Essentially we have traversed the nasty part of the “GREAT RECESSION” and we are on the path to recovery. We have moved from a 3Q09 theme of “REFLATION ROTATION” to “RATE ROTATION” in 4Q09 and now we believe that interest rates are headed higher. One of our key themes headed into 1Q10 is “RATE RUN-UP”:

(1) The FED is behind the curve and the next few data points on the US economy and employment will drive interest rates higher.

(2) Inflation is evident in a number of places, but primarily reflects the effects from higher energy prices.

(3) Feeding the rich at the trough of the Yield spread.

The consensus believes (and it is likely true), that there are some factors supporting the USA economic recovery that are of temporary nature. There is no denying that the financial “crisis” is behind us and that the economy is on more solid footing. SO why does the Fed maintain rates at a “crisis” level?

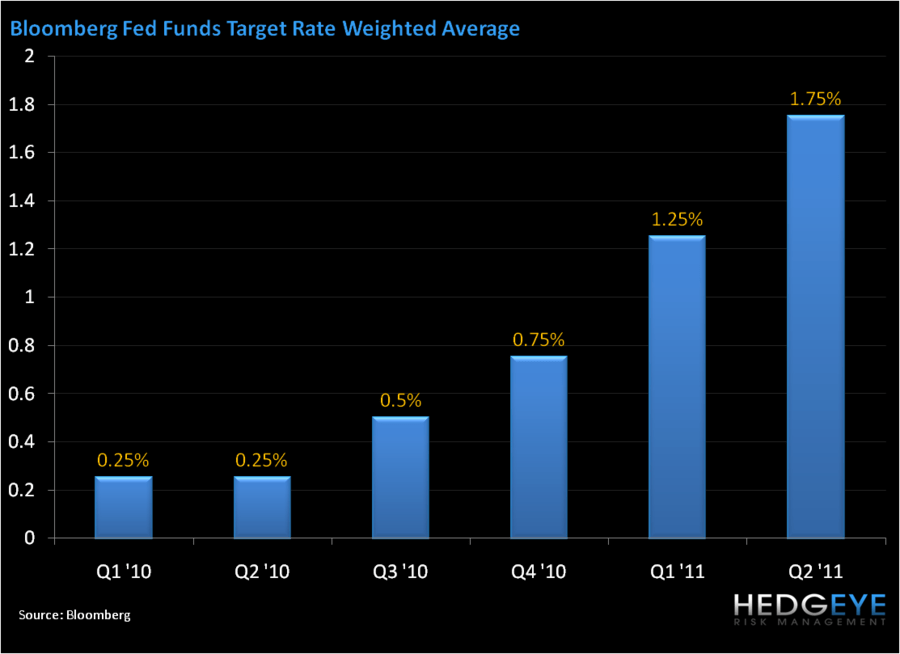

Current street expectation for an increase in the FED funds target rate is not until 3Q10. Our view is that FED will likely be changing its policy statement at the next meeting and that an actual interest rate increase is not far behind.

One of the biggest issues with the current interest rate policy is that it is feeding the rich and starving the poor. The yield spread (10-year minus 2-year Treasury yields) is trading at 281 basis points wide and peaked out at +288 basis points wide on January 11, 2010. The spread is killing the average American’s saving account and is providing the best ever environment for Investment Banking Inc. to print money.

While the next few data points on jobs and the economy will point to improved growth, the underlying pace of growth is still in question. Clearly manufacturing is getting a boost from inventory corrections and pent up demand; the upward trend in industrial production, ISM, capacity utilization, and new orders for nondefense capital goods all look strong. But consumers sentiment is not improving and his/her balance sheets are not financially sound.

All in, the net-net impact has been to stem the pace of job losses and, if temporary help and the census hiring trends is a leading indicator, set the stage for and improvement in the unemployment rate and the potential for actual gains in nonfarm payrolls in the months ahead. In the short run, interest rates are headed higher, but all of this is setting the stage for a challenging 2H10 given the likelihood that growth slows as government stimulus will eventually come to an end.

Howard Penney

Managing Director