Editor's Note: This is an excerpt from an institutional research note written by Hedgeye Industrials analyst Jay Van Sciver on 1/25/18. For info on how you can subscribe to Jay's research email sales@hedgeye.com.

“We must be careful not to believe things simply because we want them to be true. No one can fool you as easily as you can fool yourself!” – Richard Feynman

Confidence In Management Fading

The UAL Investor event last night was exceptional in that it completely reversed course on many key prior initiatives. We’ll review a few, but it puts analysts in the awkward position of having told investors and PMs that doing “X” (e.g. cutting high cost regional flying) is the way forward, only to find a year or two later that doing the opposite (e.g. more regional flying for connectivity) is the way forward. Basically, UAL told investors they are going to try harder on things like asset utilization and employee productivity.

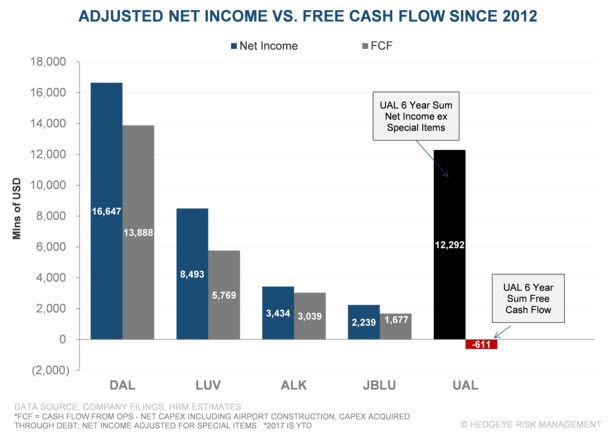

The most off target part of the presentation, in our view, is the focus on EPS and representations about the balance sheet. UAL burns cash – Free Cash Flow is negative. If one values UAL as an operating company, it should be worth the present value of future free cash flows to equity. If an airline burned cash over a 6 year period during decent economic activity, and burned cash in 2017, which was a very robust macro economy, a period over which its fleet aged and it “was shrinking”, what would that equity be worth?

UAL doesn’t provide a balance sheet in the earnings release, so we will need to wait for the 10-K to really understand the performance drivers. We update and contextualize a few key charts and quotes below. We very much see the report as consistent with our UAL thesis, and expect that investors that have been looking for a turnaround at UAL will continue to be disappointed. With fuel up, expect 2018 to be worse on the cash burn front.

Is That Balance Sheet “Terrific”?

As a cash burning company, UAL has mostly seen its balance sheet weaken in the last half decade. Had fuel not dropped precipitously, we think UAL might have spent much more time discussing balance sheet metrics. Encumbering unencumbered assets would be ‘terrific’ for the short case. A company with no debt and borrowing capacity might be considered to have a terrific balance sheet. UAL? Not so much. Where, exactly, is the cash for UAL’s share repurchases coming from?

Upshot: We continue to see UAL struggling to generate cash in 2018, with yesterday’s presentation showing a company that is flailing as it copes with an inferior cost and hub structure. With fuel prices and competitive intensity both looking like headwinds in 2018, we expect shares of UAL to trend lower.