In the last 24 hours the latest reading on confidence and sentiment are headed in two different directions - confidence up, sentiment down.

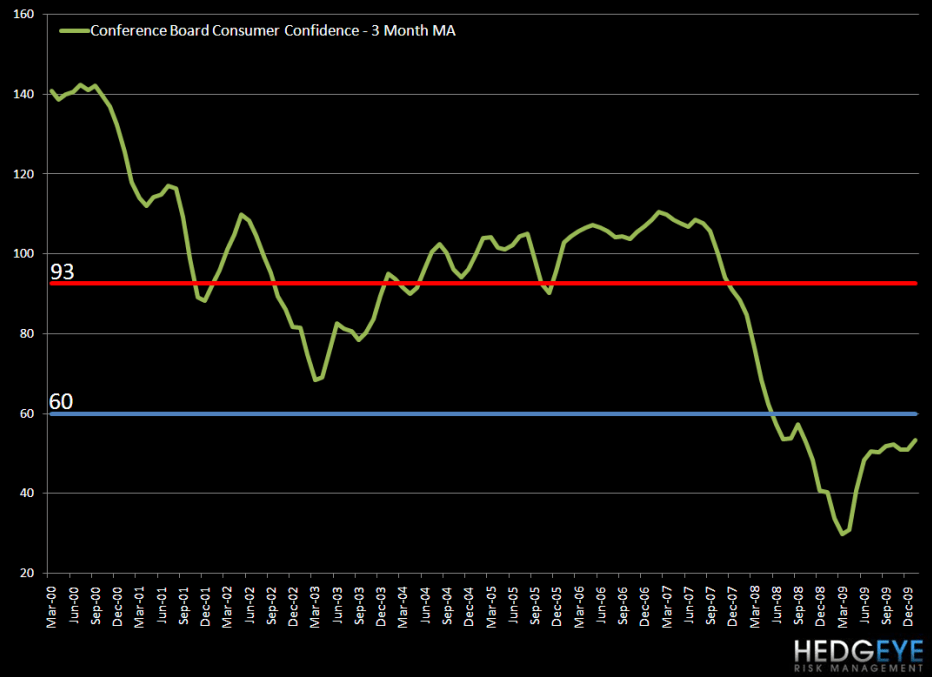

Yesterday, the Conference Board’s January confidence index increased to 55.9 (higher than the Bloomberg survey) from a revised 53.6 in December. The January figure is up 111% from the record low of 25.3 in February 2009, but 65% below the 92.3 average over the past 10 years. This is the highest reading since September 2009, when the index stood at 61.4.

Like we have seen with the “bottoming” in housing statistics (both starts and prices), confidence is bottoming too. While the popular press will make a big deal about yesterday’s move, any print below 60 on the Conference Board Index is just not that meaningful.

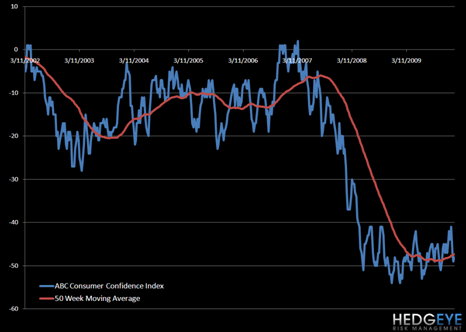

The bottoming feeling in confidence was also seen in the ABC number reported last night. The index improved to -48 from -49 last week. Personal finances improved to -6 from -10, while the state of the economy deteriorated to -84 from -82 last week.

The difference between the bulls and bears contracted dramatically to +15.7%; it was +33.3% last week and +37.5% two weeks ago. According to Investors Intelligence, readings above +30% are very bearish. The levels over the last two weeks were the highest since the spread was +42% at the October 2007 market peak.

The markets are fighting to maintain upward momentum as the S&P 500, the CRB and China are all broken on TREND and TRADE. What is not working currently is the buy-the-dip mentality that has been in place since the March 2009 low. The latest surge in pessimism, however, is a net positive for equities.

Howard Penney

Managing Director