Yesterday, all of the major indexes posted their biggest one-day losses for 2010 on accelerating volume. The Hedgeye Risk Management models are still showing that the TRADE and TREND for the S&P 500 is BULLISH, while the Utilities (XLU) is the only sector to be broken on TRADE.

We woke up to another round of the Chinese withdrawing stimulus yesterday, which contributed to markets posting their biggest one-day losses in 2010. Also, the People’s Bank of China raised the proportion of deposits that banks must set aside as reserves by 50 basis points starting Jan. 18.

THE CHINESE OX IS IN A BOX!

On the MACRO front it was another quiet day which means there are no vapors to help push the RECOVERY trade higher. The VIX also had its biggest one day move in 2010 rising 3.9%. With the VIX down 15.8% so far in 2010, investor complacency has crept into the market. The Chinese can clear that up quickly if you are not paying attention.

The best performing sector yesterday was the Consumer Staples (XLP). The grocers and food stocks were the bright spot in the staples after the Q3 earnings beat and upwardly revised guidance from SVU and KFT. HSY was the best performing packaged food stock on reports that Ferrero ended talks with the company regarding a rival bid for Cadbury.

Yesterday in the US the Materials (XLB) was the worst performer. The XLB is one of the sectors with the most leverage to the recovery trade, as the CHINESE OX IN A BOX theme will work against the XLB. In addition, aluminum stocks were hit hard in the wake of the earnings miss from AA. The fertilizer, steel and precious metals stocks all finished lower on the day.

The Financials have seemed to run into a brick wall on the back of increased regulatory concerns. The renewed regulatory concerns were grounded amid reports that the Obama administration is considering assessing some kind of tax on banks to help close the budget deficit and recoup TARP losses. The banking group finished lower for just the second time this year, with the BKX down 1.7% on the day. Within the XLF, the large-cap names BAC, C, WFC and JPM were among the worst performers. The weakness in the XLF also included the brokers, with MS down 2.84% and GS down 2.18%, the latter of which finished down for a third straight day.

The Technology (XLK) underperformed the S&P 500 by 20bps, as the SEMI stocks weighed heavily on the sector with the SOX down 3.59%. The SOX suffered its biggest one-day pullback since 10/1/09.

As we wrote about yesterday, living up to expectation is difficult to do. The selloff in the SOX might be discounting that the stocks are already pricing in upside to current December quarter earnings season. Outside of the semis, ERTS declined 7.8% after the company's disappointing Q3 pre-announcement and decreased full-year guidance.

The range for the S&P 500 is 35 points or 1.5% (1,153) upside and 1.5% (1,118) downside. At the time of writing the major market futures are trading up slightly.

Yesterday the CRB declined 1.68% on the back of the Grains and Energy. The soft commodities Orange juice, Sugar and Coffee were the best performing on the day.

In early trading today Copper is trading near a two week low on the back of the news out of China. The Hedgeye Quant models have the following levels for COPPER – buy Trade (3.26) and Sell Trade (3.49).

Yesterday, gold declined by 1.9%, its biggest drop since 12/17/09. The Hedgeye Quant models have the following levels for GOLD – buy Trade (1,123) and Sell Trade (1,160).

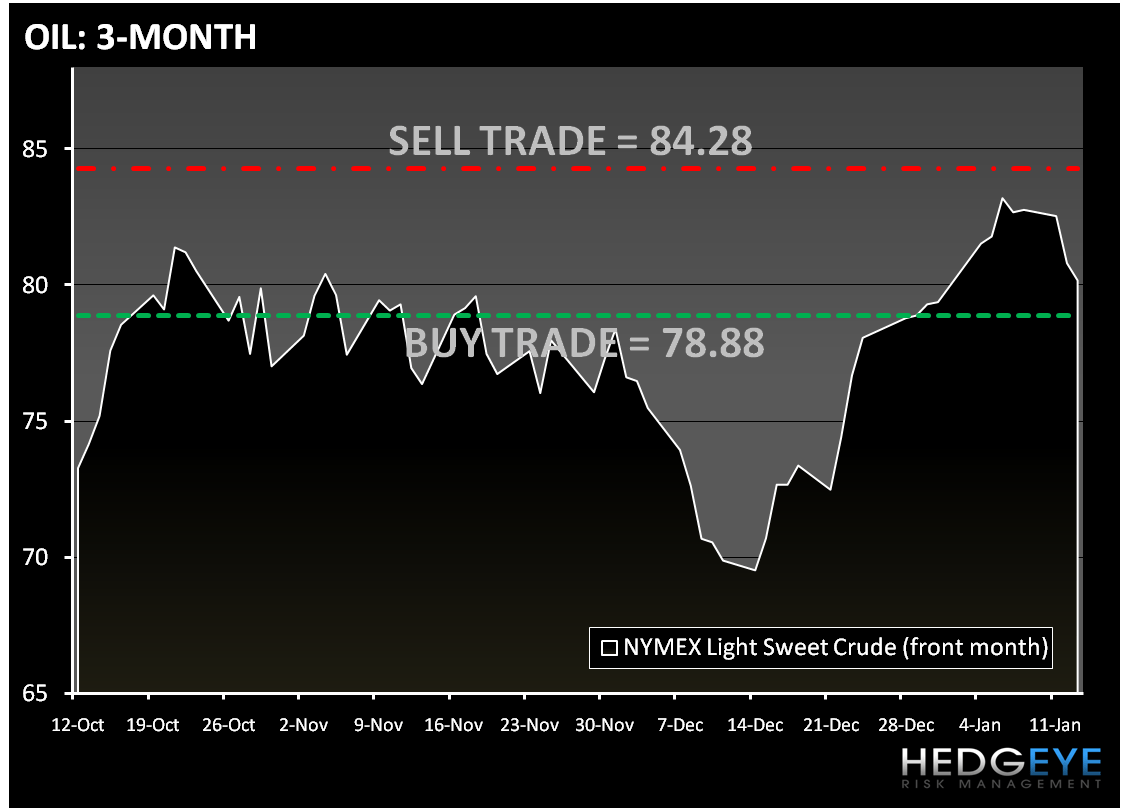

In early trading Crude oil is trading down for the third day in a row. The Hedgeye Quant models have the following levels for OIL – buy Trade (78.88) and Sell Trade (84.28).

Howard Penney

Managing Director