ADT filed an initial S-1 in December 2017 indicating the company plans to IPO. Our first pass review is more bear than bull, and consequently ADT goes onto our Short bench pending more data.

Since going private Apollo has gotten rid of ADT management and combined the company with two other assets in the security system market, Protection1 and ASG. Here we review the positives and negatives that stand out to us from the new ADT.

The Positives

Management is increasing prices on a declining customer base and at the same time improving churn metrics. That is pretty impressive. It shows ADT’s new CEO has a good toolkit. It also implies that the company had been poorly run in the past. Achievable operating fixes was likely a central tenet of the buyout.

Churn has declined from 16.5% pre-merger to 13.9% (15.2% to 13.8% y/y comparison) under new management. The combination of price action and declining churn is leading to higher operating cash flow margins.

There are a lot of moving parts in the OCF numbers including merger costs, but just taking net income plus D&A, we see a ~150bp improvement in margins y/y for the 9mos ended 9/30/17.

We also see ADT Canopy as a medium term positive. The monitoring service-only option, launched two years ago, potentially reduces the friction in the customer on-boarding process using the channel of any-brand home gateways, and also reduces ADT exposure to the costs of hardware electronics and service installation.

The Negatives

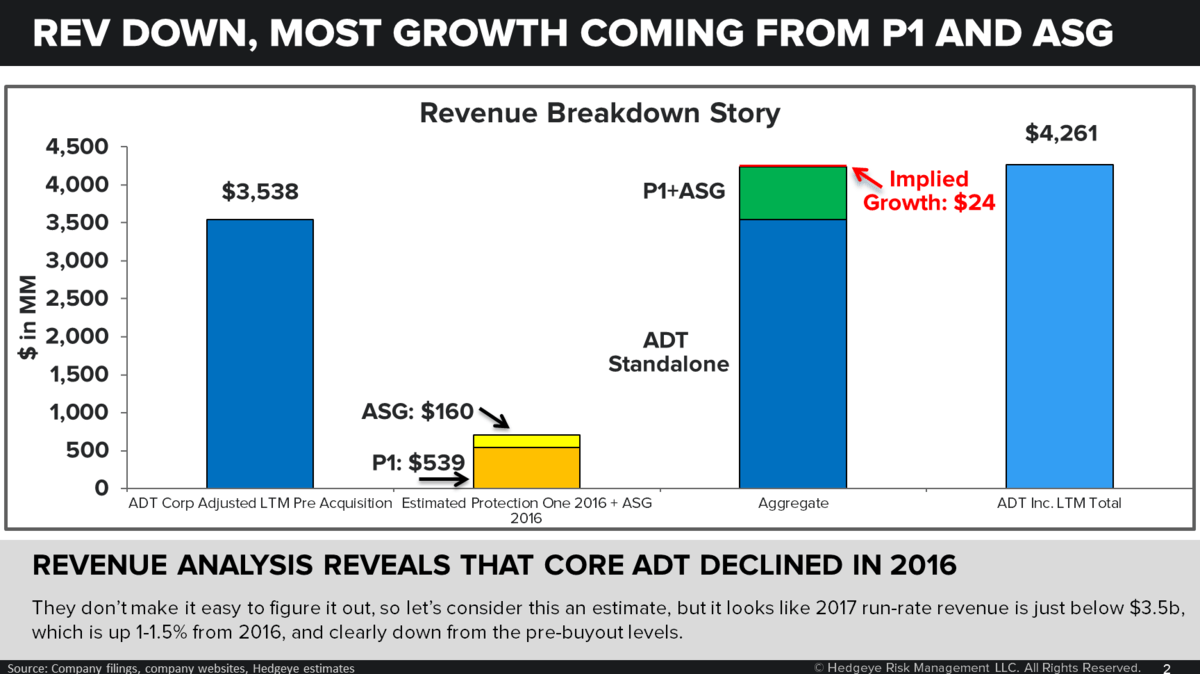

The security system penetration curve is essentially non-existent. The S-1 discloses a 2017 penetration of US homes of ~20% whereas the comparable study from 2010 placed the rate at ~19%. And, even with all the great management moves to raise prices and reduce churn, consolidated y/y % growth looks like a meager 3.1%.

Worse, our math on 2016 revenue indicates standalone ADT revenue declined (even when factoring changes in revenue from M&A). We calculate core ADT revenue was down in 2016, and barely up in 2017 thanks to price increases on a declining customer base.

Canopy, IoT, and the push of the consumer electronics market into home gateways could help trigger an uplift in home security service penetration rates. But that trend also opens a Pandora’s box of competition that will change the home security systems market. The shift to monitoring-only service is a short term positive, but also basically admits the fact that the consumer electronics industry is coming full force into this sector via the home gateway market. Home gateways will help manage electronics in our homes, and security is an important application in that category. So the competitive factors here are set to change.

For one thing, it potentially implies that ADT’s hardware installed base, which carries a book value equal to ~17% of total assets, will have a low or zero terminal value. ADT’s traditional selling motion was to charge a large installation fee for the hardware that could be amortized over the life of the contract, thus tying customers into a long term pay structure. Without the hardware installation element, the durability of customer contracts may be challenged.

Second, while it sounds fun to have so many new hardware partners who are all eager to drive rich service subscriber dollars to ADT, it is unlikely that these large companies will remain satisfied selling low margin consumer electronics devices into our homes.

Third, some of the new competitors will also wield modern day software tools into the service category which is ripe for automation and the use of greater analytics. Most of the alarms that ADT receives are false positives which could be greatly reduced using image recognition software and analysis. If the false positives are removed and all the system does is to notify 9-1-1 for a true break-in, how hard is that for a software giant to program? The opportunity is ripe for software to eat into ADT’s core service revenue. While this is a nascent threat, long term value investors have to be wary about their assumption of terminal value of the ADT subscriber base.

Valuation & Taxes. The S-1 states the company will not be a material cash tax payer until 2023 due to a $3.5b NOL. But the recent tax law changes imply that NOLs can only buffer 80% of EBITDA, and interest expense related tax deductions are also limited, creating a likely cash tax headwind for ADT.

The company capitalizes and breaks out the FCF impacts from client acquisition, maybe in the hopes that investors see those costs as transient. With d-d% churn rates likely remaining for the foreseeable future, ADT will always need to pursue new client growth and will always incur client acquisition costs.

That said, $141m in LTM FCF is kinda tough to get excited about. 2017 improvements to $228m for 9mos ending 9/30/17 are promising, but still far from panacea. If we generously assume ~$300m+ for 2017 FCF on its’ way to $400m run-rate exiting 2018 thanks to ongoing churn improvement, we can see how people might get creative. But with ~$11b in debt outstanding, creativity will require a high multiple, and we just can’t see our way to that in light of no market penetration element, low growth, still d-d% churn, new technology related risks rising, and slim/improving real cash generation.

Last point - why would they go public now?

Bull. Apollo believes in the new CEO and wants to showcase his ability to capture greater value and cash flow from the user base of the former ADT.

Bear. Fact #1: ADT was already levered at the time of the take-private. Fact #2: ADT doesn't generate that much in real cash. Fact #3: Apollo just paid themselves a dividend from ADT that equates to greater than 5x trailing FCF. Conclusion: Apollo had to get creative with financing.

Enter the Koch brothers, not rich for nothing. The Koch Investors provided $750m in equity financing (preferred securities) that grows over time (now already ~$772m) and carries an ~11% annual cash dividend. Cash. At $84m for 2017 alone, the dividend will eat up 25-30% of ADT real FCF. Redeeming the Koch Securities and getting rid of those cash payments is likely a priority that can be achieved in the IPO.

You pick which side of that argument you like. Still time + data ahead to make any formal conclusions.