Last week the S&P 500 traded down 1.08% on Friday and finished lower by 0.78% for the week. The number of shares traded on the NYSE was the biggest so far this year and the decliners outnumbered advancers approximately 3 to 1.

No sector was up on the day, although six sectors did outperform on a relative basis. Only one sector, Utilities, broke TRADE on the Hedgeye Risk Management quant models.

As we look at today’s set up the range for the S&P 500 narrowed from 35 points on Friday to 20 points or 0.44% (1,131) downside and 1.32% (1,151) upside. At the time of writing the major market futures are trading flattish on the day.

On the MACRO front, the markets had a number of mixed economic data points to consider on Friday. First, January preliminary University of Michigan confidence was slightly disappointing at 72.8 versus consensus 74. Second, December Industrial Production was in line at 0.6%, while November was revised down to 0.6% from 0.8%. December Capacity Utilization was 72.0% versus consensus 71.8%; while November was revised up to 71.5% from 71.3%. Third, December CPI was 2.7% versus consensus 2.8% versus the November reading of 1.8%. On the positive side of the MACRO data January Empire Manufacturing was 15.92, much stronger versus consensus 12.

Treasuries rallied across the curve on Friday and the dollar index was up 0.77% on the day; the Dollar index had its first up day in the last five trading days. The increase in the dollar pressured commodities as Oil and Gold traded down on the day.

The worst performing sector last Friday was Financials (XLF). Within the XLF, the Banks lead the sector lower with the Bank Index (BKX) down 2.1%, with the investment banks weaker too. While the Obama “responsibility tax” was front and center it was JPM earnings that were the key negative data point for the day. As it related to JPM, revenues disappointed and there were lots of questions raised about the quality of the quarter with an outlook less robust. Regional banks were also weak on the day.

Technology (XLK) was the second worst performing sector on the day, as the Semiconductor index (SOX) declined 3.4% on the day. INTC declined 3.1% despite reporting a good quarter last, although higher than expected inventory and unsustainable gross margin concerns were an issue.

On a relative basis, the best performing sector last Friday was the Consumer Staples (XLP). The XLP benefitted from KFT as it improved 1.6% on the day. Consumer Discretionary performed in line with the market, down 1.1%; the XLY was facing a bearish consumer confidence number.

Yesterday, the CRB index closed lower 1.02% on the back of a decline in Energy commodities; nearly every other major commodity traded higher last Friday.

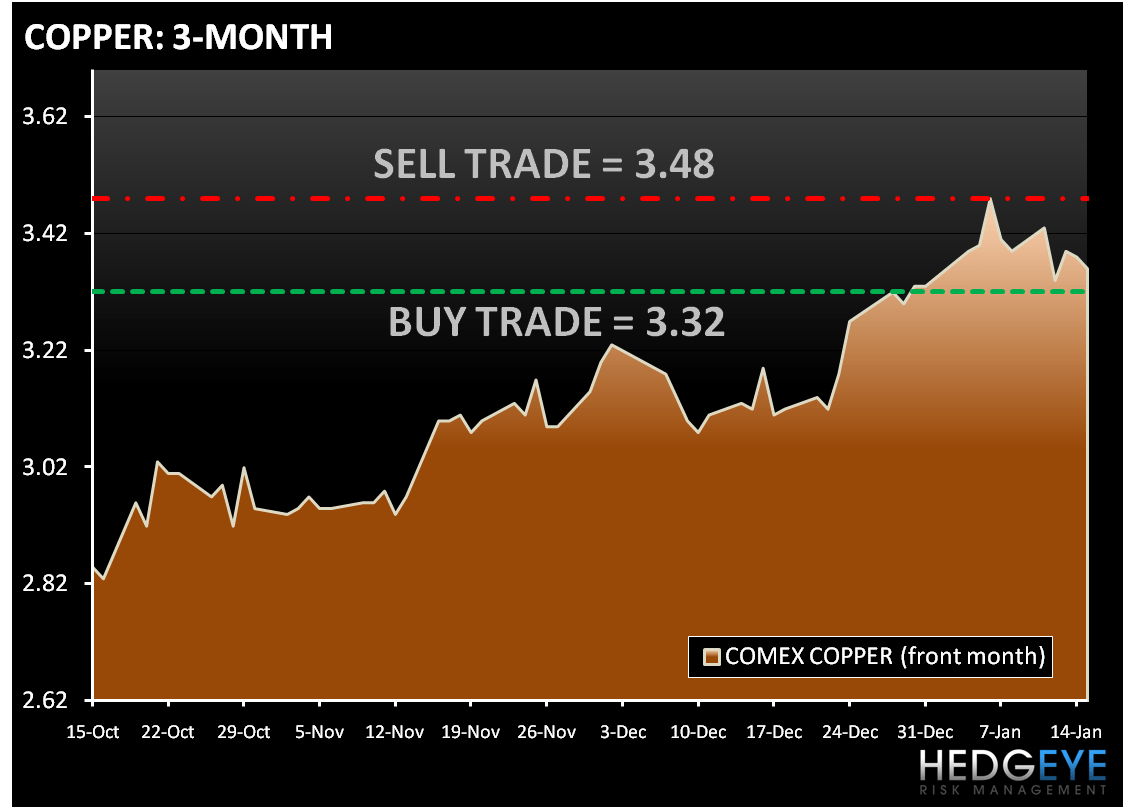

In early trading Copper is trading up 1% after declining for the previous two days. The Hedgeye Risk Management Quant models have the following levels for COPPER – buy Trade (3.32) and Sell Trade (3.48).

In early trading Gold is trading down about 0.2% to 1,131. GOLD continues to underperform especially when compared to other precious metals. Gold continues to trade in a fairly tight range and consolidating around the 1,130 level. The Hedgeye Risk Management models have the following levels for GOLD – buy Trade (1,118) and Sell Trade (1,153).

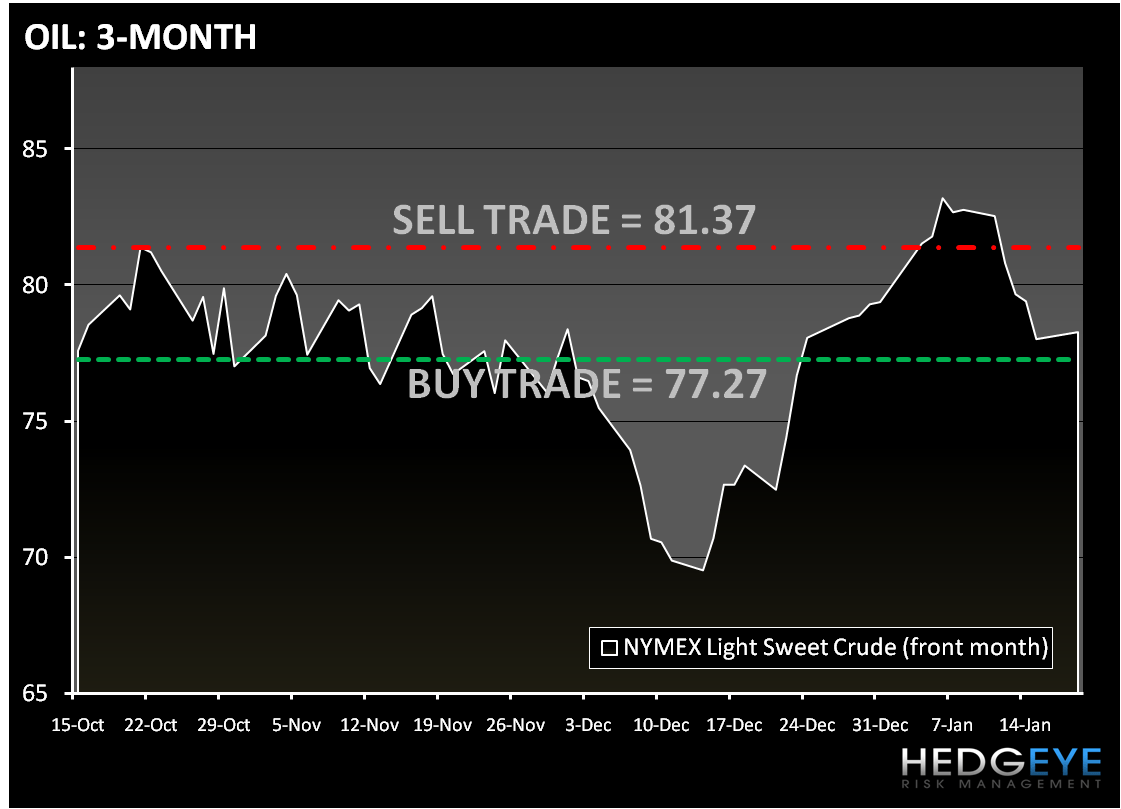

Last week crude oil traded lower for five straight days, declining 5.7%, and is trading down flat in early trading today. The Hedgeye Risk Management models have the following levels for OIL – buy Trade (77.27) and Sell Trade (81.37).

Overnight most Asian markets traded to the downside, although China ended slightly higher on the day. The Chinese market traded higher, despite the fact that China raised its yield on one-year bills for the second week in a row. Europe is down across the board, after trading higher on Monday.

Howard Penney

Managing Director