In the business world, the rearview mirror is always clearer than the windshield.

-Warren Buffett

As I said on Thursday, the initial estimate of GDP is the most heavily rigged and politicized data point put out by the government. Friday’s headline GDP number of 5.7% was a very strong number, but the advanced number is more about politics than reality about the strength of the US economy. More importantly it’s looking in the rear-view.

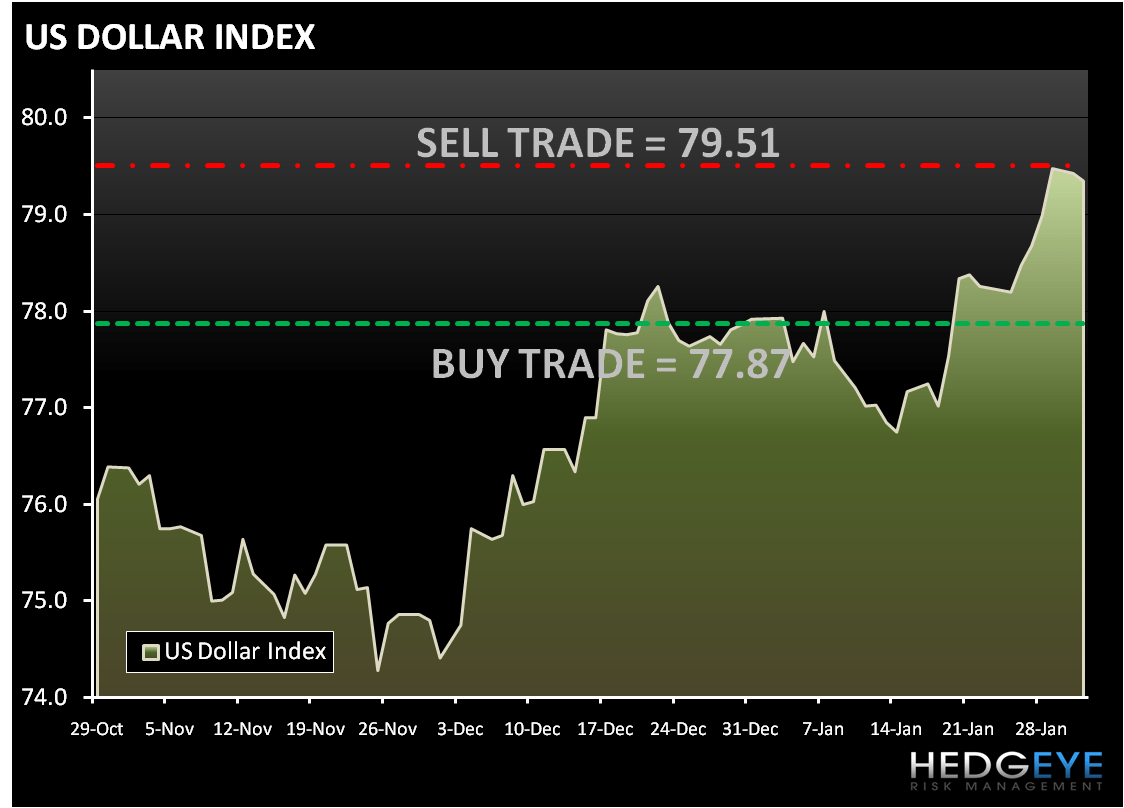

The markets were lower on Friday after rising initially from the strong GDP number. The REFLATION trade continues to unwind with the strength in the US economy, which is dollar bullish. The Dollar index was up 0.71% on Friday and is now up 2.06% year-to-date. The Hedgeye Risk Management models have the following levels for DXY – buy Trade (77.87) and Sell Trade (79.51). With our “Break-out Buck” theme we are dollar bullish in 1Q10.

Also on the MACRO front there were other bullish economic data points out on Friday. The January Chicago Purchasing Managers Index was 61.5 vs. consensus at 57.2 and the final January University Michigan Confidence reading was 74.4 vs. consensus at 73.0.

The Greece debacle continues to live on. The reports of EU willingness to consider providing relief to Greece met “Europeans Pointing Fingers” (see or 1/29 post) with sharp denials. The issue has demonstrated that European countries are quick to dismiss their own problems in favor of calling out their neighbors.

The VIX was up 3.75% on Friday and is up 13.56% year-to-date. The Hedgeye Risk Management models have the following levels for VIX – buy Trade (22.37) and Sell Trade (28.94).

Regardless of how fast they are growing or innovating, Technology (XLK) was the second worst performing sector on Friday and year-to-date. The semiconductor index is under considerable pressure declining 3.42% on Friday. Year-to-date the SOX is down 12.18%. Friday’s standout to the downside was SNDK, declining 11.67%, on a decent quarter, but underwhelming guidance. Mr. Softie (MSFT) also reported a good quarter but declined 3.36% on Friday.

On the back of the stronger confidence numbers, two of the three best performing sectors on Friday were consumer - XLY and XLP. While the GDP number was strong, the personal consumption expenditures declined sequentially down to 2.0% annualized from 2.8% in 3Q09 and the personal savings rate increased slightly to 4.6% from 4.5%.

As we look at today’s set up the range for the S&P 500 is 32 points or 1.5% (1,056) downside and 2.3% (1,098) upside. At the time of writing the major market futures are trading up on the day.

In early trading today Copper is trading lower to an 11-weeks low; a stronger dollar and concern about China’s demand. The Hedgeye Risk Management Quant models have the following levels for COPPER – buy Trade (3.03) and Sell Trade (3.12).

In early trading today Gold is little changes but could trade higher today on a weaker dollar. The Hedgeye Risk Management models have the following levels for GOLD – buy Trade (1,066) and Sell Trade (1,111).

Crude oil is little changed over concerns over the pace of demand growth. The Hedgeye Risk Management models have the following levels for OIL – buy Trade (71.38) and Sell Trade (77.08).

Howard Penney

Managing Director