The S&P rolled over on Wednesday, with all of the major indexes finishing down more than 1% on the session. Tuesday’s euphoria over the election in Massachusetts was quickly overcome by the potential for Congressional gridlock on a number of important issues. Overall the volume was still light, but was up 1.9% day-to-day; breadth was the worst it’s been all year.

The Hedgeye RISK Management sector models saw a breakdown yesterday in two sectors – XLY and XLU – both broke TRADE. All nine sectors declined yesterday and all nine are positive on TREND.

On the MACRO front, the “CHINESE OX IN A BOX” and liquidity concerns were on the front burner as the focus was on Beijing's efforts to curb new bank lending. Not surprisingly, this dynamic weighed on the RECOVERY trade as the Dollar Index continues to trade higher. Of the three worst performing sectors two are leveraged to the RECOVERY TRADE - Materials (XLB) and Energy (XLE).

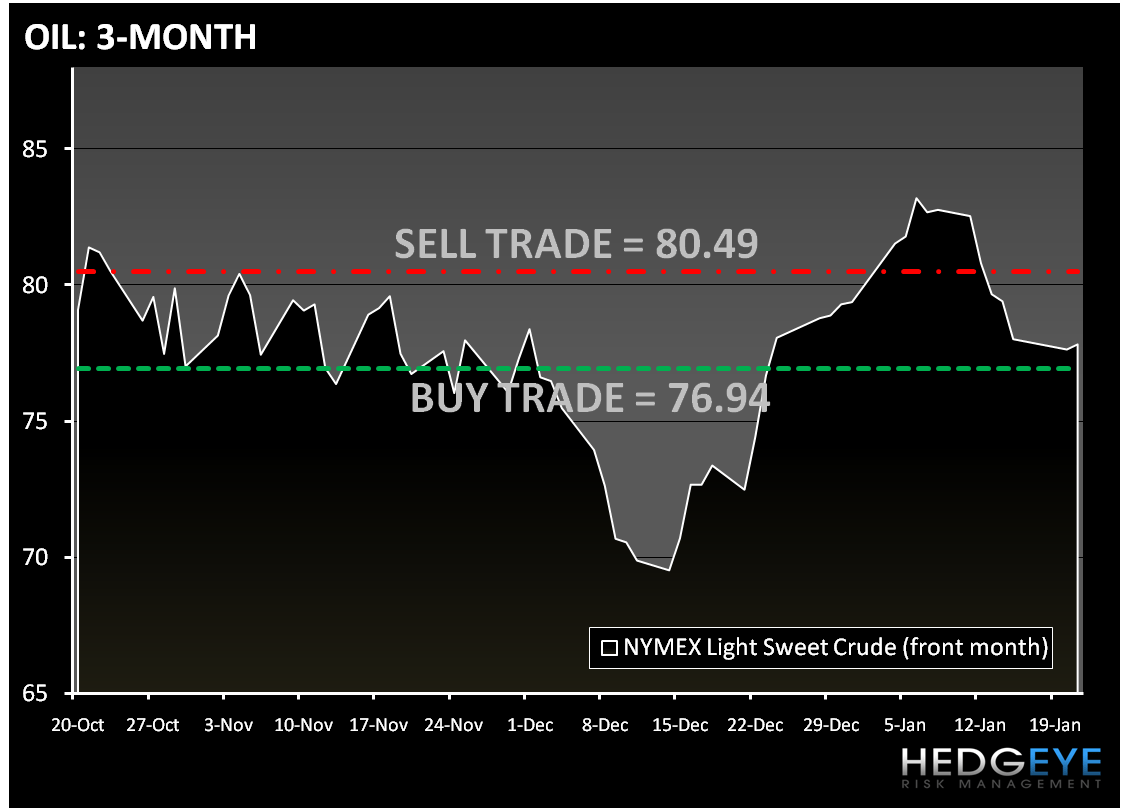

The XLE and XLB were also hit by the strength in our “BUCK BREAKOUT” theme, which underpinned the safe haven status (i.e. better fiscal outlook now that Democrats have lost in Massachusetts and heightened risk aversion with the VIX up +6.1% on the day yesterday. Precious metals and industrial stocks were among the biggest decliners in the XLB, while higher-beta coal and oil services stocks were underperformers in the XLE sector. On Wednesday, crude closed down 1.9% to $77.74 a barrel.

Also on the MACRO front the MBA mortgage applications slowed to 9.1% from 14.3% and housing starts declined 4% from 8.9% last month. On the positive side building permits were 653,000 vs. 584,000 last month.

Also taking center stage on the downside was Technology (XLK). The XLK underperformed yesterday despite the Q4 earnings beat from IBM. There was weakness in the software group today, with the S&P Software Index declining 1.4%, while the Semis held up better than the broader XLK.

The best performing sector yesterday was the Financials (XLF), down only 0.3% on the day. Within the XLF the banking group bucked the broader market selloff today with the BKX up 1.4% with the Trust names (STT, NTRS and BK) trading higher following their Q4 earnings results. Regional banking stocks are also performing wells after their Q4 earnings reports.

As we look at today’s set up the range for the S&P 500 is at 20 points or 0.43% (1,133) downside and 1.05% (1,150) upside. At the time of writing the major market futures are trading down on the day.

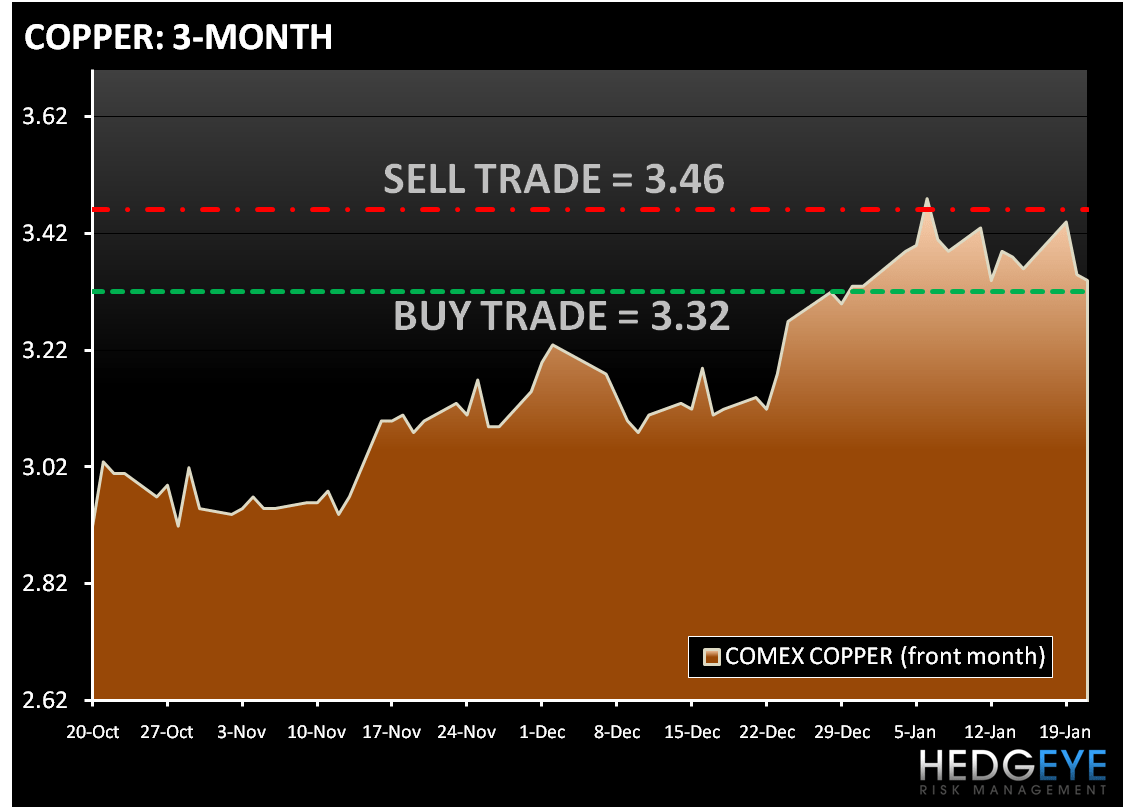

Copper imports by China, climbed for a second month in December on rising demand. Despite this news Copper traded down 2.67% yesterday and is flattish in early trading today. The Hedgeye Risk Management Quant models have the following levels for COPPER – buy Trade (3.32) and Sell Trade (3.46).

In early trading today Gold is declining for a second day, after falling 2.4% yesterday; the biggest decline since December 17, 2009. The Hedgeye Risk Management models have the following levels for GOLD – buy Trade (1,101) and Sell Trade (1,134).

Yesterday crude traded down by 1.9%, and is trading slightly lower in early trading today. The strength in the Dollar and increased inventories are putting pressure on oil. The Hedgeye Risk Management models have the following levels for OIL – buy Trade (76.94) and Sell Trade (80.49).

Howard Penney

Managing Director