For the eight day this year the S&P was up on the day, rising 0.24%. Volume was very light on the NYSE, declining 8% sequentially and 54% below the average daily volume for 2009. With INTC reporting earnings last night and JPM expected shortly, earnings season is about to get into full swing.

On the MACRO front the market largely ignore bad news, as yesterday’s performance came despite an unexpected decline in December retail sales. In fact the Consumer Discretionary was the third best performing sector yesterday. Within the XLY, retail stocks underperformed with the S&P Retail etf down 0.82%.

The MACRO calendar was the headwind for the group after retail sales fell 0.3% month-to-month in December vs. consensus expectations for a 0.5% increase. The big category decliners included autos (-0.8%), general merchandise (-0.8%), food/beverages (-0.8%) and clothing (-0.6%).

The best performing sector yesterday (for the second day in a row) was Healthcare (XLV). Within the XLV, managed care was a bright spot with the HMO +1.4%, despite reports of progress in terms of merging healthcare reform legislation from the Senate and the House.

Surprisingly, the XLF (the second best performing sector yesterday) was able to shake off the formal announcement from the Obama administration regarding its bank tax proposal. Within the XLF, the bank stocks extended its two day rally up 1.64%. Also, the regional bank names continued to outperform with the KBW Regional Bank etf up 3.05%.

While not one of the top three performing sectors, Technology (XLK) outperformed the S&P 500 for a second straight day. A big chunk of support came from the software group, with the S&P Software Index up 1.69%. Outside of software, the SOX declined 0.6%. INTC rallied 2.5% ahead of its Q4 results and is trading 3% higher in early trading after blowing out 4Q numbers.

Parts of the RECOVERY trade underperformed yesterday. Yesterday, Energy (XLE) outperformed, but the Materials (XLB) was the worst performing sector on the day. Metals, mining and Chemical stocks were the worst performing stocks in the etf.

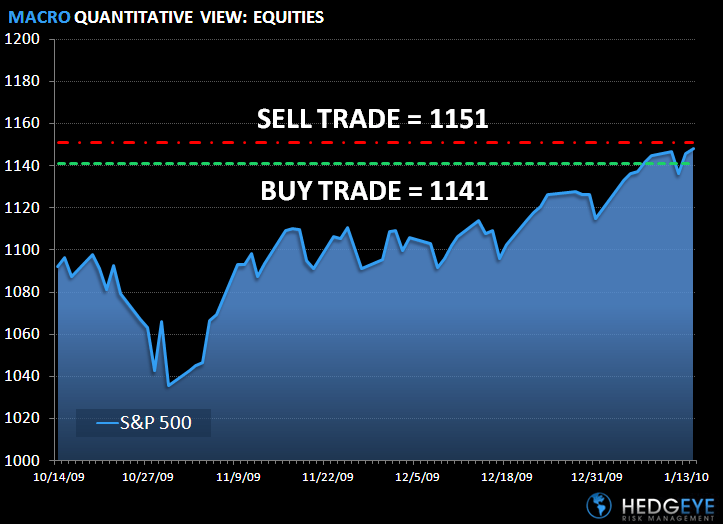

The range for the S&P 500 is 10 points or 0.6% (1,141) downside and 0.2% (1,151) upside. At the time of writing the major market futures are trading lower on the day.

Yesterday, the CRB index closed lower 0.25% on the back of a decline in Energy, Grains and Precious Metals. Livestock and Industrial commodities traded higher on the day.

Copper stockpiles advanced 1.8% in Shanghai this week to the highest level in almost a month, according to the Shanghai Futures Exchange. In early trading today Copper is trading lower, after declining 0.37% yesterday. The Hedgeye Risk Management Quant models have the following levels for COPPER – buy Trade (3.33) and Sell Trade (3.49).

In early trading Gold is trading down about 1% to 1,131. The Hedgeye Risk Management models have the following levels for GOLD – buy Trade (1,119) and Sell Trade (1,154).

Yesterday, crude oil traded lower for the fourth day in a row and is trading down 1% in early trading today. Oil has traded down about 5% this week. The Hedgeye Risk Management models have the following levels for OIL – buy Trade (77.10) and Sell Trade (81.72).

Howard Penney

Managing Director