Copper production in China hit record levels in 2009. According to the Chinese Statistics Bureau, output of refined copper gained 9.6% y-o-y to 4.25 million metric tons. Clearly, a large driver of this increase was China’s stimulus program in 2009.

China accounts for ~40% of global copper demand. As our thesis on China continues to play out in Q1, Chinese Ox In A Box, and China slows sequentially in Q1, it will have a negative impact on copper demand. We are seeing some follow through on this today with copper futures currently down ~1.2% based on the Chinese economic data released last night and comments from the Chinese government regarding fiscal policy.

Mining stocks echoed concerns over this potential slow down from China yesterday. The world’s largest mining company BHP Billiton reported results yesterday According to BHP:

“Government stimulus measures appear to have supported a gradual return to normalized trade levels, albeit from a low base."

Clearly, to the extent that government stimulus is not repeatable year-over-year, demand for copper should slow sequentially from Q4 2009.

In fact, concern over a potential slowdown in copper demand due to a slowing of government stimulus from China appears very justified. Over the past couple of days, based on both a statement from Premier Wen Jiabao and a statement from the Chinese Statistics Bureau that removed reference to a “moderately loose” fiscal and monetary policy. This, of course, suggests that China will be tightening policy. Reports from China suggest that the new policy will be finalized by the time the National People’s Congress meets in March. This is on the back of China’s attempt to slow loan growth.

On this point, BHP also stated in their earnings release:

“In China, the impact of measures to control loan-growth will add another future variable. Consequently, we expect some degree of volatility in the short term outlook for our commodities.”

Clearly, the world’s mining companies have and are proactively preparing for the Chinese Ox In A Box, which is critical for managing their businesses. According to a recent report by the Copper Study Group:

“Through October, Chinese production of refined copper grew by 43% to 1.8 million metric tons to account for 40% of world use-and nearly offset and 18% decline in the rest of the world. Use decreased by 21% in the European Union, by 31% in Japan, and by 21% in U.S.”

In effect, China contributed all of the world’s incremental demand last year, which is why the global mining community have their Hedgeyes focused on China.

We are also starting to see a mismatch in supply and demand in global inventories. Yesterday, copper inventories on the LME were reported up 8,000 tonnes to reach 534,650 tonnes, which is the highest level since March of 2009.

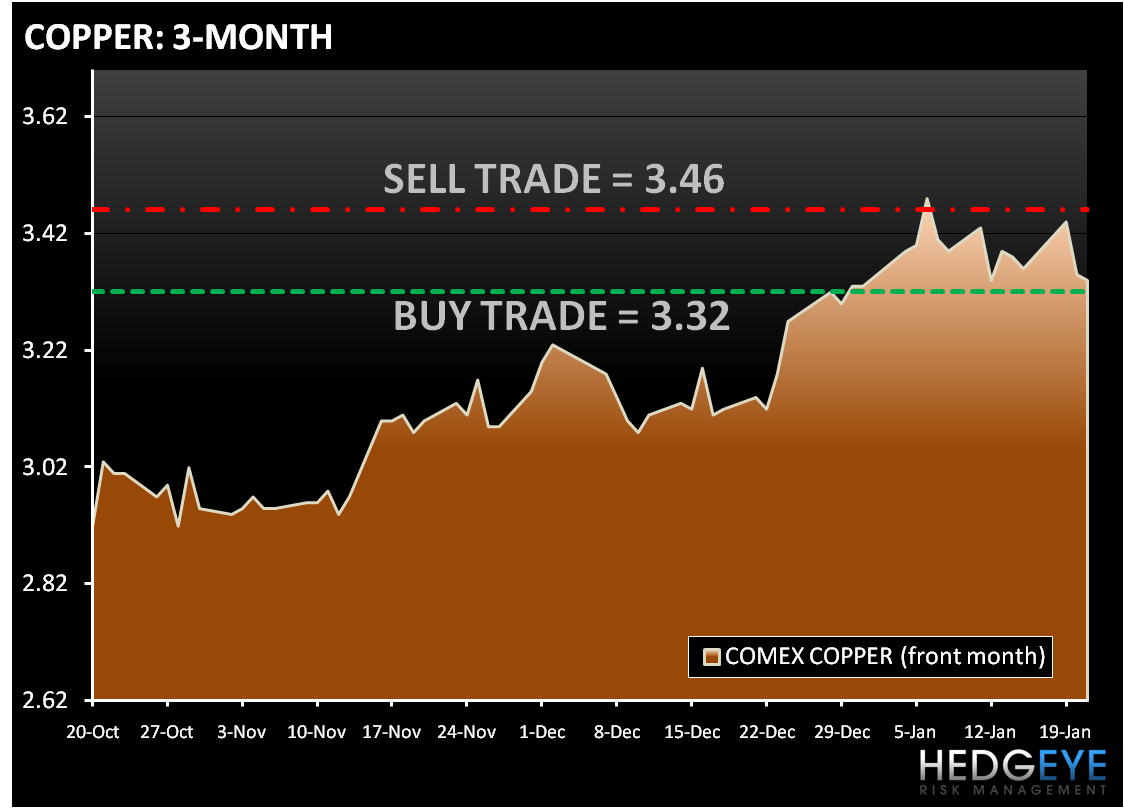

Currently, copper appears to be a leading indicator for the Q1 slow down in China. Additionally, copper supply and demand fundamentals are lined up bearishly in the intermediate term. Below, we’ve outlined our current levels on copper as of this morning.

Daryl G. Jones

Managing Director