Keeping an Eye on Yue Yuen

As the epicenter for many brands in the global supply chain for athletic and casual footwear, there are some meaningful category, geographic, and input cost callouts from Yue Yuen’s Q.

Total sales growth for Yue Yuen improved sequentially on the 1 year and 2 year. Order flow marked a bottom in Q4 09 (September) at -6.1% (inventories down 8%) and rebounded in December’s Q1 10 at -3.4%. Compares for the rest of the year are easy due to the sharp drop in sales in Q2 09. Yue Yuen expects order flow from its brand name customers to be stable going forward and believes global consumer demand for athletic and casual shoes as well as athletic apparel will be reinvigorated by the World Cup.

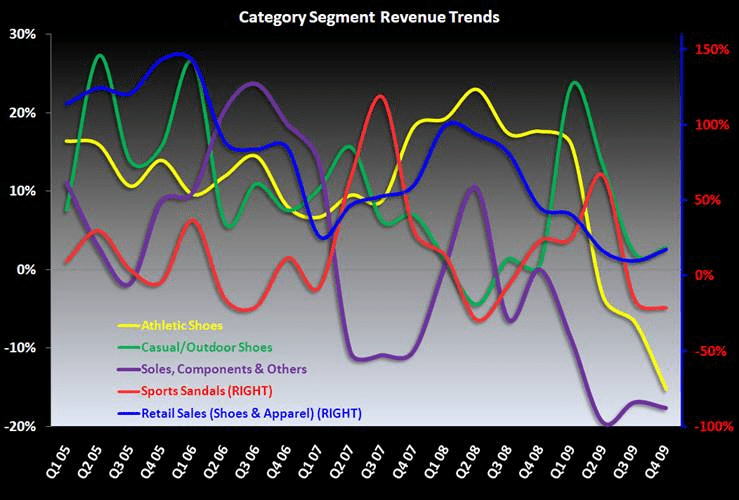

Athletic shoes, which represent about 68% of wholesale sales, were at their weakest levels in Q4 09 at -15%. Only shoe components came in weaker. These numbers have proven to be a lagging indicator to US footwear sales, so we’re not surprised by the weakness. In fact, we’d be alarmed if the numbers started to tick up meaningfully, as it would suggest that sales to the wholesale channel are picking up without us having seen the order flow on the front end. That would concern us as it relates to speculative inventory. Casual and outdoor shoes sequentially improved in Q4 and performed as the only positive wholesale category in Yue Yuen’s portfolio. Strong growth in Chinese retail at 17.4% from 9.8% in Q3 09 helped drive company topline to a sequential improvement.

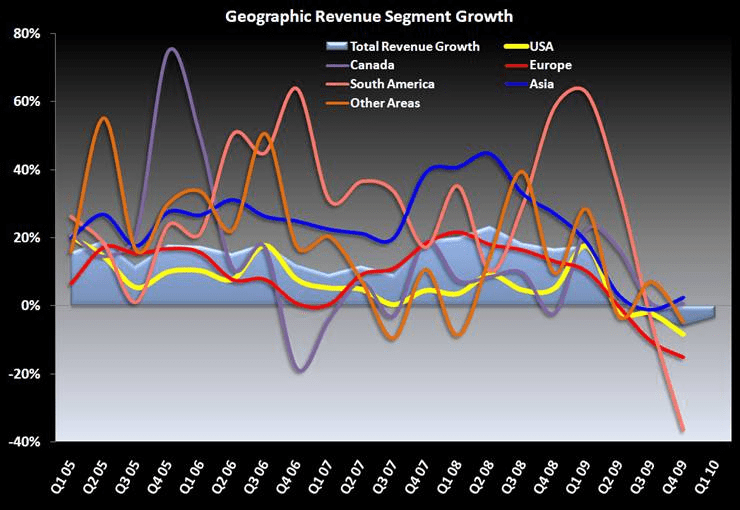

Yue Yuen is banking on steady Chinese growth in athletic apparel and footwear from the increasing interests of the Chinese consumer in athletic lifestyle apparel and footwear. South America, Europe, and the US remain weak while China and Asia continue to grow. Revenue distribution amongst categories and geographies has been undergoing a dramatic shift as the Chinese athletic footwear and apparel market quickly surpasses the ailing US consumers. US revenue has fallen from over 50% of Yue Yuen’s sales in 2002 to 31% in while Asian sales (over 90% is greater China) have grown from 14% to 39% over the same time period. The growth in China’s slice of pie has been driven by Yue Yuen’s focus on retail where the company has over 10,000 points of distribution from its joint ventures and directly operated retailers. Yue Yuen captured the emergence of the Chinese consumer as their retail business was less than 1% of sales in 2002, and is now greater than 20%. Yue Yuen is positioned well for growth as the global emphasis shifts away from the US.

The company cautioned that wages, commodities, currencies, and global responsibilities continue to pressure profits. Minimum wage increases for factory workers is occurring across all of Asia and commodity prices are threatening margins. The potential appreciation of the Renminbi, which has been demanded by developing countries, would hurt the manufacturing side of Yue Yuen’s business as FX will become a serious headwind. They’ve been noting this for a while now, and the tone has not changed meaningfully – so there’s not much here that is new to us as it relates to our broader thesis.

-Zach Brown