With the meeting of the World Economic Forum this week in Davos, we’re getting a host of interviews from the Who’s Who, including European policy makers that are asked to comment on Greece’s budget deficit issues. What’s clear from the interviews is that while by in large most of the European community has tried to calm fears of sovereign default in Greece’s debt—suggesting a close cooperation with Greek officials to cut spending and hone in on its budget deficit over the next three years - we’ve also seen officials (including those with important name tags on) put their foot in their mouth. In particular, Monetary Affairs Commissioner Joaquin Almunia recently said” “Greece will not default. In the Euroarea, default doesn’t exist.”

As we’ve noted in our recent posts on Greece (see our portal), there’s plenty of evidence that sovereign default exists, and could be a reality for Greece. Further, we’d point you to “This Time is Different”, a book by Carmen Reinhard and Kenneth Rogoff that discusses sovereign default across nations over the last eight centuries. In short, Almunia’s statement seems fully absurd.

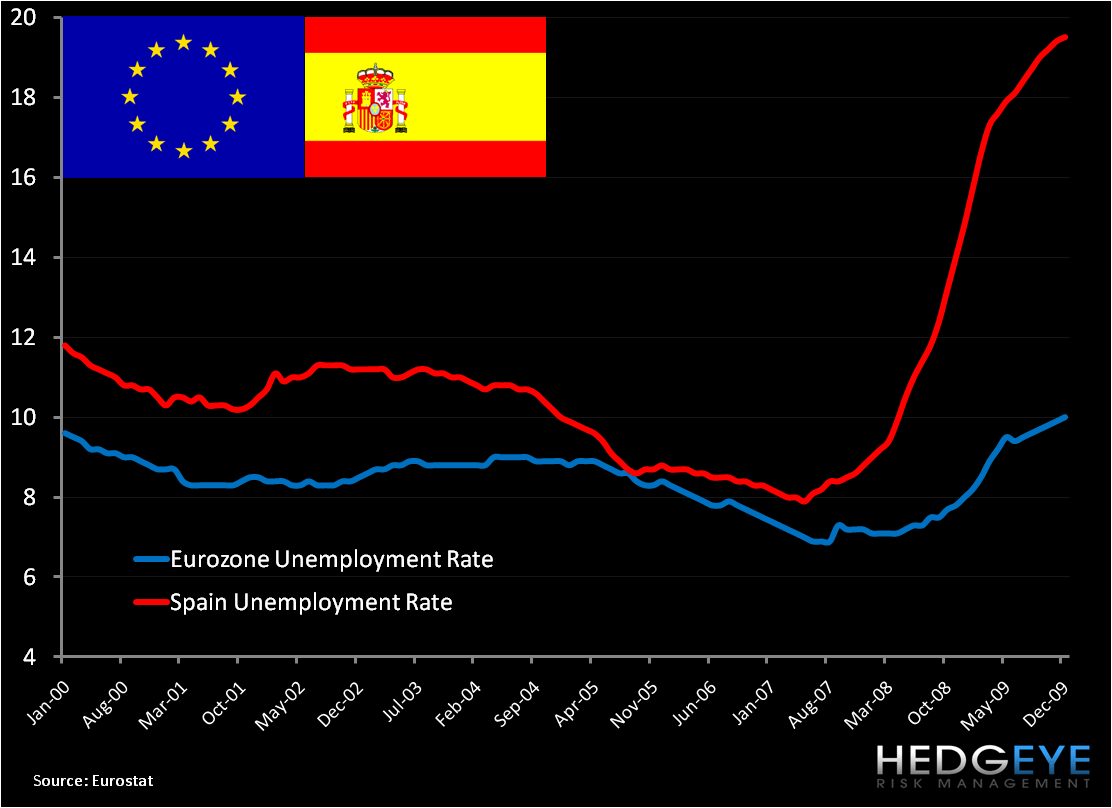

The interviews have also demonstrated that European countries are quick to dismiss their own problems in favor of calling out their neighbors. The chart of Spanish unemployment is just one of the charts referenced to deflect attention. Today, Spain released its 4Q09 unemployment at 18.8% from 17.9% in the previous quarter, well above the Eurozone’s most recent reading of 10%.

Matthew Hedrick

Analyst