Position: Short natural gas via the etf UNG

In the last few days, we’ve laid out a few shorts in the commodity world. We shorted the XLE, which comprises the major U.S. based energy producers, and yesterday we shorted UNG, the natural gas etf. The thesis behind both of these positions is slightly different as oil is driven by global drivers, while natural gas is a localized, North American market.

Despite the fact that Punxutawney Phil saw his shadow this morning, which, according to the urban legend, means we will experience six more weeks of winter, winter is basically in the rear view mirror, and sequentially demand for natural gas should decline seasonally as it usually does. This year the seasonal impact will be particularly pronounced as we’ve just experienced one of the more seasonally cold winters in reason history. That, too, has become consensus. As we wrote on January 11th:

“Cold weather is good for the price of Natural Gas, we definitely get that. We also get that the idea of cold weather is becoming a solidly consensus notion. Consider the following headlines that are currently posted on the drudgereport.com:

- Cold Stuns Floridians, causes deaths elsewhere;

- Arctic air has invaded the south;

- Cold kills 100,000 tropical fish in S Florida;

- Chill Map;

- Cold snap death toll rises across Europe;

- Global cooling may set in for 20 – 30 years; and

- Feds: December was 14th coldest in 115 years.”

As of now, there is less winter in front of us than behind us, so natural gas should begin building inventory as demand naturally declines.

Currently, inventory in the U.S. is still well above normal levels. According to the most recent natural gas update from the DOE:

“Working gas in storage was 2,521 Bcf as of Friday, January 22, 2010, according to EIA estimates. This represents a net decline of 86 Bcf from the previous week. Stocks were 120 Bcf higher than last year at this time and 87 Bcf above the 5-year average of 2,434 Bcf.”

While natural gas did see a weekly decline in the most recent numbers, inventory levels are still very high and the price of natural gas is still roughly ~15% higher than it was a year ago. With higher inventory and higher price, something has to give.

The recent increase in the price of natural gas that we’ve seen as of late has been leading to an increase in drilling activity as well, which is negative for future price in a time when both inventory and production are still high. According to the Baker Hughes rig count, they see an addition of 36 rigs to the fleet in the United States and 35 rigs to the fleet in Canada week-over-week. On a year-over-year basis, the United States rig count is still down on a year-over-year basis, though Canada, which is a major producer and exporter to the United States of natural gas, is up by 99 rigs.

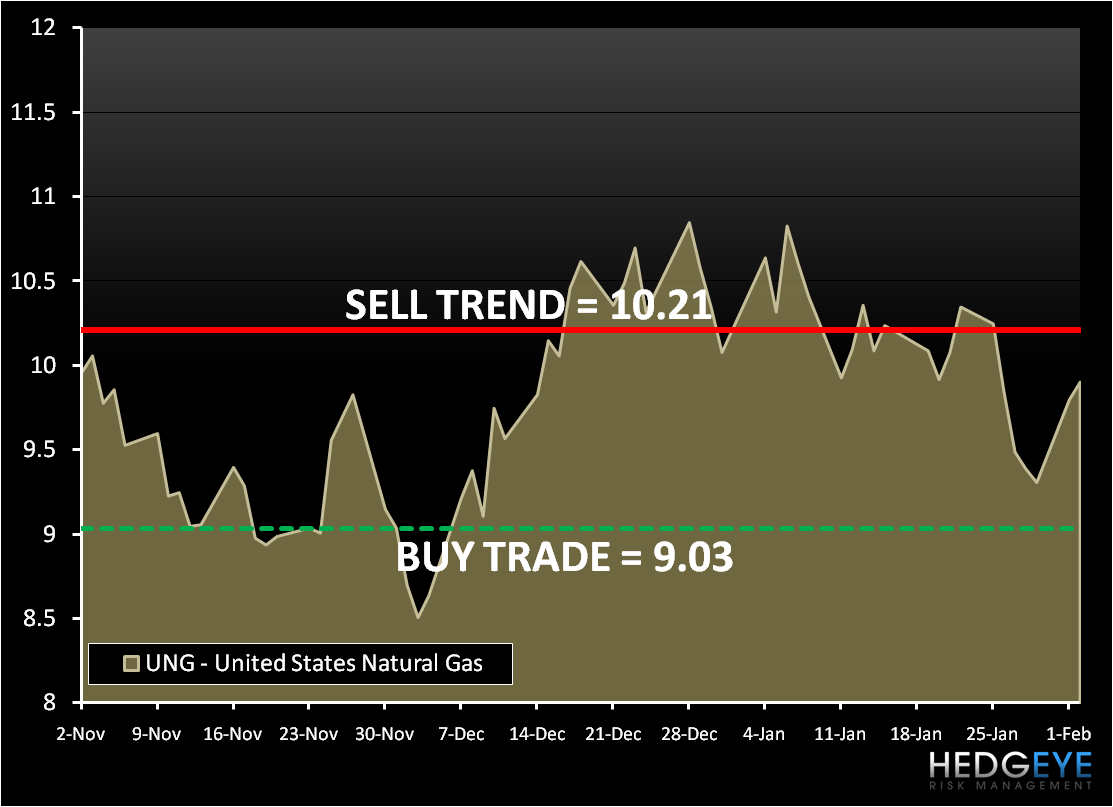

Below we’ve outlined a chart with our current levels on UNG, the natural gas etf.

Daryl G. Jones

Managing Director