“We need to go faster on structural reforms in France.”

-Emmanuel Macron

Now there’s one thing I agree with when it comes to the political path forward in France. As we’ve reminded investors in 2017, irrespective of Macron’s election victory, France is not the United States of America.

Q: What happens when you get US #TaxReform + US Growth & Profits (and capex, and new orders, and confidence, etc.) #Accelerating?

A: All-time SP500 highs.

Back to the Global Macro Grind …

Welcome to Macro Monday! For those of you who are new to subscribing to our Global Macro Risk Management #process, on Mondays we contextualize last week’s macro market moves within intermediate-term @Hedgeye TRENDS and long-term TAILs.

So rather than talking up the buying of the damn US Equity & Credit dip we saw on Friday, first let’s review major FX moves from last week:

- US Dollar Index was +0.1% last week and is currently NEUTRAL from an intermediate-term TREND perspective

- EUR/USD was down -0.3% last week and is currently NEUTRAL from an intermediate-term TREND perspective

- GBP/USD led major FX gainers closing +1.0% last week and is back to BULLISH TREND @Hedgeye

- JPY/USD was down -0.6% last week and remains BEARISH TREND @Hedgeye

- CAD/USD was +0.2% last week and remains BEARISH TREND @Hedgeye

Note that when something is “neutral” it’s trading right around my critical TREND signal level and needs more time and space to pick a trending direction. If the USD Index were to recover 93.30 it would go back to BULLISH TREND; EUR/USD has a long-term TAIL risk level of $1.19.

Looking at some of the key Reflation/Deflation callouts within the lens of the Commodity market last week:

- The CRB Index (19 Commodities) was down -0.8% last week but remains BULLISH TREND @Hedgeye

- Oil (WTI) corrected -1.1% last week but also remains BULLISH TREND @Hedgeye

- Copper corrected -3.0% last week but remains BULLISH TREND @Hedgeye

- Nickel got smoked, dropping -7.8% last week and moves to BEARISH TREND @Hedgeye

- Lumber prices reflated another +3.8% last week and they remain BULLISH TREND @Hedgeye

Once Mr. Market confirms BULLISH or BEARISH TREND signals, we ask ourselves why? Why is it that lumber is diverging from nickel? Is it post-hurricane rebuild demand in the USA vs. #ChinaSlowing on the “Old China” front (nickel)? I think so. But that’s just me.

Since there’s a healthy debate on “what is a currency” these days (Neil Howe will host our 1st ever #Bitcoin research call tomorrow – ping if you’d like access), those of us who think Gold is a currency realize it’s losing value as real US rates rise:

A) Gold under-performed again closing down -0.7% last week and remains BEARISH TREND @Hedgeye

B) Silver sucked both relative and absolute performance wind dropping another -3.6% last week = BEARISH TREND @Hedgeye

And while we realize we have clients who only invest in one part of one asset class of the world, our job as Global Macro Risk Managers is to help you pick RELATIVE winners in addition to helping you avoid relative losers. Europe (stocks and bonds) has plenty of those divergences.

Looking at US stocks vs. European ones:

- SP500 was up another +1.5% last week to +18.0% YTD = BULLISH TREND @Hedgeye

- Nasdaq finally corrected a whopping -0.6% last week to +27.2% YTD = BULLISH TREND @Hedgeye

- Russell 2000 ramped another +1.2% last week to +13.3% YTD = BULLISH TREND @Hedgeye

- EuroStoxx600 dropped another -0.7% last week to +6.2% YTD = BEARISH TREND @Hedgeye

- FTSE (London) was down another -1.5% last week to only +2.2% YTD = BEARISH TREND @Hedgeye

- France’s CAC 40 lost -1.4% last week to +9.3% YTD = BEARISH TREND @Hedgeye

While I realize this is annoying some European Bulls, these are indeed the rate of return facts. If you want to be super bullish on Europe on both an absolute and relative basis to the USA, it should be in long-term Government Bond terms!

A) UST 10YR Yield was UP +2 basis points to +2.36% last week = BULLISH TREND (in yield, bearish on the bonds) @Hedgeye

B) Italy’s 10YR Yield was DOWN -10 basis points to 1.72% last week = BEARISH TREND (in yield, bullish on the bonds) @Hedgeye

C) France’s 10YR Yield was DOWN -9 basis points to 0.61% last week = BEARISH TREND

So how would a “European growth and inflation is better than the US” bull reconcile all that I just wrote? I have no idea but I’m happy to hear the narratives even though I’m tone deaf to them relative to the rates of change in both the economic and market data.

Another place US growth and reflation bulls have been getting paid (relative and absolute) since Reflation’s Ramp (in SEP when Oil broke out) is being long US bank stocks vs. Chinese stocks:

A) Financials (XLF) had a huge week, closing +5.1% last week to a US market return of +18.6% YTD = BULLISH TREND @Hedgeye

B) Shanghai Composite Index corrected another -1.1% last week to only +6.9% YTD = NEUTRAL TREND @Hedgeye

Have macro tourist friends who aren’t long the Financials because they’re “concerned about a flattening yield curve?” Sorry to hear that. They definitely didn’t get that call on positioning from us (and they just missed the biggest relative performance week of the year).

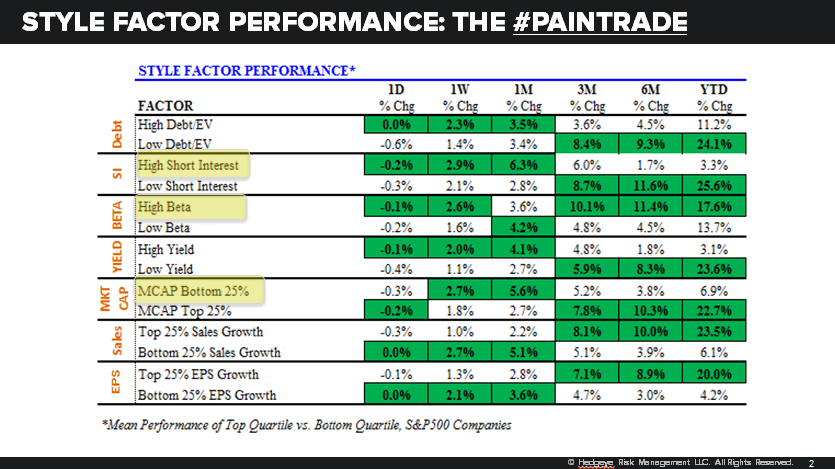

Another reality that continues to manifest in US Equity Style Factor terms is what’s called the Pain Trade:

- HIGH SHORT INTEREST stocks led gainers, closing up +2.9% last week

- HIGH BETA stocks were right behind consensus shorts at +2.6% last week

- SMALLER CAP stocks played catchup too, closing +2.7% last week

*Mean performance of Top Quartile vs. Bottom Quartile, SP500 companies

This Macro Monday will indeed prove painful for anyone who shorted Friday’s Trump v. Flynn lows. While Reforming Bears who invest with their emotions and political opinions has been a grind in 2017, I think our consistently data-driven coaching approach is gaining some traction.

Our immediate-term Global Macro Risk Ranges (intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.31-2.42% (bullish)

SPX 2 (bullish)

RUT 1 (bullish)

NASDAQ 6 (bullish)

USD 92.40-94.25 (neutral)

EUR/USD 1.16-1.19 (neutral)

YEN 110.61-113.66 (neutral)

GBP/USD 1.32-1.35 (bullish)

Oil (WTI) 56.08-59.30 (bullish)

Gold 1 (bearish)

Copper 3.02-3.12 (bullish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer