As speculation abounds today that the European Union could offer Greece a rescue package to address its budget deficit issues, the reality remains that the lack of credibility in PM George Papandreou’s government is a serious one that looks far from over.

While a rescue package is at best a rumor right now, we’re of the camp that the fiscally conservative Germans, represented by Bundesbank President and ECB member Axel Weber, will attempt to own the debate and force Greece to clean up its own mess before the international community considers floating a deal.

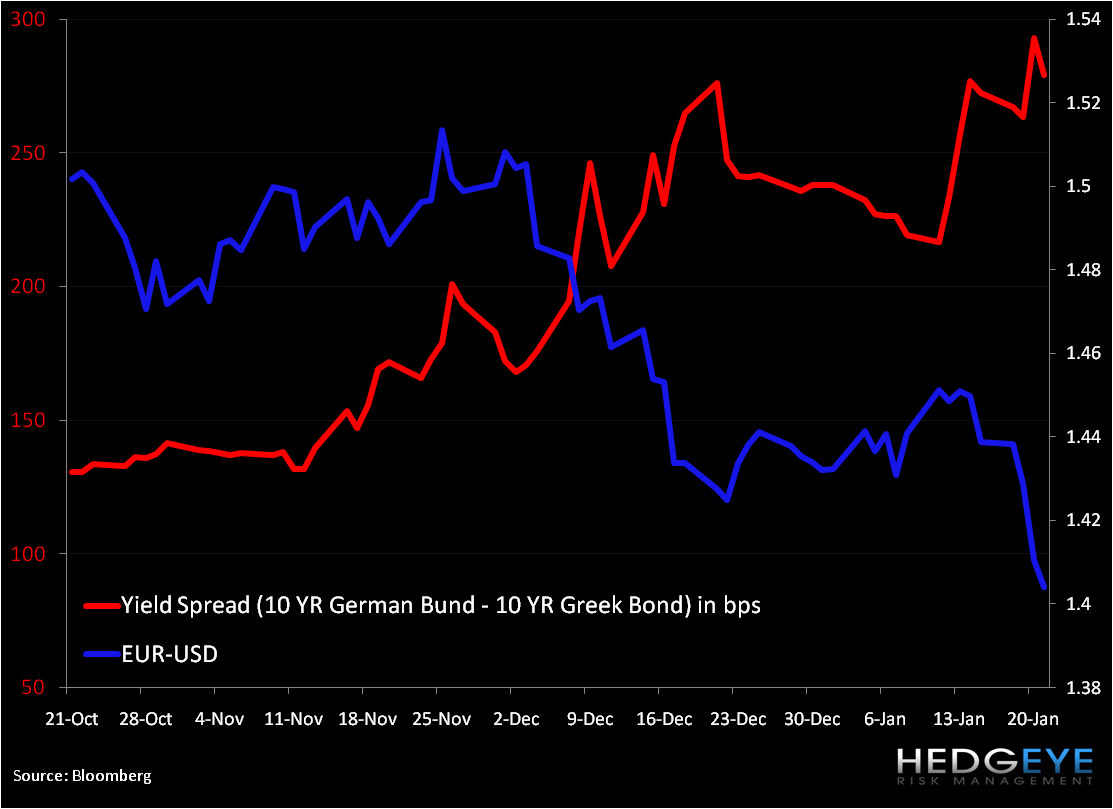

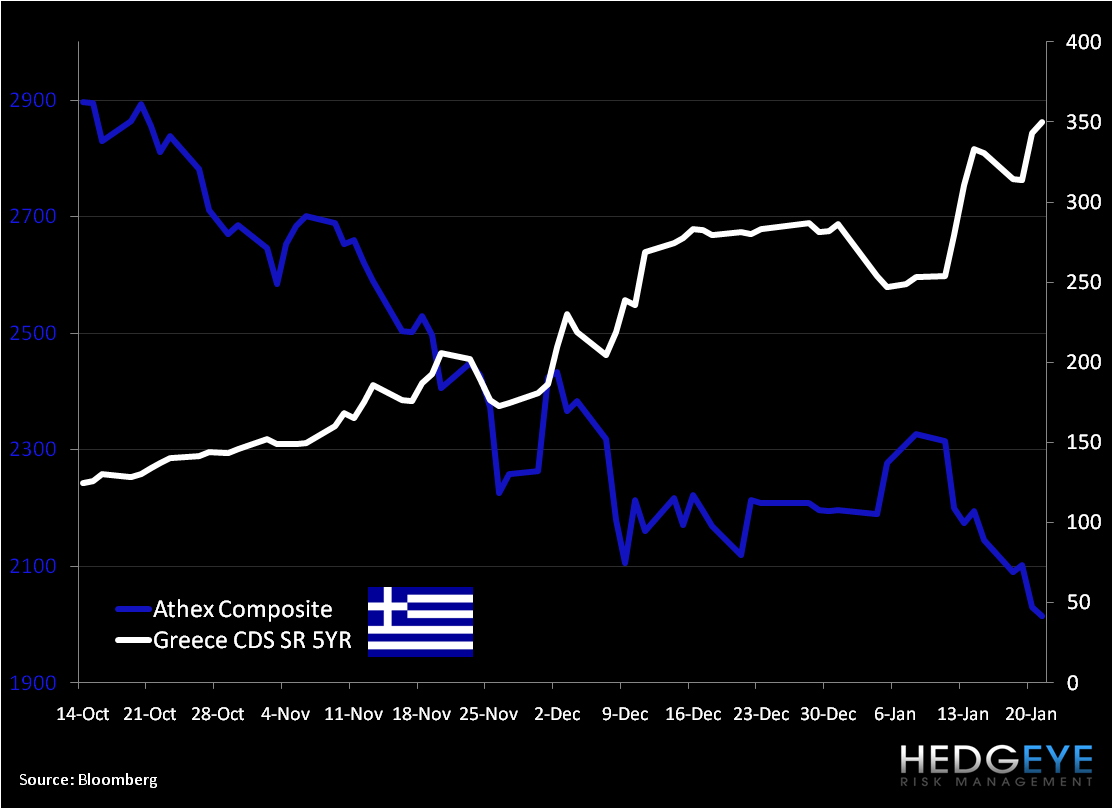

As the uncertainty over the Greek state continues, we’re seeing the premium investors demand to hold Greek debt continue to balloon, as the chart below shows the spread between the yield on the 10YR German bund and the 10YR Greek bond continue to blow out. While the spread is just off its widest in the intermediate term, certainly the trend to the upper-right hand corner is bearish, especially if supply outstrips demand. All the while, the country’s domestic equity market (Athex Composite) has been hit hard over the last week, as CDS prices continue to run up.

We’ve had our pulse on the possible ripple effects from a shaking Greece. Note the recent depreciation of the Euro versus the US Dollar, down 3.2% since 1/13, and indication to us that while the Greek economy is around less than 10% of the German economy (or roughly the size of the German state of Bavaria), the issues surrounding Greece call into question similar stresses that may be ailing other European countries. In our 1Q 2010 Theme call we noted that the countries of Spain, Italy and Portugal are on our watch list.

While we covered our short position in the Euro via the etf FXE in our model portfolio on 1/19 (regrettably a tad bit early), we remain long the USD via UUP.

Matthew Hedrick

Analyst