KEY POINTS

- 3Q17 = Further Deterioration: TRVG had previously suggested that 4Q revenue growth should reaccelerate off of 3Q17, but its updated 2017 guidance suggests 4Q revenue will decelerate further in the LSD to low-teens range vs. 17% growth in 3Q17. Mgmt also implied in its release that 1H18 revenue may decline (although it wouldn't confirm as much during the call). Mgmt suggested that revenue concentration amongst its largest advertisers started declining in 4Q17, which confirms that PCLN is paring back on its Trivago ad spend.

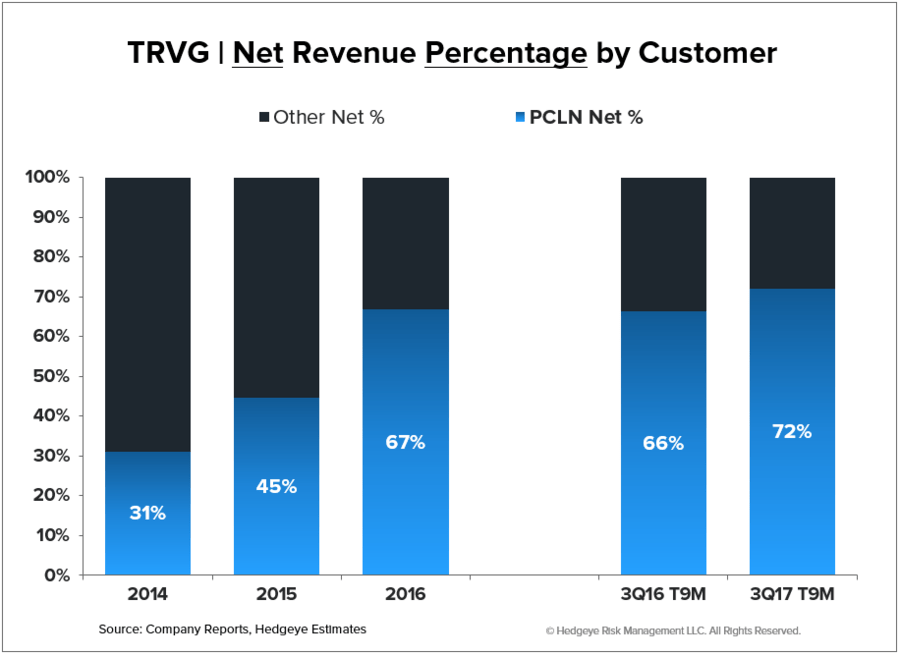

- TRVG's Model is now Structurally Defunct: The two central tenets of our analysis of its model 1) TRVG is hostage to PCLN & EXPE and 2) its inventory is tethered to its ad spend (see deck below). The first point is now more important since there is no point in acquiring (paying for) traffic unless you have a buyer to resell it to (PCLN represented over 70% of its net revenues in T9M). Further, TRVG suggested the pressure is coming in the form of CPC rates, so for all we know PCLN is now bidding less for TRVG's traffic than what TRVG has to bid to acquire it. But at a minimum, TRVG's ad budget/inventory is funded by revenues collected in the preceding quarters, so if PCLN is paring back its Trivago ad spend, then TRVG will struggle to drive inventory growth in subsequent quarters, and so on so forth…

- Implications for PCLN, EXPE, TRIP: The only clear takeaway is that PCLN is paring back on Trivago ad spend, which isn't necessarily indicative of a pullback in its performance-based ad budget since PCLN may just be shifting that budget toward other online channels (SEM/Google). It’s unclear what this means for TRIP since we’re not sure if PCLN is paring back on meta, or is specifically targeting TRVG given how quickly PCLN’s Trivago ad budget (i.e. TRVG’s net revenues) had grown over the LTM. However, the positive is that TRVG will be paring back on its traffic acquisition efforts, so a less of a headwind for TRIP (although TRIP is also paring back to fund its TV budget, so may not matter). EXPE also pared back its Trivago spend meaningfully into 3Q (growth decelerated 62 percentage points), which we suspect is mostly a function of TRVG's constrained inventory rather than EXPE's desire to buy it. But we estimate that TRVG has been a meaningful source for EXPE's room night growth over LTM, so EXPE could see incremental pressure on room night growth starting 4Q17.

TRVG | What You Need to Know

Jan 9th, 2017

[click here]

See deck above for supporting detail on our TRVG analysis. Let us know if you have any questions.

Hesham Shaaban, CFA

Managing Director

@HedgeyeInternet

Todd Jordan

Managing Director

@HedgeyeSnakeye

Sean Jenkins

Associate