YUM is scheduled to report 4Q09 earnings after the close on Wednesday with the earnings call to follow on Thursday morning. Given that the company updated its 4Q09 outlook and provided detailed FY10 guidance on December 4th prior to its annual investor meeting in New York, I am not expecting too many surprises. My EPS estimate of $0.50 is slightly better than the street’s $0.48 per share estimate, but again, an earnings beat from YUM would not come as a surprise. If YUM’s earnings do come in better than expectations, that will be the extent of any good news in the quarter. Management guided to 4Q09 same-store sales growth of -3% in China, -1% in YRI and -8% in the U.S., which implies a further sequential slowdown in 2-year average trends in the U.S. and China, YUM’s two biggest segments from an operating profit perspective. A -1% at YRI in 4Q09 yields a +2.0% 2-year average trend, which is flat sequentially from 3Q09, but down from the 5%-plus level that the company posted in 1Q09 and throughout all of 2008.

YUM’s stock has underperformed its QSR peers over the last year and more recently, in the last 6 months, slumped -3.1% versus the group’s average 10.3% move higher. This sequential slowing of top-line trends across each of the company’s segments is largely to blame, and management’s full-year 2010 comparable store sales guidance assumes more of the same. YUM’s same-store sales guidance of +2% in the U.S. implies flat 2-year average trends in 2010, but this is flat with what have been consistently weak results. YUM’s 2% comparable store sales target for China in 2010 assumes a 250 bp decline in 2-year average trends, after declining more than 600 bps in 2009. And, the 3% target for YRI also points to continued declines in 2-year average trends.

Management maintained its 10% EPS growth goal for 2010. The company will benefit from continued commodity deflation in the first half of the year, particularly during the first quarter and should be helped by foreign currency favorability, also in the first half of the year (the company guided to a full-year foreign currency translation benefit of $25-50 million). The solid cash flow story remains intact with YUM set to generate about $900 million in free cash in FY09 and I am modeling a number north of that in FY10. That being said, I think investors need to a see shift in trends in China, most importantly, and in the U.S. before becoming more comfortable with owning this name.

U.S.:

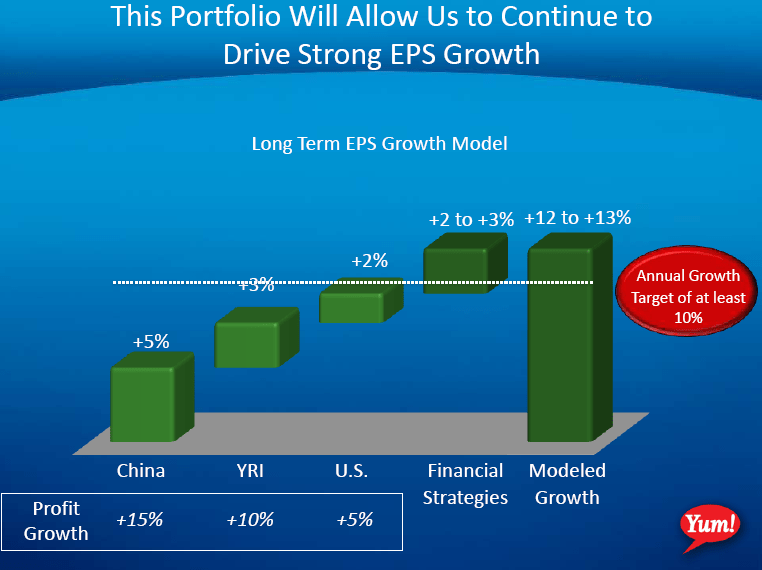

Despite all of the slides that YUM management has put up over the years showing the size of the U.S. relative to the growing size of China and YRI in terms of operating profit, currently, the U.S. remains the biggest segment at 38% of operating profit. Although the U.S. is still the biggest standalone segment, the company’s ongoing EPS growth model relies more on growth driven by Financial Strategies than from the U.S. business (as seen in the company’s slide attached below). This is not new as the company has successfully achieved its annual 10% EPS growth goal while consistently missing its ongoing U.S. operating profit growth target of 5%. If the company is unable to hit this 5% goal in 2009 (my model has the company just falling short), it will only become increasingly harder to do. Yes, YUM is currently operating in a difficult environment from a top-line perspective but the company has been benefiting from significant commodity favorability, particularly in the second half of the year, on top of the recently implemented G&A savings (yielded over $50 million of the targeted $60 million in savings through 3Q09). It is important to remember that YUM’s initial 2009 guidance included 15% operating profit growth in the U.S. This was then revised down to high single digit growth, which again, I think could prove aggressive.

During the fourth quarter, YUM will reverse its prior four quarters of operating profit growth in the U.S. Same-store sales growth deteriorated further as indicated by management’s -8% guidance (could come in worse as we have heard from YUM’s peers that weather in December was a factor), commodity deflation will still benefit the company during the quarter but to a lesser degree than in 3Q09 (only about $9 million vs. $16 million in 3Q09, according to guidance provided in the 3Q09 earnings release) and G&A savings could be partially offset by “certain G&A expenses that are a bit back loaded this year.”

Going forward, management has said that YUM’s profits will increasingly be driven by Mainland China, YRI and Taco Bell (estimated to make up 90% of profits by 2012 versus close to 85% now). In the meantime, the company continues to maintain its 5% operating profit goal in the U.S. In 2010, YUM will be lapping positive operating profit growth in the U.S., which in and of itself, puts the company’s 5% operating growth at risk once again. YUM will also be lapping the $60 million in cost savings. Not to mention, we do not know when trends will stop getting worse.

So that leaves China and YRI to buoy future growth, but based on recent trends and the uncertainty around when demand will return to prior levels, some investors may not be convinced.

China:

As I said earlier, same-store sales trends in China continue to get worse. And, easy comparisons no longer seem meaningful as the company’s 4Q09 guidance of -3% is lapping only 1% growth from the prior year (which is an easy comparison relative to the 12%-14% compares from 1H08). In 3Q09, YUM was able to deliver 32% operating profit growth despite the slowdown in top-line trends as commodity deflation helped to the tune of $21 million. Although the company is expecting a similar level of commodity favorability during the fourth quarter, the continued fall off in same-store sales will lead to increased sales deleveraging. I am modeling single digit operating profit growth in the quarter, which is a far cry from the 20%-plus growth to which investors have become accustomed. Commodity deflation should continue to benefit margins in the first quarter, but remember the company’s same-store sales guidance implies a continued fall off in 2-year average trends for the full year. Management will do its best to offset any bottom line weakness with continued development growth (6% of the company’s EPS growth target is driven by new unit growth), but it is important to note that the company lowered its targets for China within it ongoing earnings growth model to 15% operating profit growth (from +20%).

YRI:

Same-store sales trends fell off during the second quarter on a 2-year average basis, but have remained fairly steady since then. Full-year guidance, however, implies a slight slowdown in 2010. Both commodity costs and foreign currency translation worked against YRI for most of 2009, but that should reverse on both fronts in the fourth quarter. Through the third quarter, YUM’s earnings included a negative $53 million impact from currency. In its December 4th 2009 guidance, the company stated that its full-year guidance assumed a negative foreign currency translation impact of about $45 million, which implies an $8 million benefit in 4Q09, largely at YRI. Those two factors should help to offset the expected 1% same-store sales decline during the quarter and lead to operating profit growth in the quarter, reversing the prior four quarters of decline. Commodity cost and F/X favorability should continue to benefit this segment in early 2010 but slowing top-line trends could weigh on results.

Howard Penney

Managing Director