.

But are these just isolated clouds in an otherwise blue sky? By all accounts, the digital advertising industry is firing on all cylinders. According to eMarketer, 2016 marked the first time ever that a greater share of the nation’s ad dollars went toward digital ads (36.7%) than TV ads (36.6%). Preliminary numbers show that gap widening to at least three percentage points in 2017. The Internet is now the single most lucrative advertising medium around, surpassing not only TV, but also (in distant second, third, and fourth place) print media, radio, and out-of-home formats like billboards.

WHAT’S AHEAD

A fair warning to readers: We will be covering a lot of ground in this piece. In the discussion to come, you’ll find the following:

- Why Investors Remain Bullish. Whether in terms of price, expert consensus, or earnings multiple, the market continues to hold Google and Facebook in high regard. These tech juggernauts are unlike any other stocks on the market.

- What Investors Expect. Consensus revenue projections imply that Google and Facebook will be able to keep profit margins high while growing their market share indefinitely. But is this feasible?

- Why the Bulls Are Wrong. For these firms to hit their consensus projections, at least one of three things must happen by 2021: Google and Facebook must utterly destroy their digital competitors; digital advertising must gobble up three-quarters of all advertising; or total advertising must double as a share of GDP. None of the above are likely—nor is any combination that would satisfy the consensus.

- Counterarguments… Countered. To get future revenues “back to consensus,” the bulls issue three counterclaims: first, that revenue growth abroad (ex-U.S.) will accelerate; second, that we still start seeing game-changing revenue growth outside of ads; and third, that these firms will benefit from the twilight of net neutrality and ultimately “own the Web.” We find these claims unpersuasive.

- How Things Could Get Even Worse for Google and Facebook. There are several scenarios in which the future for these firms may be even dimmer than we project. Their margins could shrink, the U.S. ad landscape could crater, the consumer tech-lash against digital could intensify, or the political outlook both at home and abroad could darken. All are very distinct threats to the consensus outlook.

- The Final Word. We offer our bottom-line on how investors should regard these stocks.

But let’s start by examining the financials of the two tech titans.

WHY INVESTORS REMAIN BULLISH

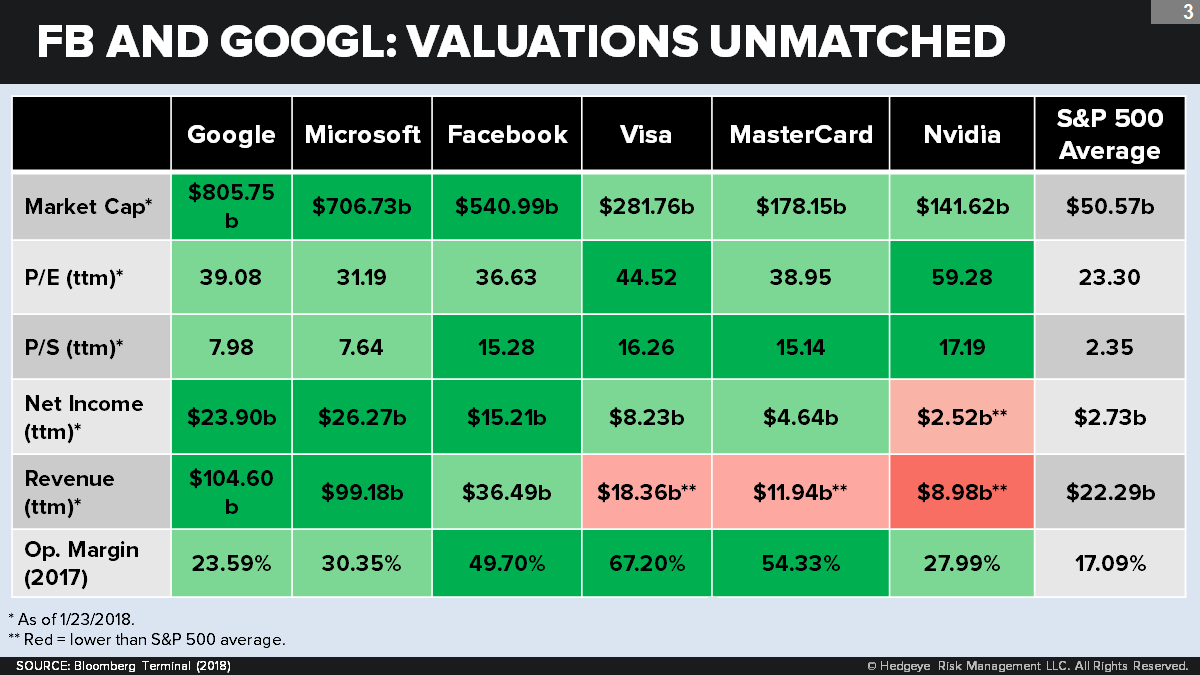

Yes, Google and Facebook rule the U.S. digital ad space—which in fact is worth a massive $71 billion as of 2016 by eMarketer’s count. The two companies together earned $42 billion in net revenue from their U.S. advertising operations in 2016, or 59% of the industry total, according to eMarketer. (For comparison, the next-largest slice of the pie went to Microsoft, at just 5%.) What’s more, the two firms accounted for somewhere between 83% (Pivotal Research Group) and 99% (Internet Advertising Bureau) of the entire growth in U.S. Internet ad revenue in 2016. Rest-of-world growth is similarly impressive.

Wall Street is bullish on the prospects of these media giants. According to a compilation of analyst recommendations by Yahoo Finance, Google currently has 38 “buy” ratings out of 43 total ratings, while Facebook has 41 “buy” ratings out of 44 total ratings. And it’s not just sell-side analysts who are optimistic. The financial media use words like “dominate” and “unstoppable” to shock and awe their readers. Consumers at large also smile on these household names: According to Brand Finance, Google (including YouTube) became the most valuable brand in the world in 2017; Facebook, after also rising steadily, shot up to number nine.

Unsurprisingly, the two firms are outperforming the buoyant S&P 500—indeed, are “pulling it up” through passive indexes: Over the past year, Facebook shares are up 47%, Google shares are up 39%, and the S&P 500 is up 25%.

Investors are paying a premium for these stocks any way you slice it. On a price-to-earnings basis, both Google (ttm P/E: 39.1) and Facebook (ttm P/E: 36.6) are roughly 40% more expensive than the S&P 500 (ttm P/E: 23.3). On a price-to-sales basis, thanks to their high profit margins, the sticker shock is bigger: Here, Google (ttm P/S: 8.0) and Facebook (ttm P/S: 15.3) are 240% and 550% more expensive, respectively, than the S&P 500 (ttm P/S: 2.4).

But these facts alone seriously understate the Google and Facebook premia. The vast majority of high-P/E stocks fit into three familiar bins: (1) relatively small firms with great growth prospects; (2) good firms hitting an earnings rough patch that investors regard as temporary; or (3) great firms that are deliberately trading current earnings for unlimited market share expansion (such as Amazon and Netflix).

Google and Facebook are none of the above. They are massive, highly profitable, and highly valued juggernauts expected to become ever more massive and profitable over time. That makes them a rarity. In fact, if you just look at nonfinancial companies with over $100 billion in market cap and over $10 billion in earnings, the only other company in their P/E territory is Microsoft. To some extent, Microsoft is recovering from a rough patch. More to the point (the significance of which we shall see shortly), Microsoft is not in the ad sales business.

WHAT INVESTORS EXPECT

Investors have clearly priced in the expectation that these companies’ sales are poised to skyrocket over the coming years. (Let that sink in: When you buy Facebook, you’re paying $15 for every one dollar in current sales!)

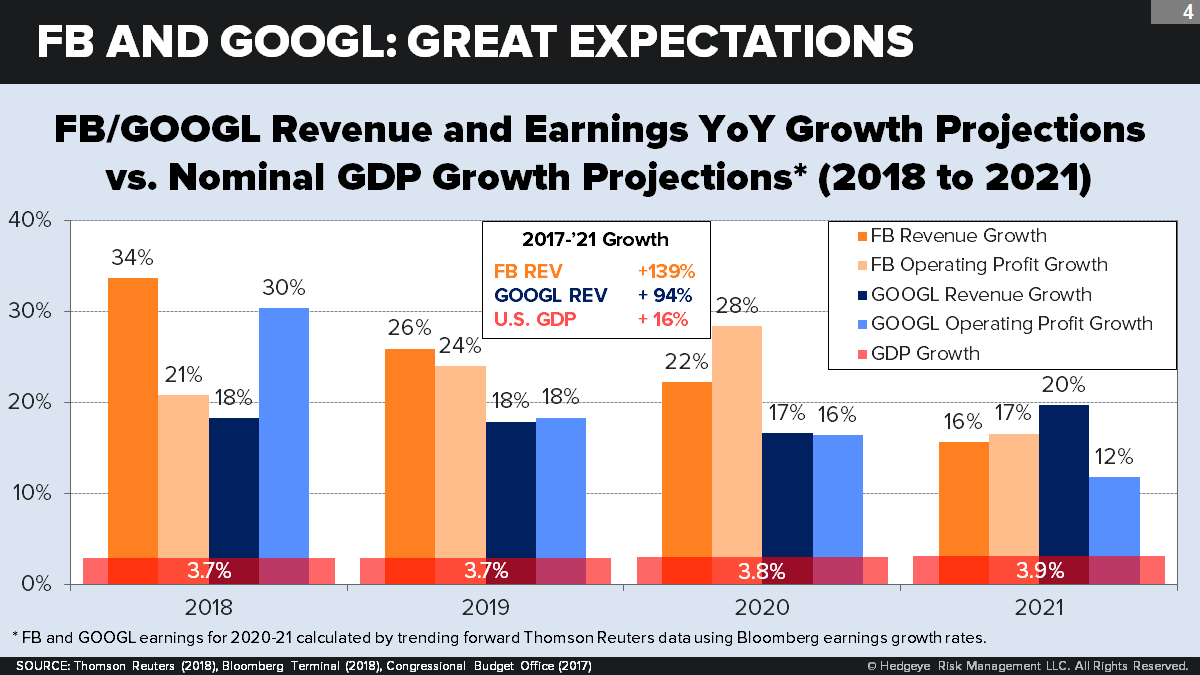

So let’s take a closer look at exactly what they expect. A Bloomberg roundup of consensus estimates indicates that Google’s revenue is projected to grow to $173 billion by 2021. Considering that Google earned 89% of its revenue from advertising in 2016, this projection implies that the company will generate $152 billion in ad revenue in 2021.

Let’s run through the same logic for Facebook. The company is projected to earn $96 billion in total advertising revenue by 2021. Considering that Facebook earned 97% of its total revenue from advertising in 2016, this projection translatea into $93 billion in ad revenue in 2021.

Are these projections feasible? It’s hard to imagine so. They imply that Google’s sales will grow at a CAGR of 14% from 2016 to 2021, while Facebook’s sales will grow at a CAGR of 28%. By comparison, the latest Congressional Budget Office projection shows U.S. GDP growing at just 3.6% nominally over the same period. Do you really trust Facebook to grow more than seven times faster than the U.S. economy for the foreseeable future?

The consensus doesn’t indicate where geographically this revenue will come from. But let’s assume that the current mix of U.S. versus global revenue holds steady through 2021. (We’ll return to this assumption later.)

As of 2016, Google earns $29 billion of its ad revenue from the U.S. market, or roughly 40% of its total ad revenue. (The company doesn’t break down its ad revenue by geography in its earnings reports.) We’ll infer, using the above growth rates, that Google is expected to generate $56.5 billion in U.S. ad dollars in 2021. Facebook, meanwhile, earns $12 billion of its ad revenue from the U.S. market, or 46% of its total revenue. Here again we’ll infer that Facebook is expected to generate $42.9 billion in U.S. ad dollars in 2021. Combined, the two companies must earn $99 billion from their U.S. ad businesses to satisfy the consensus.

The above projections, daunting as they are, rely on a number of problematic bets by the consensus. Will revenues abroad keep pace with revenues in North America? (Last year, they didn’t.) Will profit margins stay rock-solid over time? (In recent years, they haven’t.) Will social and political wild cards continue to favor the industry? (Go to Google Trends and type in “tech-lash.”) Yes, we will return to all of the above.

WHY THE BULLS ARE WRONG

There are three basic dynamics that we must assess. In order for Google and Facebook to hit these growth targets, investors must be expecting one, two, or even all three of the following dynamics to take place:

A) Google and Facebook will squeeze out all of their digital competitors.

B) Digital ad spending will rise rapidly as a share of total ad spending.

C) Total ad spending will grow rapidly as a share of GDP.

As we will soon see, none of these dynamics are likely on their own. What’s more, no plausible combination of these dynamics will provide enough revenue growth to justify the optimistic projections of the bulls.

We’ll discuss this first in the context of the all-important U.S. market. Later, we’ll come back to the question of whether a shortfall in U.S. revenue can be compensated for by positive surprises in the rest of the world.

DYNAMIC #1: GOOGLE AND FACEBOOK TAKE OVER DIGITAL

First, let’s tackle the proposition that Google and Facebook could simply grow their market share within the U.S. digital ad space. In 2016, they owned 59% of it. That still leaves a sizable chunk of the market that they could theoretically wrest from the hands of Microsoft, Amazon, Twitter, and the rest of their digital media foes. Lately, they’ve been blowing away market-share projections (like those of eMarketer) to the upside. Is there really any stopping them?

Let’s investigate.

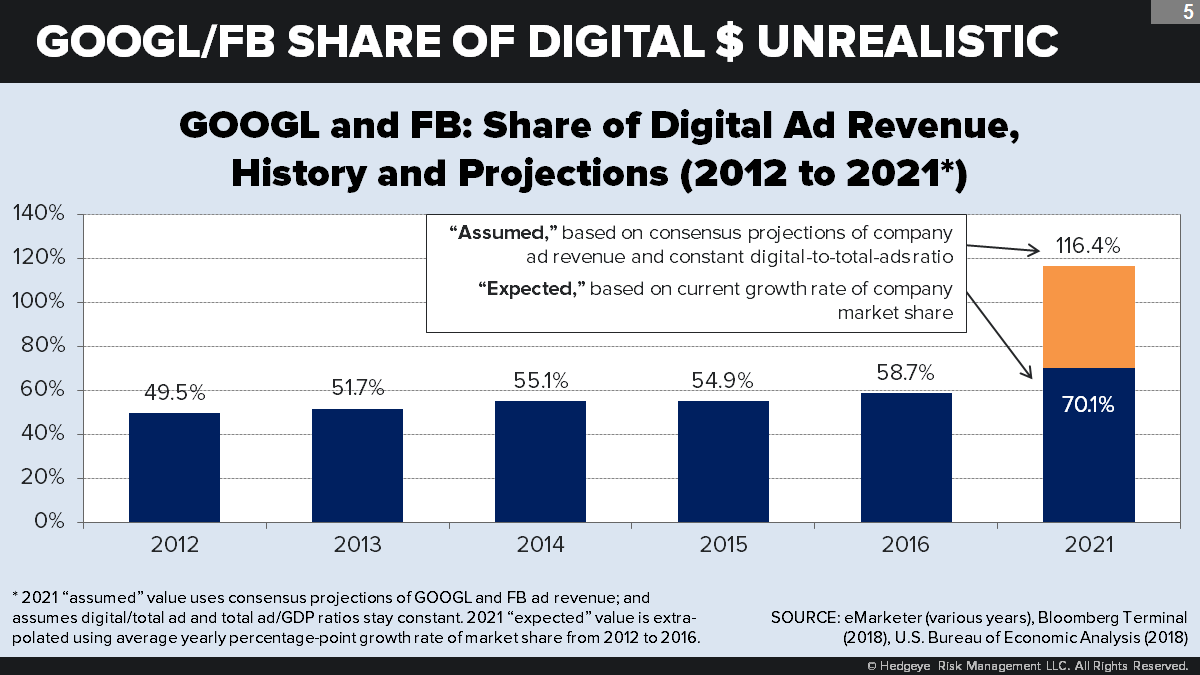

We’ll first assume that Google and Facebook continue to grow their market share within the digital advertising space at the same average rate as over the past four years (2.3 percentage points per year, 2012-16). At that rate, these companies would have a 70% market share by 2021. (eMarketer currently projects around 71%.)

The question then becomes: 70% of what? If we assume that the digital ad universe grows at the same rate as GDP, the digital market will be worth $86 billion in 2021. That equates to a combined $60 billion in U.S. ad revenue for Google and Facebook.

But $60 billion comes nowhere near the $99 billion that the consensus expects these two companies to generate on their own. Assuming a universe constrained by GDP growth, in fact, Google and Facebook would fall short even if they captured 100% of the digital advertising market. They would have to gobble up 116% of U.S. digital ad revenue. Logically impossible.

In fact, it may even be optimistic to assume that these companies will continue growing at their current rate. Will they even be able to hit 70% of the market? Maybe not.

Keep in mind that the lion’s share of these firms’ ad revenue (nearly three-quarters of Google’s and virtually all of Facebook’s) comes through user entry to their websites (e.g., AdWords on Google Search or Chrome). This means that ad revenue is critically linked to website use. For many years, the two firms drove up revenue in part by growing the share of all online persons who use their sites.

But recently those shares in the United States have pretty much plateaued. Google now handles around 65% of all search queries and 93% of all mobile search queries—shares that are no longer climbing. Between 70% and 80% of online adults now use Facebook, a share which also seems close to saturation. (Tellingly, Facebook’s growth in the last few years is almost entirely due to Boomers age 65+ “catching up” and signing on.) Media traffic referral by the two firms, after strong recent growth from Facebook, has similarly stabilized at around 75%.

Google and Facebook could compensate by loading more ads on each user, but of course that would endanger the all-important “user experience.” Facebook CFO Dave Wehner has been warning for well over a year that his folks have pretty much packed as much ad content as they can onto News Feeds, even as Facebook thrusts “Ad Breaks” into the middle of its organic videos—and Google dumps tons of ads into its once ad-lite YouTube.

Finally, just last month, Facebook announced a major retreat on ad placement density, with Mark Zuckerberg confessing: “Recently we’ve gotten feedback from our community that public content—posts from businesses, brands and media—is crowding out the personal moments that lead us to connect more with each other.” Ya think?

Sure, Google and Facebook can and do persuade advertisers to pay more per impression by touting their superior consumer data and targeting algorithms. But it’s impossible to keep growing that margin every year or, for that matter, to get advertisers to keep paying for that margin.

Perhaps mindful of how little energy they can afford to waste if they want to steamroll their remaining rivals, Google and Facebook are trying to become well-behaved duopolists by no longer competing much against each other: Google has given up dabbling in social; Facebook has quit experimenting in search. Instead, they worry together about rebel digital outposts that refuse to shrink on schedule and that dare to defy their death star. These include small but devoted social media communities like Twitter, Snapchat, Spotify, and Yelp. Or digital subsidiaries of telecom giants like Verizon (Oath) or Comcast (FreeWheel, Spotlight).

One competitor hardly anyone suspects may yet pose a serious threat to Google and Facebook: Amazon. Google is well aware of the danger: In 2014, Google Executive Chairman Eric Schmidt said that, “Many people think our main competition is Bing or Yahoo. But really, our biggest Search competitor is Amazon.” According to a 2016 PowerReviews survey, 38% of online shoppers start their product search on Amazon, higher than the share that starts on Google (35%). Amazon is reported to be developing a free, ad-supported version of Amazon Prime. And in voice command, Echo certainly got the jump on Home.

A recent Morgan Stanley report predicts that by 2020 Amazon will be earning $7 billion in ad revenue—seven times what it earns today and roughly 6% of the projected U.S. digital market. If Amazon expands at this pace, Google and Facebook will need all the other digital competitors to shrink even faster.

Amazon points to a bigger challenge for Google in particular. On today’s Internet, every site wants to be sticky, immersive, and tribal, packed with so much functionality that consumers never have to leave. This evolution of Internet sites into a medieval crazy quilt of walled gardens is uniformly negative for Google, which relies on a vast and uniform webiverse to lubricate its search engines. (Facebook, on the other hand, embraces its obsessive walled-garden identity: See “Is the Public Square Disintegrating?”)

The trend is exacerbated by the shift to mobile, which tends to push user activity into “apps” that break from the Web and are often invisible to Google. It also pushes a large share of the most profitable U.S. users onto iOS platforms, which enables Apple to extort a rent from Google in return for privileging users with easy access to Google features. (Insiders suspect that the biggest driver of Google’s rising TAC is a massive $3 billion payment to Apple in 2017 in return for incorporating Google’s search engine inside Safari—up from $1 billion in 2014.)

The trend also compels Google to prioritize ad exchanges like DoubleClick or AdSense that place “programmatic” on participating websites. It’s a profitable business, but not as profitable as AdWords. (Another reason for rising TAC.) Moreover, many advertisers are starting to fight back by demanding lower commissions and more transparent metrics to judge the efficacy of their campaigns. In a world where Amazon charges just one penny per 1,000 ad impressions achieved through its header exchange, the 5% cut that Google commands for its Exchange Bidding program is prohibitive. Increasingly, brands like Fiat Chrysler are even developing their own metrics to measure their campaigns.

Finally, one can’t help but notice a sort of reductio ad absurdum in the specter of Google and Facebook draining all the revenue out of digital advertising. Keep in mind that these firms produce little premium content on their own, making them by and large parasitical off the TV, film, news, and radio organizations that do. If digital’s ad-dependent content firms continue to sink into the red, how much content will be left to “feed” these giants with anything worth seeing?

News journalism, in particular, has over the last two decades been decimated by revenue losses. When nearly 2,000 news outlets last year organized into the “News Media Alliance” and sought permission from Congress to negotiate ad prices jointly, Google and Facebook were compelled to adopt a conciliatory response—lest their feedstock be reduced to nothing but fake news and kitten GIFs. Even a parasite needs to keep its host alive. (A growing number of hosts are choosing to rid the parasite by shifting to a “paywall” business model, a topic we will return to.)

Do the arithmetic: In 2016, major search and social media platforms took in 73% of all digital revenue (59% of that went to Google and Facebook; the other 14% went to Microsoft, Yelp, Twitter, Amazon, etc.) That left 27% of digital revenue going mainly to print, TV, movie, and gaming content producers. By 2021, assuming that the big duo hits their projected 70% of the total—and that the other platforms (including Amazon) remains at 14%—we would see the content share squeezed down to 16%. This implies a catastrophic revenue shrinkage for most content. Could we really imagine Google and Facebook doing even better—and hitting a 75% or 80% market share?

Now let’s summarize. Yes, it is certain that Google and Facebook will continue to grow as a share of all digital advertising. But will their rate of market-share growth dramatically accelerate relative to the post-2012 trend—as the bullish projections imply? Not likely. In fact, the firms may do well to just keep gaining market share at an unchanged pace. That will bring revenues nowhere near projections.

But what if the entire digital market were to grow, thereby boosting the available revenue for these firms?

DYNAMIC #2: DIGITAL ADS TAKE OVER TOTAL ADS

If digital ads were to push all other ad formats to the margins, it would clearly benefit Google and Facebook. Is this a realistic proposition? Let’s find out.

Digital advertising’s market share grew by an average of 3.6 percentage points per year from 2012-‘16. Assuming that this growth rate holds steady, digital will reach 55% of the total ad market by 2021.

This gain isn’t nearly enough to create the kind of revenue growth that investors are projecting. Assuming that total ad spending keeps growing at the same rate as GDP, it will reach $234 billion by 2021. Thus, in order for Google and Facebook to earn $99 billion in U.S. ad revenue thanks solely to a surge in digital advertising, the space would have to capture 72% of all ad spending in 2021.

Such meteoric growth in a new medium’s share of the total ad market would be historically unprecedented. Going back a century, whenever a new advertising medium emerges, it grows as a share of all advertising in a second-derivative concave-up pattern—yet quickly hits an inflection point, at which point its growth turns concave-down. In other words, a new medium grows quickly upon its introduction, but within a few years, it starts to grow more slowly before eventually stabilizing at its new share of the pie. Right now, Internet advertising revenue is beginning to shift from concave-up to linear—which suggests that it will soon turn concave-down.

Digital advertising’s recent concave-up growth phase can be explained in part by Nielsen data showing a massive rise in the time Americans spend consuming digital content. Even as time spent watching linear TV continues to decline gradually, overall U.S. screen time has exploded, thanks to a huge recent increase in digital media usage. The average American now spends two and a half hours per day surfing the Web on their smartphone—a more than doubling in just two years. In all, Nielsen reports that consumers spend roughly two-thirds of their waking lives (10 hours and 49 minutes per day) consuming content on some type of media. That’s an 18% rise in the total time spent with media in just two years’ time.

These data should give the bulls pause, because they imply that their forecasts have been misled by the recent past. The last two years cannot be extrapolated as a trend line for future growth—even if we concede that Nielsen’s numbers may be inflated by the prevalence of multitasking and second-screening. Such an extrapolation would soon imply more daily time spent with media than Americans are awake. Quite simply, Google and Facebook have been reaping the benefits of a once-in-a-lifetime shift in the way that Americans consume content. Indeed, the personal and social harms caused by screen-time addiction have already ignited a “tech-lash” that may redound badly for Google and Facebook on many fronts (more on that later).

Some analysts have begun to grasp the negative implications of this steep rise in digital use. In the words of Brian Wieser, senior analyst at Pivotal Research, “Digital advertising will soon be approaching a point of saturation, indicating that there are limits to growth which may not be fully accounted for by the investment community.”

Bulls will undoubtedly say this time is different. After all, digital ads are so much more efficient and granular in targeting consumers than, say, ads on radio or linear TV. Why couldn’t they crush everything else in sight?

Well, we must first mention that every new medium seems futuristic compared to the ones that came before it. Radio seemed infinitely more effective than a print newspaper ad, while TV seemed infinitely more effective than a radio ad. And yet none of those mediums suddenly disappeared when a new one was introduced.

In reality, the efficacy of any ad depends on its context—which explains why there is still a robust market for billboard ads. Not even a digital ad delivered directly to an individual’s pocket can beat a billboard ad when that individual is driving down the highway or hurrying to catch a plane. Likewise, despite the rapid growth of e-commerce and mobile IT, Census data show that 91% of all retail dollars are still spent in a brick-and-mortar store—which is becoming its own hotbed of out-of-home advertising, thanks to the proliferation of omnichannel shopping and beacon technology. (See: “Tracking Shoppers, Boosting Sales.”)

Are there other more specific reasons to question the unstoppable advance of digital? Here are three.

Reason #1: Ad blocking. Unseen digital ads are useless, and the recent explosion in ad-blocking technology is doing just that: blocking people from seeing them. From January 2013 to January 2017, the number of global desktops using ad blockers has grown at a 46% CAGR. The global growth in mobile ad blockers is even steeper: 62% CAGR over the last two years. The spread of ad blockers, costing U.S. digital advertisers an estimated $10 billion this year, clearly terrifies the industry since use of ad blocking in North America lags way behind the developing world. Once the United States catches up, the industry’s cash cow could be in danger.

Google and Facebook are leading the response to ad blocking on a number of fronts. They are engaged in a high-tech arms race to “block” the blockers—which typically generates only temporary victories. They are lobbying to forestall adverse regulations, such as a terrifying EU proposal (tabled for now) that would make it illegal for publishers to detect users’ ad blockers. They are literally paying off big ad blockers like Adblock Plus to get them to “filter in” their own ads. And they’re trying to co-opt the ad blockers by inventing their own digital ad whitelist and their own ad-blocking software. (Chrome is introducing its own ad blocker this month.)

Reason #2: Misguided ad targeting. The very strength of digital ad programming (precise targeting via big data and AI algorithms) is also its biggest weakness—namely, that there are no humans involved. This leads to widespread bot or click fraud, acknowledged by everyone in the industry as an as-yet unsolved problem. Google is routinely settling multimillion-dollar “invalid traffic” court cases against irate advertisers. Estimates of total fraud vary, but one frequently cited number (low-balled by an industry-friendly group) is an astounding $6.5 billion in 2017.

Beyond outright fraud, advertisers worry about how digital’s complex distribution system is utterly nontransparent and threatens “brand safety” (ads mindlessly juxtaposed with unsavory content or fake news). JPMorgan recently announced that it will restrict its ads to “human-checked” YouTube channels. So much for "programmatic."

Reason #3: Nondigital strikes back. Yet if programmatic does indeed have a downside, nondigital media is beginning to take advantage of digital’s upside. Let this be reason number three. The big TV and radio networks are no longer bound to “dumb” age-and-sex Nielsen categories. Viacom, NBC, Time-Warner, and Disney are all now pitching advertisers on micro-targeted ads via OTT, cable, and VOD distributions. In 2017, rival networks started to create joint systems allowing advertisers to place targeted ads across networks (Turner, Fox, and Viacom under OpenAP and ABC, CBS, Fox, Discovery, A+E, and others under Thor). Later this year, Next Gen TV (just approved by the FCC) will allow any TV to be individually addressable.

According to NBC’s head of ad sales, “This is giving marketers the targeting they crave with premium content. They thought they were getting that with digital, but it didn’t quite work out… Clients want to be in a great premium environment that is safe, legitimate, and trustworthy, but can also deliver on business goals.” eMarketer expects U.S. spending on addressable TV ads to more than double to $3 billion by 2019. Nowadays, using TV ads alone, firms like Simulmedia and OpenAP are helping a brand like L’Oréal target a consumer segment as granular as women who bought lipstick from certain retailers in the past month.

Largely due to these new initiatives, ad analysts are ramping up their TV revenue forecasts. Credit Suisse now projects that TV ad spending ($71 billion in 2016) will roughly double by 2030 and hardly decline at all (remain at 35%) as a share of total ad spending. If Credit Suisse is even close, growth in the digital share will be decelerating dramatically.

In sum, Google and Facebook are destined to compete not only with digital competitors in pursuit of ad dollars—but also with new and old “content” media that people have already written off.

OK, so let’s rule out endless growth in the digital ad share. What’s left? The only other way that analysts’ revenue expectations would be reasonable is if total ad spending grows faster than GDP.

DYNAMIC #3: TOTAL ADS RISE AS A SHARE OF GDP

Let’s assume, as we’ve conceded in the earlier sections, that Google and Facebook do grow per their recent trend as a share of digital advertising, and that digital advertising does likewise as a share of total advertising.

As it turns out, this still doesn’t allow us to get to a scenario in which Google and Facebook earn enough from ads to justify their current price, because we’ve constrained ad spending as a share of GDP. In 2021, if ad spending grows on pace with GDP, it will reach $234 billion, or 1.04% of nominal GDP as forecasted by the CBO.

How much would ad spending have to rise as a share of GDP to get these projections to work? For Google and Facebook to generate $99 billion in U.S. ad dollars in 2021 thanks solely to a rise in total ad spending, the ad universe would have to grow to $462 billion—or 2.05% of GDP. That’s double 2016’s share.

History shows that this level of ad spending is without historical precedent. Over the past century, ad spending has averaged just 1.3% of GDP, with little variation. One could say, in fact, that ad spending and GDP are inextricably bound: This ratio has never strayed so much as half a percentage point in either direction—even with such jolts as the rise of radio, the Great Depression, World War II, the emergence of television, and most recently the dawn of the Internet Age.

What explains this constancy? Apparently, either the supply or the demand for advertising has a unitary elasticity with respect to price—so that a percentage decline in the cost of targeting customers (e.g., due to technological improvements or rising population density) is roughly matched by a similar percentage increase in spending per target.

In any case, we have never seen 2.1% of GDP before. The previous record (an anomaly triggered by the collapse of GDP at the peak of the Great Depression) was 1.7% in 1932. The next-highest peak, just over 1.5% in 2000, was an outgrowth of the dot-com bubble.

There’s no reason to expect this unyielding relationship to change. Ad spending certainly won’t break upward in the near term. If anything, ad spending has been trending lower than the historical average lately: Since the Great Recession, the ratio has hovered just over 1% (it’s at 1.04% today)—and shows no sign of reverting back above its long-term average late in the business cycle.

The Economist recently noted that “something doesn’t ad up [sic] about America’s advertising market”—namely, that “stockmarket investors are wrong to expect an enormous surge in advertising revenues.” Indeed. Expecting ad spending to suddenly turn about and double in the next few years as a share of GDP is sheer fantasy.

BUT WHAT IF…

OK, so no dynamic on its own could possibly result in Google and Facebook earning enough revenue to justify their prices. But bulls of these Internet stocks will ask: Why not a little of all three? Surely, some combination of the three dynamics could raise the companies’ revenue to sufficient levels.

Our answer would be that there’s no plausible combination of the first two dynamics—Google and Facebook expanding as a share of digital ads, and digital ads expanding as a share of total ads—that would justify the revenue projections.

Let’s say for argument’s sake that Google and Facebook continue to grow as fast as they have within the U.S. digital ad market since 2012. In that case, they would earn 70% of all digital ad revenue by 2021.

But as we have seen, 70% doesn’t mesh with investor expectations. It implies that, in order for Google and Facebook to meet their $99 billion combined revenue projections, the digital advertising universe must grow from 37% of total advertising in 2016 to 61% in 2021. In other words, digital advertising would have to grow roughly 5 percentage points per year—something that’s never happened in any single year since the dawn of the Internet.

As for the third dynamic—total ad spending as a share of GDP—it is unlikely that this could play a positive role given the historical stability of the ads-to-GDP ratio. Indeed, as we shall see a bit later, this ratio may be more likely to decline in future years as it is to rise.

COUNTERARGUMENTS… COUNTERED

There will naturally be plenty of pushback to the idea that Google and Facebook, two of the leaders of the Internet Age, are not worth the price of admission. What could the bulls say? Let’s take on three arguments in order of plausibility, from most to least.

“Just wait until we bring the next billion online.” In other words, Google and (especially) Facebook will be rescued from any domestic slowdown by accelerating revenue gains abroad. This is certainly the bulls’ best argument. After all, both firms are well established on the world stage. And it’s hard to be rigorously quantitative about markets that range from Columbia to Bangladesh. You’re tempted to just wave your hands and say, wow, there’s a lot going on.

We should note for starters, however, that over the last several years, revenues abroad for neither company are growing any faster than revenues at home. For Google, the U.S. share of total revenue (their 10-Qs don’t break out just ad revenue) actually rose from 44% in Q4 2013 to 48% in Q4 2017. For Facebook, the North American share has also been steady at around 49% since 2014.

Why? Well, in most of the high-income world (Europe, developed East Asia) and relatively affluent Latin American nations (Mexico, Brazil), Google and Facebook have already attained such high penetration (e.g., Google controls a stunning 92% of Europe’s search engine market) that the number of users there aren’t growing any faster than they are at home.

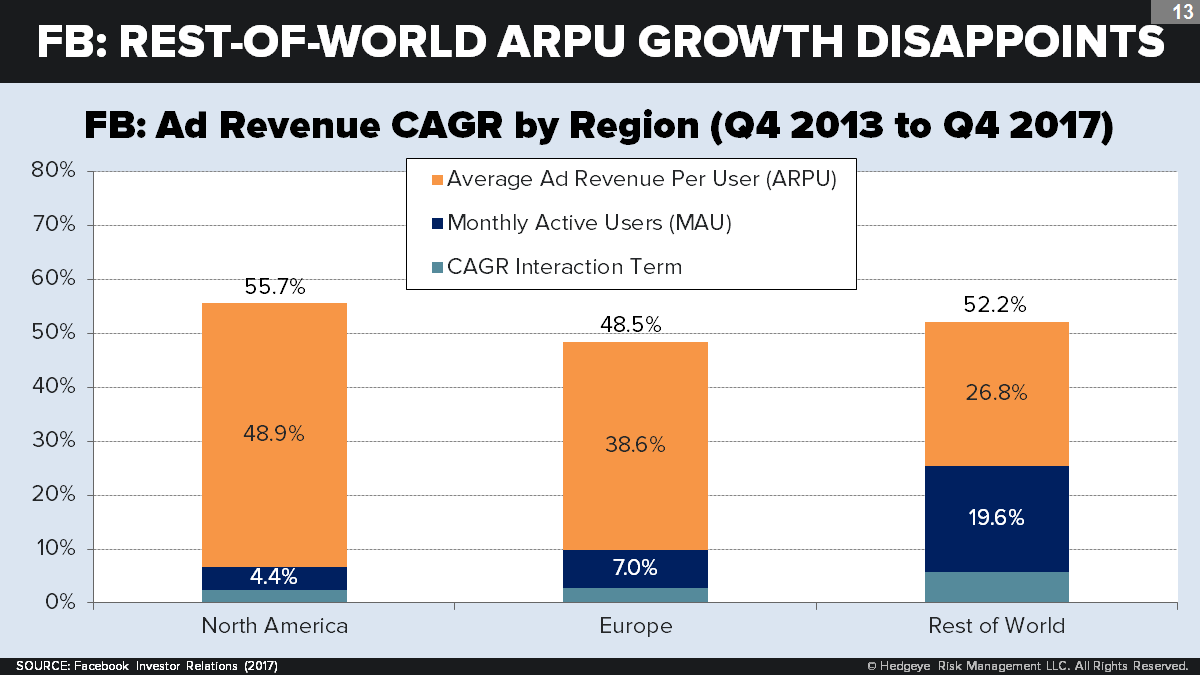

In the less affluent emerging and frontier markets, users are indeed growing much faster. Monthly active Facebook users (MAU) for the “rest of the world” outside of North America and Europe have grown at 20% CAGR over the last four years—versus 4% for North America and 7% for Europe. But that’s being offset by a commensurately lower growth rate in average ad revenue per user (ARPU)—which is 27% in the rest of the world, 49% in North America, and 39% in Europe. This is probably happening because the most affluent and connected persons in (say) Vietnam and Pakistan are the first to sign up, and further recruits are progressively poorer and less connected.

Achieving any digital profitability in most of these societies is in fact problematic. Average per-capita consumption in Africa, South Asia, and Southeast Asia (less than $4,000 nominal) is typically about 10% of the U.S. level. After subtracting out food, rent, and nontradable services, cash available for digitally swayable spending is about 5% of the U.S. level. Due to incomplete penetration that favors the more affluent, Facebook is still doing better than that: Its Asia-Pacific ARPU ($2.54) is just under 10% of its North American ARPU ($26.26). But as penetration deepens, that ratio will keep falling.

Facebook has often claimed, as a sort of mission statement, that “user growth in the future will be primarily concentrated” in these low-ARPU regions. (It said as much in its 10-K SEC filing for 2017.) The company has been less open about the enormous difficulties of profiting from such growth. Beyond simply consumers not having much money to spend on advertised items, these challenges include unreliable electricity, limited literacy, unaffordable data services, inadequate mobile phones (desktops are rare), and disinterest by most domestic producers in digital advertising. Mobile ad blockers (to spare low-income users the time and cost of downloading irrelevant ad code) are vastly more prevalent in Indonesia and India than in North America.

Facebook does not publish its costs or capex by region. But according to Caribou Digital, Facebook may already be losing money in many low-ARPU nations, including India, Indonesia, Philippines, and pretty much all of Africa. And this is before Facebook even launches its giant Internet-beaming drones over Nigeria. Rising cost and declining revenue per additional MAU is not an obvious formula for success.

If China—which currently blocks both Google and Facebook—were to suddenly change its mind, that could improve the duo’s prospects abroad. But Chairman Xi is very unlikely to reverse course (despite obsequious courting by Mark Zuckerberg)—and in any event Baidu, Weibo, Tencent, and Alibaba would be tough competitors. Breakthroughs in other countries with tough cultural or political barriers to American social media (e.g., Japan and Russia) would also help.

But the global populist and authoritarian tide seems actually to be pushing in the other direction. It is pushing back on the presumption that Silicon Valley globalism gets to write all the rules. (We will return to this topic later.) Sure, go ahead and bring on the next billion—but be careful what you wish for.

“Just wait until the moonshots land.” Here’s where the real fanboys come in, the ones who say that Google and Facebook are about so much more than ad revenue. After all, listen to their slogans: These companies are doing no evil, connecting us all together, and making knowledge universally accessible and useful. Along the way, they are creating artificial super-intelligence (Google’s DeepMind), joining people’s hands virtually (Facebook’s Oculus VR), and even making the old grow younger (Google’s Calico Labs). Surely one or more of these nascent pursuits ought to become seriously profitable, right?

Maybe. But again we need a reality check: Despite all the media hoopla, none of what Google calls its “moonshot projects” or “other bets” (from self-driving cars, Internet balloons, and robots to AI, longevity science, and new-fangled heat pumps) has yet to generate serious revenue. Altogether, these amounted to $302 million in Q3 2017, or 1.1% of total Google revenues. And since expenses exceeded revenues by 3-to-1, the moonshots are not even close to overall profitability. Google’s new CFO Ruth Porat, charged with making all divisions accountable under the new “Alphabet” rubric, made headlines last year for scaling back on many of them.

Google does earn plenty of revenue—about 15% of its total—from activities other than advertising. But most of this is from its cloud computing business. It got into cloud because it found itself with lots of spare servers and memory, not because it possessed any special edge in cloud technology or software. Most industry observers agree that Google trails Amazon and Microsoft in cloud adoption by a wide margin. It would be dangerous to assume that cloud alone could save Google.

Facebook, meanwhile, is even more ad-dependent than Google, earning a staggering 99% of its Q4 2017 revenue from advertising. As far as non-ad projects go for Facebook, the lineup is sparse, consisting solely of Oculus VR and a few other rumored hardware projects that have yet to be announced.

Of course, the argument could be made that the resource underlying all of these disparate bets—user data—has plenty of value on its own. It’s no secret that Google and Facebook have amassed breathtaking amounts of data over the years: All told, Google may hold as much as 15 exabytes of data, or the combined memory capacity of 30 million PCs. Surely the very ownership of all this data is reason enough to pay a premium for these companies, right?

This would make sense if the data had vast untapped potential that is unrealized by markets. But Google and Facebook already are generating plenty of revenue on this data by selling it to advertisers. It’s why you may see ads for official NFL jerseys if you recently Googled the score of the big game, or why your News Feed may be filled with Ticketmaster offers if you recently liked the Facebook page of your favorite band.

What’s more, consumer sentiment is starting to turn against these companies’ unfettered access to user data: Navigating the Web in secrecy without the oversight of Google or Facebook has practically become its own lifestyle. More radically, some economists contend that tech giants aka “data refineries” should start paying users for access to coveted personal information—in effect, compensating users for renting their IP. At best, the revenue-generating potential of user data is already being realized. At worst, data may soon become a liability.

If Facebook is more likely to look at faster global growth as its deus ex machina, Google is more likely to look at jaw-dropping tech breakthroughs. While Facebook’s argument falls short, it’s more respectable than Google’s. No one ever thought it made sense to up-value a giant conglomerate like GE or Textron based on some new idea it is incubating that is neither profitable, nor at scale, nor related to its main business. It makes no sense here, either.

It is a measure of the idealism (or hubris) of these firms’ leadership that, with ample funds to invest, they can’t identify projects more directly connected to their economic model. In particular, they remain almost entirely dependent on other firms to supply them with the premium news, data, and entertainment content without which they cannot survive. They’ve invested little in trying to relieve that dependence. Instead, they’ve allowed other firms—like Amazon, Netflix, Bloomberg, Verizon, Disney, and others—to get way out ahead of them. Someday, they may come to regret that choice.

“Just wait until Google and Facebook are all there is.” Late last year, technologist Andre Staltz created a stir by publishing a post entitled, “The Web Began Dying in 2014, Here’s How.” Staltz’s premise is that, as a rising share of users access the Web through Google and Facebook, a tipping point will be reached when most users no longer care much about accessing it any other way. Already, he points out, Google (through AMP) and Facebook (through Instant Articles) are pulling content into their own sites and onto their own servers. Ultimately, neither service wants to be a web “site” at all—but rather a total environment that users never have to leave.

In weird synchrony with Staltz’s scenario, governments around the world are lately showing declining interest in net neutrality. This is true not just in the United States (where President Trump’s new FCC Commission recently repealed net neutrality rules), but even more so around the rest of the world, especially in EMs, where ISPs are moving toward zero-rated or pay-for-play plans like Facebook Zero or Google Free Zone that restrict or funnel users toward privileged sites. Google is no longer showing its old enthusiasm about lobbying in favor of net neutrality, possibly because it knows it will be “dealt in” on any essential ISP package.

Ultimately, Stultz suggests, we may arrive at a dystopia in which the Web sort of withers away (available only with difficulty, perhaps, to the very curious). In its place, there will be simply the “Trinet”—Google, Facebook, and Amazon. Presumably, all digital ad revenue, and even some paywall revenue, will flow through this troika.

It’s an ambitious and intriguing scenario. And stated this baldly, it seems to be a clear win for Google and Facebook.

Yet the story’s plausibility breaks down critically in two places. First, despite the FCC repeal, it is not true that net neutrality is about to perish in the United States. Surveys show it is overwhelmingly supported by Americans—who still set the tone for the world on this issue. (See: “Net Neutrality Is Dead, or Is It?”)

Second, if net neutrality were to perish and if Google and Facebook thereby became obvious monopolies, they would almost certainly become regulated monopolies, subject to a full monte of content rules and common carrier price-and-entry regulation. Once again, an apparent win would become a loss. As we’ll see shortly, the threat of increasing government control surely worries the firms’ leadership even without the end of net neutrality. Stultz’s vision, in other words, could be a dystopia for Google and Facebook most of all.

HOW THINGS COULD GET EVEN WORSE FOR GOOGLE AND FACEBOOK

The core arguments presented above show why Google and Facebook are unlikely to grow at a sufficient rate to satisfy expectations. But it doesn’t end there. There are several possible scenarios that, if played out, throw further doubt on the current valuation of these Internet giants.

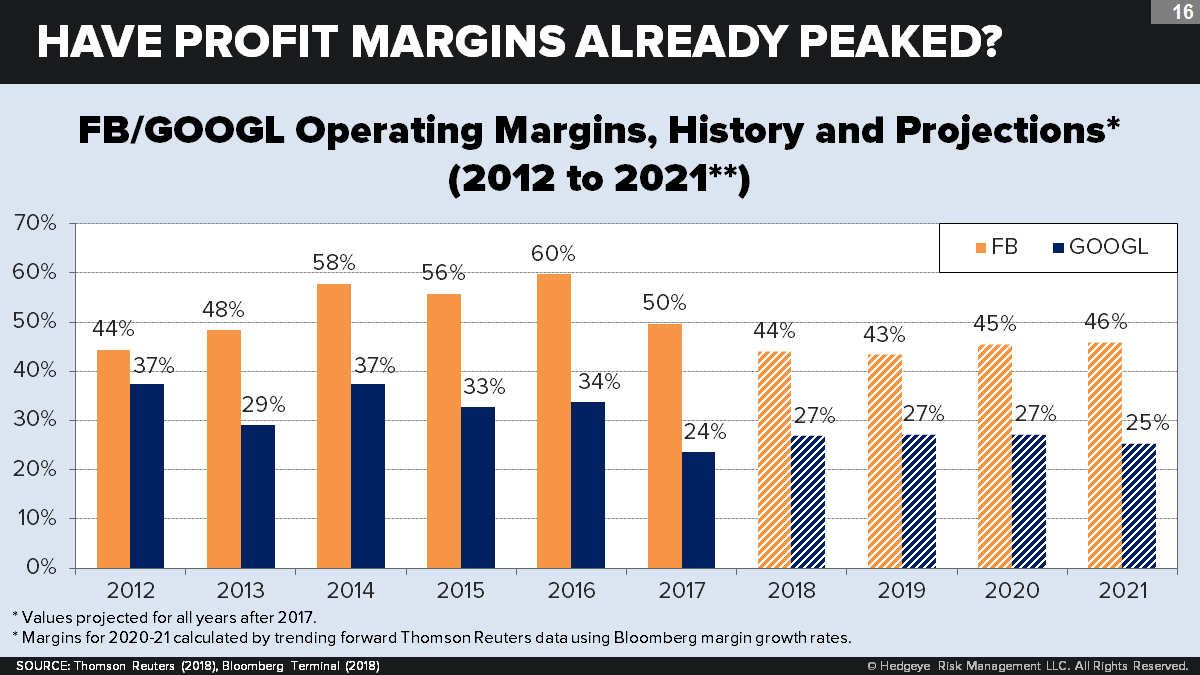

Profit margins compress. The consensus earnings projections for Google and Facebook not only assume rapid revenue growth but also—crucially—high profit margins that do not decline much over many years. In fact, with the 2017 numbers in, the consensus shows virtually no decline in margins over the next four years. Remember: Every one point decline in Google’s future margin translates into roughly a 4% increase in needed revenue by 2021 beyond the consensus forecast.

This may be optimistic. There are few historical examples of giant companies that are able to sustain high profit margins indefinitely while at the same time growing their market share. Inevitably, such companies see their margins erode.

Sure, you can find small companies that accomplish this. Or you can find giant companies that maintain high profit margins without enlarging market share (Apple). Or you can find giant companies that can do all of the above for just a few years. Microsoft, for example, after appearing at #3 in the S&P 500 in 1997, was able to expand its market share and its profit margin until 2000. When the bubble burst, Microsoft hit peak penetration—97% of Internet-connected devices ran on Windows in 2000—while generating an operating margin of around 50%. But thereafter, growing market competition (and a settlement with DOJ) chopped its margin and gradually pulled down its market share (to only 20% by 2012).

Why is it so hard for a market-expanding giant to maintain high margins year after year? Two reasons.

First, growing market share means rising competition, which in turn will force a company to lower its prices. This is especially true in the tech sector, where companies like Amazon and Apple are willing to go without a profit—or even operate at a loss—in order to grow their market share. With prices per click coming down in the digital ad space thanks to growing competitive pressures (see our discussion earlier), it’s getting harder, not easier, for Google and Facebook to turn a profit.

Second, a firm that grows indefinitely nearly always reaches a point when per-unit costs stop declining and start rising. That’s why most industries remain competitive, with many players. Google and Facebook, with their vaunted “network” economies of scale, are supposed to be immune from this effect. But maybe they won’t be.

Gigantic companies are nearly always prone to the hubris and complacency that accompany success—which degrades their efficiency. This is a fact of sociology, not of technology. (It’s surely not cheap to foot the R&D bill for companies that want to usher in a digital utopia, complete with cities run by algorithms and an end to old age.) More seriously, Google and Facebook are about to encounter steeply rising political and regulatory costs associated with their communication dominance (see below). That too is a fact of sociology.

Ad spending shrinks as a share of GDP. We’ve mentioned that ad spending has been trending lower as a share of GDP over the past few years. There are reasons to suspect that this is more than just a temporary blip—but instead could become a long-term headwind for ad-dependent companies.

The most conspicuous challenge for total ad spending is that many of the biggest CPG firms that traditionally spend the most on paid advertising—especially in big food and household staples—are getting hit by flattening sales and shrinking margins. Problem? They face an existential brand equity crisis: Savvy, cost-conscious consumers (with Millennials leading the way) are no longer willing to pay a premium for Jif peanut butter when they could get Walmart’s Great Value brand for 20% less. (See: “The Ebbing of Brand Equity.”) As a result, companies like Unilever and Kraft Heinz have been forced to take the carving knife to their ad budgets: P&G plans to cut its marketing budget by more than $2 billion over the next five years.

This challenge helps explains the recent decline in per-GDP ad spending—and certainly accounts for the current doom and gloom in the ad and marketing agency world. The BI “Global Advertising and Marketing” index, essentially flat since 2013, has not participated at all in the Trump-era boom in the S&P 500. With consumer discretionary surging and a news-packed year coming up (Olympics and a mid-term election), some industry analysts expect an ad-spend rebound in 2018. Even such a rebound, however, may not change the longer-term picture. The forecasters at MAGNA (the research arm of IPG, one of the world's big four ad consortia) does allow for a 4.8% growth spurt this year. But they also expect the CAGR in total U.S. ad revenue from 2016 to 2021 to come in at a dispiriting 2.9%. Yes, that’s well below nominal U.S. GDP growth.

And if there’s a recession? Well, then it gets worse. With rare historical exceptions (such as the early 1930s), ad spending tends to be strongly pro-cyclical. That makes today’s anemic number, at the flush end of an economic recovery, especially worrisome.

Many bulls naturally assume that as ad-targeting technology keeps improving, companies will inevitably spend more on ads over time. But, as we have seen, history shows no such tendency. Both the supply and demand for a perfectly targeted ad have a price-elasticity of approximately negative one—so that better targeting over time proportionally increases the supply of ad inventory and a lower price per target induces a proportionally larger demand for targets. Net result: No change in overall ad revenue per GDP.

And maybe it gets worse. One could imagine a bearish scenario in which rising ad demand no longer compensates for the falling price per target—and total ad revenue craters. This often happens with business inputs experiencing ever-rising efficiency. Think, for example, of PCs and word processors: Lower prices led to commensurately greater demand—until, catastrophically, they didn’t. Imagine a world in which targeting ads to specific individuals is so ubiquitous and inexpensive that its ROI declines relative to a firm’s other marketing activities, such as promotions, word of mouth, earned media, live events, broadcasting, cross-product tie-ins, and so on. That would be bad news indeed for advertising revenue.

While the steam drill was a profitable marvel compared to John Henry, it ultimately meant railroads could spend next to nothing ramming steel into rock.

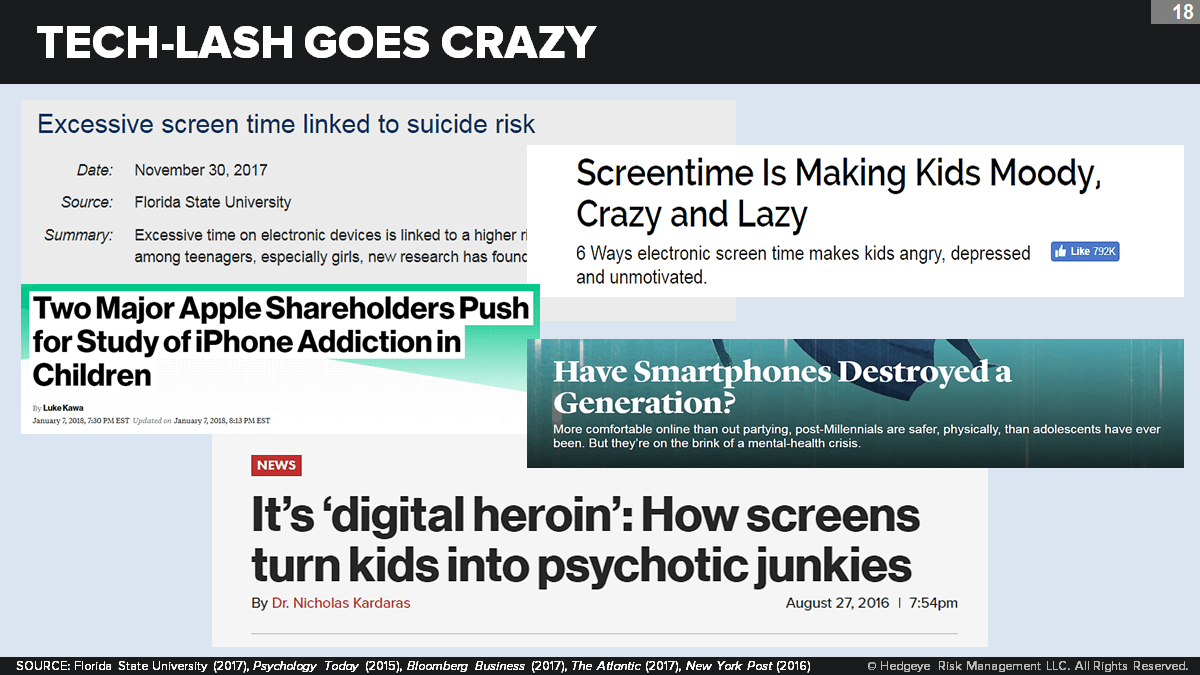

The consumer tech-lash worsens. For Silicon Valley, the bad news about the rapid recent rise in daily digital screen time is that this rise, as we have seen, must decelerate in the near future. But the worse news is that—thanks to a mounting “tech-lash” over the ill effects of so much digital immersion—we might actually see the trend stall entirely. Very few Americans, when asked, think it’s a good idea that adults are spending roughly two-thirds of their waking hours plugged into some kind of media. Or that teens spend almost as long (9 hours per day, as of 2015) plugged into digital media. What if the upward trend not only slows—but flattens out entirely or even noses downward?

It could happen. The roar of negative commentary about growing digital use may indeed reflect an imminent change in popular behavior, perhaps encouraged by new policies (in schools or the workplace) “nudging” people away from digital excess. Digital platforms and social media are increasingly portrayed by concerned parents, media watchdogs, and academic researchers as akin to addictive drugs. They are making us less happy and less social. They are undermining economic productivity. They are blighting children’s imagination. And they are causing mental illness.

The public has been especially alarmed by recent statements from Silicon Valley professionals expressing grave misgivings about their own industry. It is well known that most info-tech executives (“never get high on your own supply”) personally use digital very sparingly. According to one former president of Facebook (who made a fortune as an early investor): “God only knows what it’s doing to our children’s brains.” A former VP of Facebook user growth expressed “tremendous guilt” over his part in “ripping apart the social fabric.” This sudden grim chorus from Facebook alumni was at least as responsible for Facebook’s January 12 correction as the official announcement regarding News Feed.

The public is also alarmed by the impact of rising digital use on their preschool and school-aged children. According to Common Sense Media (as of 2015), “78 percent of teens check their phones at least hourly and 50 percent report feeling ‘addicted’ to their phones.” Jean Twenge’s recent bestseller iGen, which indicts digital media for just about everything wrong with today’s “super-connected kids,” was cited in the recent letter by two institutional investors to Apple requesting that the company do research on the harms it may be causing. The public may not be relieved to learn that Silicon Valley families themselves tend to be restrictive about letting their own kids use digital (often sending them to tech-free Waldorf and Montessori schools).

Beyond a rebellion against rising digital time, an emerging tech-lash is also likely to encompass a rebellion against digital ads. The bearish omen here for Google and Facebook is that aversion to digital ads is highest among the youngest consumers, which may translate into rising aversion overall with each passing year.

Millennials—who have grown up with the instant gratification of DVR, Tinder, and same-day shipping—are especially turned off by digital ads. A recent Millward Brown study found that, when encountering an ad online, 82% of 16- to 19-year-olds will skip it as fast as they can; 51% won’t even see the ad thanks to ad-blocking software. (By comparison, 67% of 35- to 49-year-olds will skip it, while 43% will block it outright.) In 2014, an estimated 21 million Millennials used ad-blocking software, more than double the number of Xers who did so. Declining ad tolerance from younger users may have helped prompt Facebook’s sweeping new shift away from branded content and toward “personal engagement”—even at the cost of less ad revenue. This story may not yet be over.

Yet another bearish sign for Google and Facebook is the emergence of the online paywall economy. Increasingly, consumers are choosing to pay for access to premium content, thus disintermediating the digital ad space. Consider the threat posed by Netflix, a service that gives millions of consumers access to ad-free content. These subscribers have clearly decided that a $7.99 monthly paywall (the cost of a basic plan) is worth the cost. On the Web, more sites are opting to put up a paywall rather than expose visitors to an endless ad barrage.

Paywalls don’t simply starve ad-dependent media networks of viewers. They also threaten to undermine the brands that still rely on ads. As consumers, we’re now used to looking behind paywalls to find elite, aspirational brands—from HBO to The Wall Street Journal to The New York Times. We’re also used to seeing major brands that remain tied to ads sink both in value and profitability—from old media like Time and USA Today to new media like Buzzfeed and Mashable. Over time, this may result in a polarizing bifurcation between creative, high-end, no-ad content attracting the higher-end demographics and bot-generated, low-end, ad-filled content attracting the lower-end demographics.

Down the road, unless they make radical changes in their business model, Google and Facebook may find themselves on the wrong side of this divide.

Political threats arise at home. During their early buoyant growth years, Google and Facebook were pretty much free to build and invent as they pleased. Most political leaders, along with the public, regarded them as market-leading innovators who should be given a wide berth—and their libertarian C-suite largely agreed, blithely assuring the public that what is good for Silicon Valley is good for America.

That era now seems a distant memory. Every month, it seems, we hear politicians, trade associations, and citizen groups expressing shock at what these firms are doing (or not doing) and issuing new demands that they better serve the public interest. What’s the matter? These companies are intruding on privacy. They are violating copyright. They are abetting terrorists and hate groups. They are empowering cyber bullies and cyber attackers. They are profiting off “our” personal data. They are secretive about choices that can bankrupt businesses and ruin reputations. They purvey “fake news” and for a price can help throw a national election.

And, oh yeah, per the tech-lash crowd, they are addicting us all to digital cocaine and basically ending civilization as we know it. All the worsening social and political headwinds were recently summarized by The Economist as the perception that the big tech companies are “BAADD”: Big, anti-competitive, addictive, and anti-democracy.

These complaints are likely to have political consequences. Throughout history, nearly every society has taken a strong collective (and regulatory) interest in how its members disseminate news and information and how they communicate with each other. Even more so when information technology is changing rapidly; when the technology is dominated by one or two very large private agents that seem unresponsive to ordinary market forces; and when populism is on the rise. What we saw back in the late ‘90s and early ‘00s was the historical anomaly. What we see today is not an anomaly.

At the very least, Google and Facebook will have to bear a mounting bureaucratic cost (fact-checkers, mediators, advisors, lawyers) to comply with all the accumulating laws, legal decisions, regulations, and advisory mandates. More likely, they will eventually have to cede some of their discretion to public panels and boards. (They may even invite the cover: If fake news is a national issue, they may figure, why should they be the lightning rod for everything that goes wrong?)

More worrisome to shareholders is the prospect of policies that would impact their revenues: like allowing media and advertisers to negotiate with them in groups; requiring customers and advertisers to opt out of (or be compensated for) sharing data; or paring back the “safe harbor” provisions of the 1998 Digital Millennium Copyright Act that allow the Internet giants to “present” content they do not own.

The possibility of outright antitrust action thus rears its ugly head. The prima facie building blocks for a legal and policy argument are certainly present. Arguably, these firms possess a dominant share of the relevant (digital ad) market. Effective barriers to entry are high—due to the “network effect” and their (purported) infinitely rising returns to scale. And, for many users, there are no realistic alternatives: Here, the very popularity of Google and Facebook—demonstrating (like telephones once did) how “vital” they are to consumers—actually works against them. Further revenue growth, of course, also works against them.

The probability of federal antitrust action, while still low at the moment, is significant and rising. If successful, the outcome may range from service untying (to compel competition) to a ban on future acquisitions to outright divestiture and breakup. One ominous warning sign is the emergence of a robust campaign by state attorneys general, led by Missouri AG Josh Hawley, an unnervingly young Republican populist, to investigate Google for possible prosecution. (And yes it’s true: From the Sherman Antitrust Act of 1890 to the Justice Department’s lawsuit against Microsoft in 1998, state action typically paves the way for federal action.) Another is the fact that the FTC already considered suing Google on antitrust grounds back in 2012. It was a credible case. Any new action could be announced at any time with little warning, as happened with Microsoft.

Meanwhile, political tectonics are shifting in the nation’s capital, and not in a good way for Silicon Valley. While Obama had a great relationship with the tech giant CEOs, clearly Trump does not. On the campaign trail, Trump promised stricter antitrust enforcement as part of his populist agenda, and has frequently thrown monopoly charges at blue-zone Internet behemoths like Amazon. Under Trump, the FTC and Justice Antitrust Division (still struggling to acquire direction) may no longer be friendly to Big Tech.

What’s more, the ascent of the political left among Democrats is simultaneously redirecting the party of Schumer and Pelosi in the same direction. Anxious to reclaim the populist standard—and eager to harness the energy of younger activists—Democrats are putting together an aggressive break-up-the-monopolies platform. And this makes Google and Facebook a prime target of the left (yes, even as they are already a target of the alt-right). Leading the way are intellectuals like Barry Lynn, whose termination from the progressive (yet Google-funded) think tank New America last year after criticizing Google’s “new monopoly capitalism” became a cause célèbre among policy scholars on both ends of the political spectrum.

Will the Democrats take the House (or even the Senate) in 2018? Will they take the White House in 2020? Unfortunately for Google and Facebook, this reads something like a heads-they-win, tails-we-lose sort of proposition. To gird for what’s coming, Google is splurging on Washington, D.C. influencers—and in 2017 became the biggest corporate spender on lobbyists (ahead of AT&T and Boeing). Facebook goosed its spending by a third. We’ll see if they can buy their way out of this corner.

Political threats arise abroad. Direct legal action against Google and Facebook in the United States remains hypothetical. In Europe, it’s already happening. The record-breaking $2.7 billion fine announced last June by EU antitrust enforcement chief Margrethe Vestager faulted Google for not operating its search site as a neutral quasi-utility—in effect, as a level playing field for all advertisers. Gulp! There goes a big piece of Google’s business model.

With the case still on appeal, it is unclear yet how Google will respond. But it comes on top of several other rulings. In May, the EU filed antitrust charges against Google over self-dealing tie-ins to its Android operating system, and it fined Facebook over lying to regulators about its acquisition of WhatsApp. In December, Germany’s Federal Cartel Office opened a new case against Facebook, contending that the company abused its market power to extort data from users. These two companies are already laboring over other recent EU mandates, such as implementing (upon user request) a “right to be forgotten” and censoring social media conversations in compliance with anti-hate speech laws.

By all appearances, the EU is just getting warmed up. Brussels needs to counter its Eurosceptic opponents with some populist “sovereignty” crusades of its own, and what could work better than trimming the wings of American-owned cultural imperialists that have dominant market share in Paris, Berlin, and Milan? Vestager’s terse verdict—that “Google abused its market dominance”—will moreover provide a useful precedent for antitrust actions in other jurisdictions (including the United States) and warm the hearts of Google’s die-hard competitors. “This will be the most significant enforcement event in consumer tech antitrust in nearly 20 years (since DoJ v MSFT),” tweeted Yelp VP of policy Luther Lowe, in a veiled reference to the U.S. Justice Department’s final (2000) ruling against Microsoft.

Rather than a stretch of bad luck, many legal observers see these events as evidence of a fundamental shift in how the world sees U.S. tech companies. No longer are these global juggernauts immune to regulation simply because they’re on the bleeding edge of the information revolution. “Legislators, administrative bodies, and courts around the world are starting to take on giants like Google, Facebook, and Amazon,” according to Ivo Entchev, a transnational lawyer based in New York.

Outside of Europe, where the global forces of populism and authoritarianism are enjoying greater sway, Google and Facebook may be facing even more challenging headwinds. In much of South and East Asia, for example, instant autocomplete search (Google) and social media bandwagoning (Facebook) are weaponizing populist crusades by Hindus in India, Buddhists in Myanmar, Muslims in Indonesia, and the Bumiputra in Malaysia. The tech geniuses of Silicon Valley, who had always assumed that instant knowledge and communication had no downside, have been largely helpless in the face of this storm. Indeed, Facebook’s friendly team of global political advisors remains on-call to assist any charismatic leader with a popular cause.

Google and Facebook could get help by collaborating with governments—and this they do, frequently because they have no other choice. With authoritarianism on the rise, more states are demanding that Internet businesses conform to their censorship standards or provide them access to user identities. (According to The New York Times, more than 50 countries have passed laws over the past five years to gain greater control over how their people use the Web.)

The one obvious drawback is that many governments will use this power to crush dissident populists. The less-obvious drawback is that many of these governments (Myanmar, Malaysia, Philippines) are themselves in league with the populists. In November, Freedom House announced that at least 30 governments around the world are deliberately “manipulating social media to undermine democracy.”

Unavoidable bottom line? In a growing number of countries, Google and Facebook will have to make a choice that, in the past, they have artfully evaded. They either decide not to do business there, or they go along to get along—toe the government’s line on news and communication in return for pocketing the local ad revenue. Their cost of going along includes both the up-front outlays to pay for compliance (governments are now savvy enough to know that Silicon Valley can afford a hefty entrance fee) and the longer-term brand cost of complicity with regimes the rest of the world finds unsavory at best, odious at worst.

A FINAL WORD

Let’s put all of these arguments in perspective.

There is no question that both Google and Facebook are large, innovative, highly profitable firms at the forefront of an information revolution that is transforming how people learn and communicate. There is also no question that both will experience a rapid rise in revenue and earnings into the foreseeable years to come.

Since both firms are very highly valued, however, one must assess whether the rise will be rapid enough to justify their current prices. We conclude that revenue and earnings are unlikely to rise at a rate that will meet the market consensus lying behind these prices.

Our core argument starts from the premise that both companies are basically in the ad sales business; and that U.S. ad spending as a share of GDP demonstrates remarkable stability over time. We do allow that both companies’ share of total digital ad revenue will grow and that digital ads as a share of total ad revenue will grow. Still, plausible values for such growth are unlikely to get the firms’ revenue numbers close to consensus by 2021 (our chosen out-year).

We examine three claims made by bulls to justify current prices and get future revenues “back to consensus”: first, that revenue growth abroad (ex-U.S.) will accelerate; second, that we still start seeing game-changing non-ad revenue growth; and third, that these firms will benefit from the twilight of net neutrality and ultimately “own the Web.” We find these claims unpersuasive.

Finally, for balance, we offer an array of bearish scenarios of our own—each pointing to developments that could make the outcome significantly worse than we project. These include compressing profit margins; shrinking ad spending as a share of GDP; a worsening “tech-lash”; and rising political threats both at home and abroad. While it’s hard to say that any one of these is likely, we would argue that one or more of them are at least plausible.

At the very least, these scenarios make Google and Facebook a riskier play than many investors assume. It may be some time before investors are proven wrong. These companies are big enough to get by on reputation alone for the time being. Yet even before a general downturn hits, the market will certainly be on the lookout for the first signs that revenue and earnings performance may not be quite up to the consensus billing.

A word of advice to any investors choosing to bet on these ad-dependent Internet giants: Proceed with caution.