For a simple takeaway... earnings growth remains resilient on the heels of an accelerating economy. In attempting to look beyond our jamming of "QUAD1" into email inboxes, the forward-looking reality is that aggressive revisions in front of difficult comps have made meeting earnings expectations a high order in coming quarters, particularly in Q1 of 2018. Unfortunately for this narrative, the Q1 2018 "event" is about 5-6 months away. However, this sine curve reality meets a potential corporate tax windfall for a cocktail of uncertainty.

So far this reporting season, earnings have come in strong, but the "beat" rates have been much less drastic due to the information technology driven earnings revisions in previous quarters.

Here are some quick-hit takeaways with visuals below:

- Q3 Earnings Growth: So far earnings growth has come in at +7.1% YY for the S&P 500 in aggregate which would be a slight deceleration from +9.7% in Q2, a trivial point at the center of our Q4 Macro Themes presentation. Embedded in that number is +29.0% Y/Y earnings growth for 26/68 companies in the information technology sector.

- Beat Rates: An important takeaway of Q3 reporting season thus far is that earnings beat rates are well below previously revised, higher expectations at +3.1% YY for the S&P 500 index vs. a 5-yr average beat rate of +4.2%. In Q1 and Q2, earnings growth in the information technology sector of S&P 500 constituents was +21.7% & +15.8% Y/Y which ultimately crushed expectations. The "beat" rates greatly outpaced average beat rates. Translation = Earnings season was a definitive catalyst for the stocks.

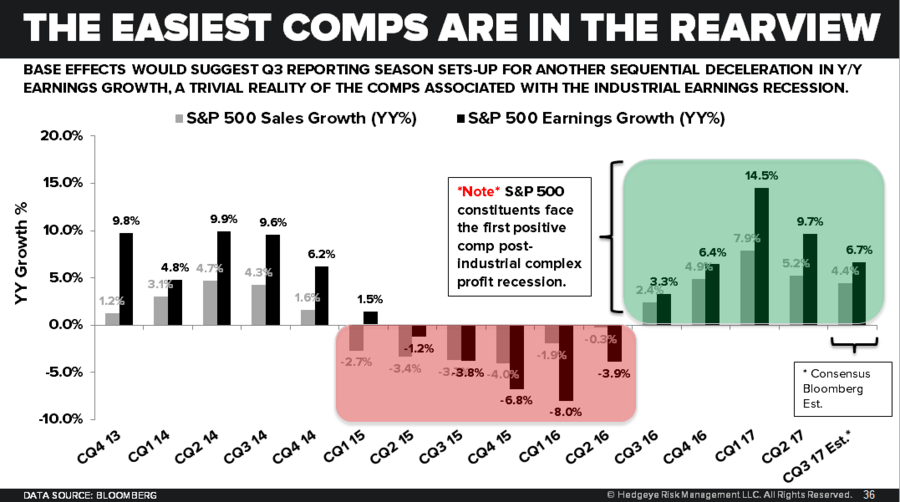

- Past Peak Growth Rates?: Now we’re not getting off our QUAD1 horse (See our Early Look from yesterday morning on earnings), but comps get much steeper in Q4 for corporate profits and especially in Q1 of 2018 which we would label as the big headwind quarter. Q3 of 2016 is the first positive base rate since Q4 of 2014. Thereafter comps steepen significantly (Q1 of 2017 was the strongest comp of +14.5% earnings growth for S&P 500 constituents).

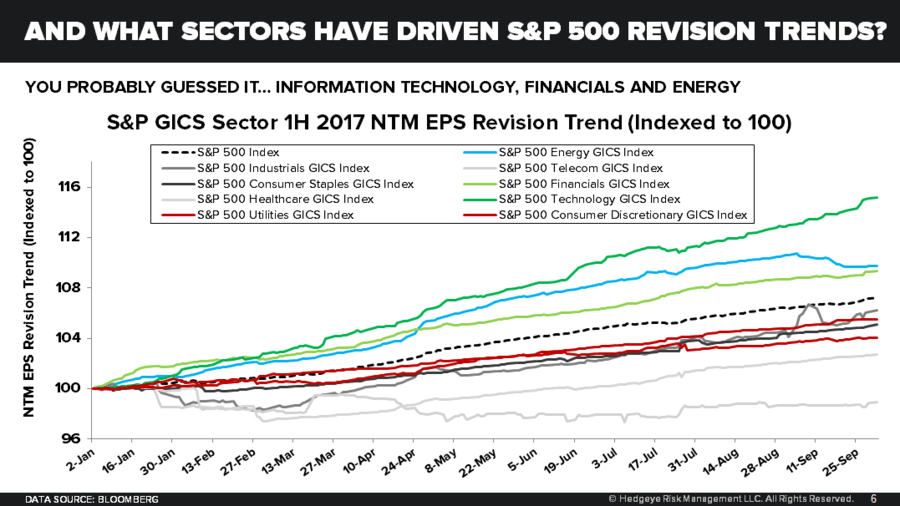

- Revision Trends & Market Multiples: Revision trends in the technology sector have been by far the largest contributor to more muted forward market multiple expansion given market returns in 2017. For Context, earnings growth for Q3 has come in at +29.0% Y/Y with 26/68 companies in the information technology sector having reported, but because of forward revision trends, this growth rate translates to a “beat” rate that has decelerated from Q2. However, a beat rate of +5.1% is still beating the trailing 5yr average of +3.9%. So all in, a positive #growthaccelerating start to earnings season with lofty revisions and multiples to grow into in the face of difficult comps.

---------

Q3 Earnings Growth

So far earnings growth has come in at +7.1% YY for the S&P 500 in aggregate which would be a slight deceleration from +9.7% in Q2, a trivial point at the center of our Q4 Macro Themes presentation. Embedded in that number is +29.0% Y/Y earnings growth for 26/68 companies in the information technology sector.

The headline growth rates in the Nasdaq 100 index also have the wow factor from the information technology sector (+85% YY for 13 of 40 tech companies). On the whole earnings growth has so far come in at +27% YY for 37/102 companies that have reported.

In the Russell 2000, 448/1956 companies have reported aggregate earnings growth of +12.0% YY. If this trajectory were to be hold, it would be a sharp acceleration from a negative print in Q2 of -4.1% for the index.

Beat Rates

An important takeaway of Q3 reporting season thus far is that earnings beat rates are well below previously revised, higher expectations at +3.1% YY for the S&P 500 index vs. a 5-yr average beat rate of +4.2%. In Q1 and Q2, earnings growth in the information technology sector of S&P 500 constituents was +21.7% & +15.8% Y/Y which ultimately crushed expectations. The "beat" rates greatly outpaced average beat rates. Translation = Earnings season was a definitive catalyst for the stocks.

Past Peak Growth Rates?

Now we’re not getting off our QUAD1 horse (See our Early Look from yesterday morning on earnings), but comps get much steeper in Q4 for corporate profits and especially in Q1 of 2018 which we would label as the big headwind quarter. Q3 of 2016 is the first positive base rate since Q4 of 2014. Thereafter comps steepen significantly (Q1 of 2017 was the strongest comp of +14.5% earnings growth for S&P 500 constituents).

We put a heavy weighting on rate of change, and in reality the earnings growth accleration four 4+ quarters came on the back of a broad-based slowdown in corporate profits. As the first chart below demonstartes, the corporate profit recession of Q2 2015 - Q2 2016 was broad-based and not siloed within commodity sectors. The 21.7% & 15.8% Y/Y earnings growth rates in Q1 and Q2 of 2017 for the information technology sector of the S&P 500 came on the back of -7.4% and -2.7% growth rates in Q1 and Q2 of 2016. So our view is that the 21.7% comp will be a major headwind in Q1 of 2018, but a quick look at the calendar reveals the "event" is 5-6 months away.

Revision Trends & Market Multiples

Revision trends in the technology sector have been by far the largest contributor to more muted forward market multiple expansion given market returns in 2017. For Context, earnings growth for Q3 has come in at +29.0% Y/Y with 26/68 companies in the information technology sector having reported, but because of forward revision trends, this growth rate translates to a “beat” rate that has decelerated from Q2. However, a beat rate of +5.1% is still beating the trailing 5yr average of +3.9%. So all in, a positive #growthaccelerating start to earnings season with lofty revisions and multiples to grow into in the face of difficult comps.

Ben Ryan

dty