Will growing “until the cows come home” come back to bite em in the butt?

I want to be clear: Yum will continue to grow in China for years and years. What I’m focused on is the rate at which Yum is growing in China.

On the surface, it does not follow that a country where the economy is growing by 10% and consumer confidence is on the rise, that concepts like KFC would be having problems. I have been told many times by senior management at YUM that taking a traditional U.S. restaurant analyst approach to analyzing China business is just wrong. Call me stubborn, but here I go.

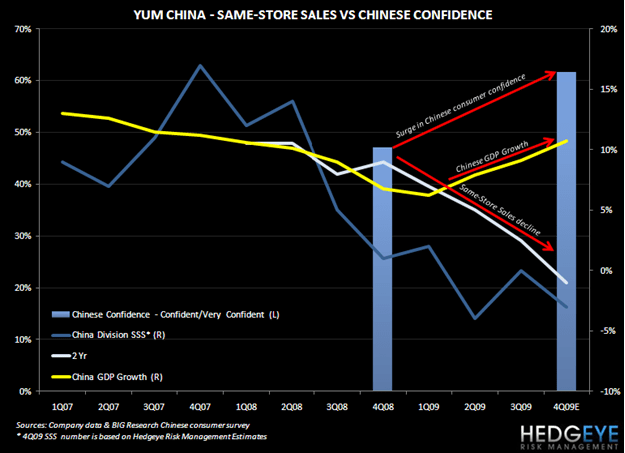

I’m trying to understand why Yum’s same-store sales in China have been coming down on a 2-year average basis throughout 2009 (and guided to come down again in 2010) when the MACRO backdrop is seemingly so positive. Why are the issues that KFC faces in China any different from any other country in the world? We see three major issues facing YUM in China: increased competition, over-building, and deteriorating brand perception among consumers due to health-related isses such as obesity.

As the chart below indicates, macro factors are providing somewhat of a tailwind. Overall consumer confidence is improving (though not reflected in sentiment towards fast food) and GDP is growing, yet YUM’s China same-store sales have gone in the opposite direction.

COMPETITION - Our contacts on the ground in China suggest that in the older, more mature cities where KFC has been for years there is significantly more local competition from smaller local players that can compete effectively on price. Not to mention that McDonald’s has made great strides in increasing its pressence in those cities as well. We have also heard that because the KFC brand is now much better known in China, when KFC opens in newer cities it has what I call the “Cheesecake” problem. The new units are so big and glamorous that they operate at peak volumes and then subsequently, struggle to grow same-store sales thirteen months later. This is not a bad problem to have until a chain begins to canabilize sales by increasing capacity in order to achieve economies of scale.

It is interesting to take our propietary comments in the context of what we heard from McDonald’s management on its most recent earnings call. “I think on an overall basis the pricing relationships in China in the quick service restaurant industry are in an interesting dilemma because of who you are competing against which is a very low price menu on the street from the non sort of chain restaurants and food available. We are not necessarily discounting but what we are doing is getting our price right in relationship to the economic time that we find ourselves in which is an ongoing pricing relationship as compared to a discounting of our food. And it moves up and down the scale depending on where we find ourselves in the consumer spending. As we’ve said, I think the environment of China which basically fell off a cliff after the 2008 Beijing Olympics. We’ve adjusted accordingly along the way to be relevant with our consumers and it’s worked well for us.”

MCD’s comments highlight that despite improving consumer confidence, YUM is not the only QSR player in China facing a slowdown in demand. The defining factor for YUM, however, is that the company is more leveraged to performance in China as management likes to point out that it continues to widen its lead in the Western QSR category with its approximately 1,700 KFC units in Mainland China relative to MCD’s 1,150 units. In 2009, MCD cut back on growth in China in response to what it called a marketplace that was not growing while YUM maintained the pace of growth it had outlined at the beginning of the year (500 new units).

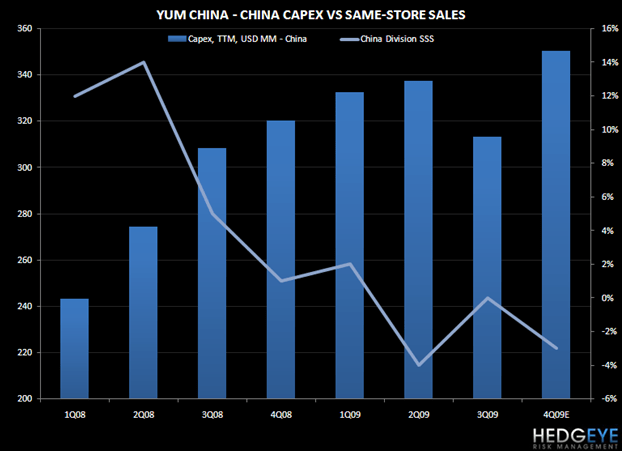

SUSTAINABILITY - Sustainability issues are looking to be a big red flag in China. The issues stem not from growth alone, but rather from the company’s rate of growth. For the past three years, YUM has raised its level of capital spending in China (forecast to grow another 9% in 2010) to roughly 10% of sales in 2009. Over the same timeframe, operating margins in China have declined to close to 16%, based on my estimates, from nearly 18% in 2006. And, return on incremental invested capital (ROIIC) has come down every year since 2006, albeit from a very impressive level. In 2009, ROIIC should come in just better than 30%, but that compares to nearly 50% in 2007 and about 45% in 2008. Based on my numbers, both margins and ROIIC will continue down on their current trajectory in 2010. Focusing too much on same-store sales and on the fact that 2-year average trends will continune to come down in 2010 may be the U.S. centric way of analyzing trends in China (as management likes to talk about system sales growth), but I can’t disregard declining margins and returns.

YUM’s mentality in China is to grow “until the cows come home” - no matter what. When a majority of management’s compensation is dependant on “system-wide sales” growth and comps are negative, the only way to get a bonus it to grow units. Over the past four years YUM has taken its total number of units in China from about 2,300 in 2005 to almost 4,000 today , with the company first talking about canabilization in 3Q05. At the time, CEO David Novak was quoted as saying that the company was cannibilizing units because four years previously, in 2001, “we thought we were starting to see some potential cannibilization in China and…we put the pedal to the metal and look at the business we’ve built”.

While YUM has taken down its total capital spending in 2009, it is forecast to grow its spending in China by about 9%. This 9% rate of growth expected in both 2009 and 2010 is toned down from the 40%-plus growth in the prior two years, but it appears that current trends should dictate further slowing in the coming years.

The likelihood of YUM slowing growth in China any time soon is low as management has publicly stated, “We could drop our sales 20%-25% and open restaurants until the cows come home - so that's what we plan on doing.” I contend that if the issues of over capacity are real and YUM maintains an accelerated pace of growth, it will exacerbate the problem.

Think SBUX!

CONSUMER PERCEPTION - In the late 90’s and early 2000’s, McDonald’s had a major problem in the U.K. dealing with consumer perception, particularly around health related issues. Based on recent performance by both YUM and MCD in China, it appears that QSR in general is facing some consumer backlash in China. Concerns about obesity preoccupy Chinese citizens and authorities alike and an awareness campaign has been launched by the government to highlight the dangers of fast food with vivid images of children playing among oversize food laced with glass and scorpions. The article, posted on france24.com, was entitled, “China scaring kids out of fast food chains”.

Obesity is a growing concern in China, and it is clear that the association between U.S.-style fast food and child-safety is being emphasized by the government.

Even if consumer confidence and GPD numbers are rising, there appears to be some MACRO related issues at play in China, too, as McDonald’s made perfectly clear on its 4Q09 earnings call.

“Now China, although their economy is improving and we delivered an increase in comp sales and guest counts in December, we expect it will still be sometime before consumers regain confidence and are willing to spend more.” NOTE: this contradicts a study that we referred to earlier in this post.

MCD’s management also went on to say - “Regarding China, a couple of things, yes we did report positive sales and guest count movement in December. You won’t see that in January though because we have the shift of the Chinese New Year so last year that was in January and this year it will be in February so by comparison that will be a little bit choppy. But, we’re optimistic in what we’re seeing with the trends. We’ve talked about China in the south, and the central and the north so we saw all three of those areas improving in December and are kind of cautiously optimistic as the consumer starts to spend a little bit of money there that we will then be able to get a little bit more out of price and get a little more traffic moving there so that’s a perspective for you.”

Another potentially important MACRO focus-point is the urban youth of China. While I have been advised by YUM’s management not to apply American logic to Chinese scenarios, I would hazard a guess that younger people are a somewhat important demographic for fast-food chains. A telling piece on France24.com entitled “Beijing graduates crammed into slums like ‘ants’” shows the harsh reality for graduates living in urban China. It is clear that these graduates are not frequenting western fast-food chains.

The photo (shown below) is followed by a comment by one such graduate living in Beijing, “This is a place to eat. It’s cheaper than in the rest of Beijing. But people only eat out for breakfast – the rest of the time we cook in our bedrooms.” Local players, whether operating out of premises or off the street, are providing formidable competition for YUM.