The deterioration in the S&P 500 that started on Wednesday accelerated to the down side on Thursday. The S&P posted its first back-to-back decline since December 8, 2009. Volume was above average, and up 42% day-over-day.

The VIX was up 19.2% and posted its biggest one-day spike since November 27, 2009 and finished at its highest level since December 17th. The Hedgeye Risk Management models have the following levels for VIX – buy Trade (19.76) and Sell Trade (22.51).

From a MACRO perspective, there were a number of factors weighing on stocks yesterday. First, China tightening concerns increased after another batch of strong economic data that helped to solidify fears about a bubble. With our “CHINESE OX IN A BOX” theme we continue to be bearish on China for the immoderate term. Last night the Shanghai index declined 0.95% and is now down 4.5% year-to-date. This is putting pressure on the RECOVERY trade, as the Materials (XLB) was down 4.3% on the day. The XLB is now down 2.2% year-to-date, which makes it the worst performing sector this year.

Second, the job picture got a little worse last week. Initial claims jumped 36,000 to 482,000 for the week ended January 16th -- the highest level in two months. Consensus expectations were for a small decline to 440,000. How convenient that the Labor Department noted that the increase was due to "administrative issues" related to a backlog of claims from the holiday season.

Third, the regional Philadelphia Fed Index fell to 15.2 in January from 20.4 in December, below the consensus of 18.0 and snapping a five-month streak of increases. While new orders fell to 3.2 from 8.3 and shipments slipped to 11 from 14.9, the bulk of the other components of the report, including six-month expectations, showed some signs of improvement in January.

The Hedgeye Risk Management models had six sectors breaks the TRADE line yesterday and the Financials (XLF) broke both TRADE and TREND. The only sector that is positive on both durations is Healthcare (XLV).

The Financials were the second worst performing sector as the there was a sharp selloff in the group following President Obama's latest financial reform proposal. Hit the hardest were the large-cap banks and investment banks with JPM -6.6%, BAC -6.2%, C -5.5%, MS -4.2% and GS -4.1%. The banking group outperformed for a second straight session yesterday, with the regional banks among the standouts in the group. Signs that credit quality is improving ahead of expectations seem to provide support to the group.

The best performing sector yesterday was Technology (XLK). A batch of largely upbeat earnings guidance out of the Technology sector was the primary factor. The software sector remained under pressure however, with the S&P Software Index down for a second straight session. The semis were mostly weaker with the SOX down 0.5%.

Earning out of the consumer space helped the Consumer Discretionary outperform by 30bps. Yesterday, EL +9.2%, PNRA +7.3% and SBUX +1.7% all reported better that expected results.

As we look at today’s set up the range for the S&P 500 is at 16 points or 0.53% (1,110) downside and 0.90% (1,126) upside. At the time of writing the major market futures are trading up on the day.

Copper prices fell to the lowest level in almost four weeks as a drop in equity markets has cooled demand expectations and the dollar’s strength. The Hedgeye Risk Management Quant models have the following levels for COPPER – buy Trade (3.30) and Sell Trade (3.38).

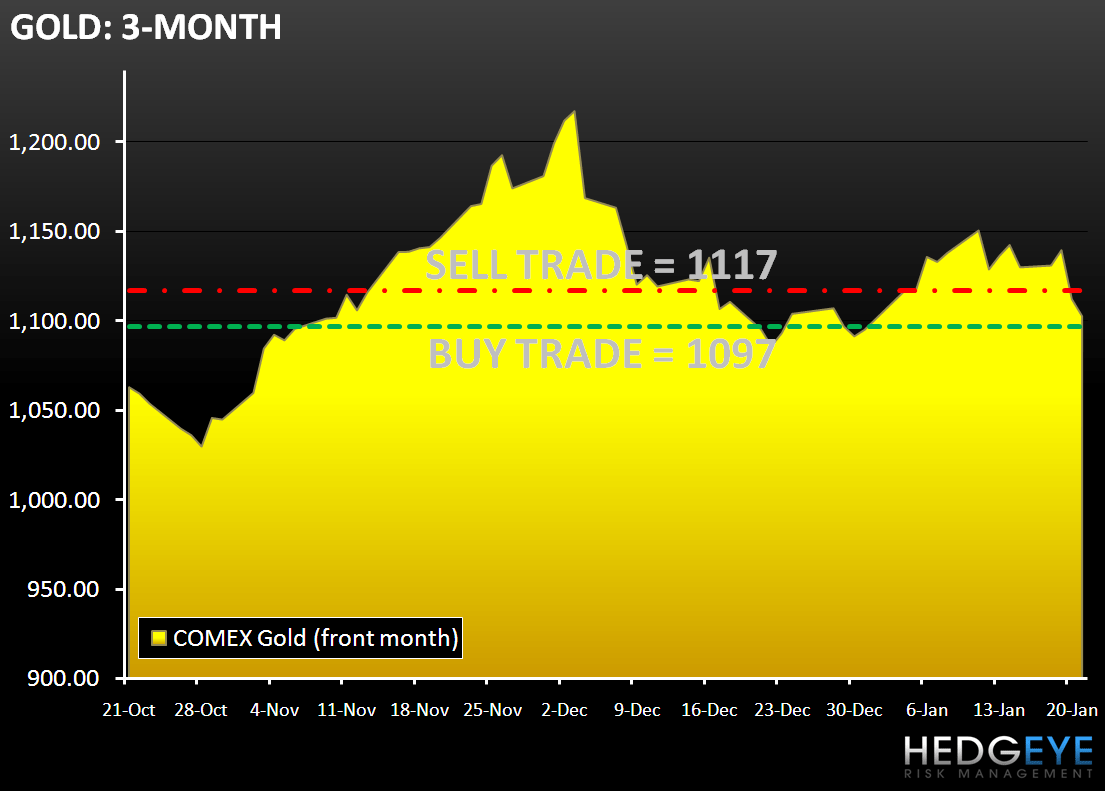

In early trading today Gold is declining for the third straight day. The Hedgeye Risk Management models have the following levels for GOLD – buy Trade (1,097) and Sell Trade (1,117).

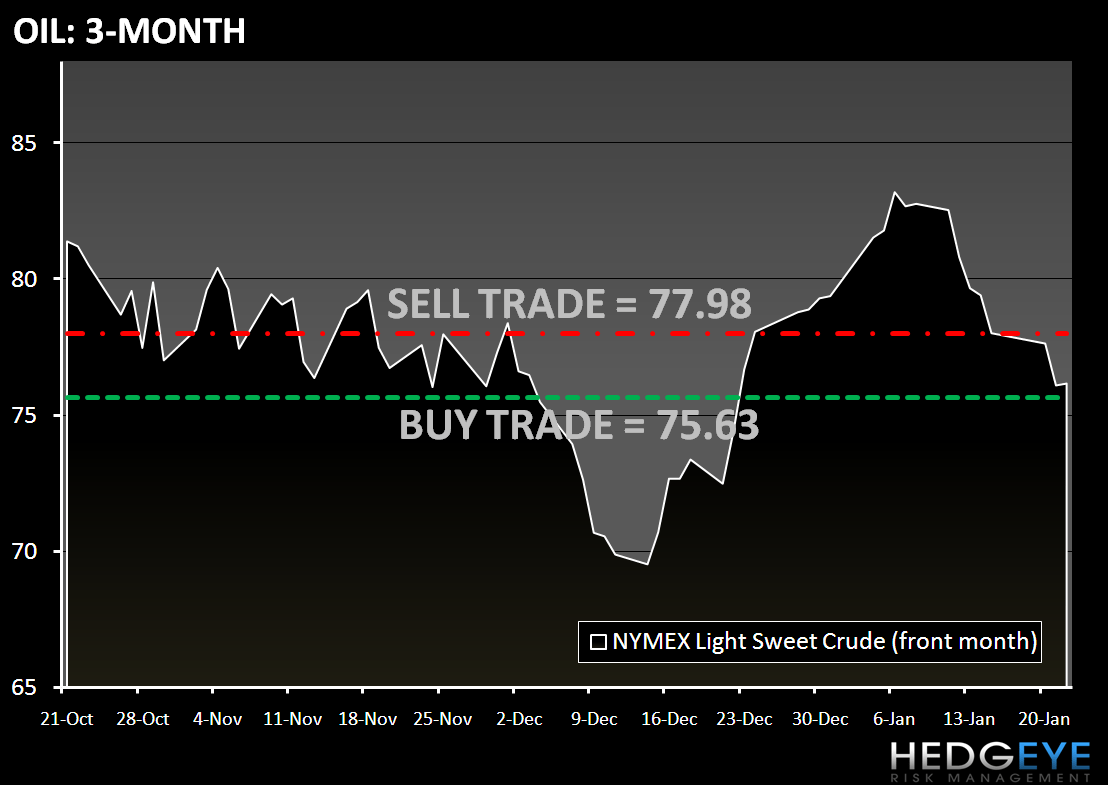

In early trading, crude oil is trading flat after declining 2.1% yesterday. Crude looks poised for a second weekly decline, on the back of a slowing China and increased supplies. The Hedgeye Risk Management models have the following levels for OIL – buy Trade (75.63) and Sell Trade (77.98).

Howard Penney

Managing Director