This special guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. Click here to get Hedgeye's Market Brief, a free weekly newsletter featuring the top 5 trending insights on Hedgeye.com.

|

“The great wheel of circulation is altogether different from the goods which are circulated by means of it. The revenue of the society consists altogether in those goods, and not in the wheel which circulates them.” –Adam Smith, 1811 |

This week in The Institutional Risk Analyst, we return to one of our favorite topics – namely credit spreads – as we consider the most recent statement from the Federal Open Market Committee. Fed Chair Janet Yellen made a presentation last week to the National Association of Business Economists illustrating that while she is puzzled by low inflation, Yellen is entirely clueless as to the workings of the financial markets.

For some time now, we have been concerned that the FOMC’s overt manipulation of credit spreads has embedded future credit losses on the balance sheets of US banks. But now we are starting to see even greater signs of stress as the large Wall Street banks again return to derivatives in order to manufacture the appearance of profitability.

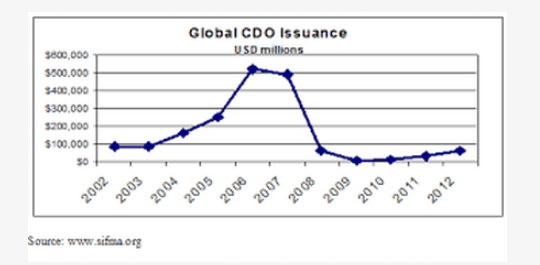

The leader of this effort is none other than Citigroup (C), which has surpassed JPMorganChase (JPM) to become the largest derivatives shop in the world. Citi has embraced the most notorious product of the roaring 2000s, the synthetic collateralized debt obligation or “CDO” security, a product that fraudulently leverages the real world and literally caused the bank to fail a decade ago.

“It’s an astonishing comeback for the roughly $70 billion market for synthetic CDOs, which rose to infamy during the crisis and then faded into obscurity after nearly destroying the financial system,” reports Bloomberg.

“But perhaps the most surprising twist is Citigroup itself. Less than a decade ago, the bank was forced into a taxpayer bailout after suffering huge losses on similar types of securities tied to mortgages. Now, many in the industry say Citigroup is responsible for over half the deals that come to market, though precise numbers are hard to come by.”

As we note in a new working paper appropriately entitled “Good Banks, Bad Banks,” large financial institutions are not particularly profitable. In times of tight credit spreads, the pressure on these banks to “cheat” when it comes to risk taking and disclosure becomes irresistible.

The dilemma large banks face when credit spreads are very low is similar to retailers that cannot compete, for example, with the efficiency of Amazon (AMZN). Low cost competitors compel other retailers to match prices, even if that forces them to lose money on each sale. Trying to “make up” the loss by increasing sale volume is the obvious path to retailer insolvency.

In banking, high spreads eventually force borrowers to default and must be cured before the economy fails. Low spreads force banks to “match or lose customers” by cutting prices. When a “matching” bank’s costs are greater than the spread borrowers pay, the correct result is to shrink the number of deals done, eventually causing spreads to rise. But that’s disastrous for bank managers. As in retail, therefore, the initial reaction of bank managers is to make up for the “low yield” on each transaction by writing more deals.

As long as government is willing to “insure” deposits of banks that speculate in this manner, it creates an obvious condition of “heads managers win” and “tails shareholders and taxpayers lose.” The most obvious use for a “synthetic CDO” is to generate a lot of fictional (“synthetic”) transactions that increase the bank’s “deal flow” without need to find actual customers that want “real” loans.

Bad banks generate a capacity to make up for the low yield on each “real” transaction by creating “synthetic” transactions. Synthetic derivatives are an obvious source for permitting fraud that necessarily harms the perpetrating bank and, ultimately, the markets as a whole.

“Bottom line,” notes our colleague Fred Feldkamp, “it is ‘impossible’ to convert ABS securities into a ‘risk free’ 20% return. As Goldman Sachs (GS) proved in 1970 with bankrupt Penn Central's commercial paper, one cannot sell bad assets to customers that you want to keep.”

Feldkamp observes that for a while now credit spreads have been too low for rational credit expansion. Banks are now forced to create and hide leverage off balance sheet (e. g. new "synthetic CDO" frauds and leveraged buyouts (LBOs) with outrageously high EBITDA ratios) in order to generate returns sufficient to pay employees when that is not available in the spreads associated with well-balanced bond sales. Again Feldkamp:

|

“When I do my spread charts, I consider the upper and lower limits to define Adam Smith's concept of a ‘Complete Market.’ Above that range of spread, there is a cushion between equilibrium and a ‘crisis zone’ because experience tells me that the ‘drag’ of high spreads can be tolerated for a while as leaders ponder what to fix. Affected firms refinance when spreads fall.” |

He continues:

|

“BELOW that equilibrium, however, I think there's only ‘irrational exuberance’ because (as Smith noted) ‘the Great Wheel of Circulation’ lacks the ‘grease’ of adequate net-interest margin (NIM) needed to keep it rolling and starts to wear out. The damage starts immediately and only the extent of the necessary ultimate repair is debatable. When banks die over dumb deals, we have no choice except to rescue depositors--thus it becomes ‘HEADS I WIN; TAILS TAXPAYERS LOSE’ at US-insured banks.” |

Feldkamp reminds us that had regulators stopped the losses generated by thrifts in the 1980s after Congress passed the ill-fated 1982 Garn-St Germain law, the cost might have been contained at a hundred billion. “By waiting seven years, however, we were just a few years away from creating a Weimar Republic collapse. Having enjoyed an eight year recovery today, the US markets are now FAR more leveraged and are therefore far more capable of a rapid descent into oblivion than 30 years ago.”

We do not need to look back 30 years, however. Synthetic CDOs were a key source for the excessive and unreported “off balance sheet” leverage at Citigroup that exploded to create the Great Financial Crisis of 2008. Starting mid-September of 2007, the Fed successfully led markets back from a “mini-crisis” that began when Bear Stearns followed the path Goldman Sachs chose decades before when Penn Central went bankrupt. Bear abandoned support for two mortgage investment funds into which it had invested customers’ money.

In mid-October, US Treasury Secretary Hank Paulson announced an intent to create a “Super SIV” (to be backed by the US government) that would “rescue” Citi from losses suffered in off balance sheet ”commercial paper conduits” that Citibank supported with standby liquidity facilities. Thankfully Hank’s ill-considered proposal never materialized. His announcement kicked off the Great Financial Crisis (that peaked thirteen months later). Within days, credit spreads for US corporate bonds leaped from “euphoric” lows to “crisis zone” highs. Credit markets required more than three years to regain spread levels observed before Paulson’s October 2007 announcement.

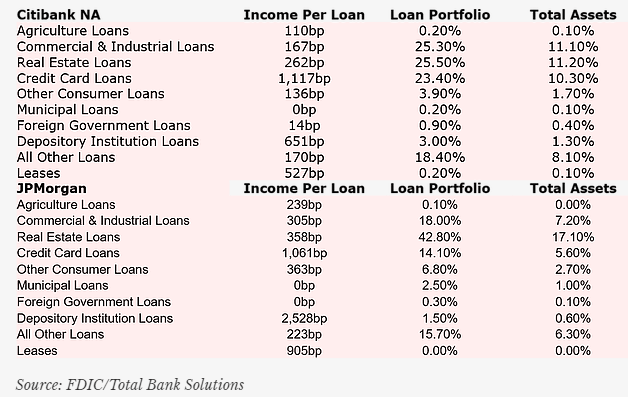

To get a sense of just how tight lending spreads are for the major banks, the tables below shows the gross loan spread, and the percentage of loans and total assets, for each loan type at Citi and JPM.

The table above illustrates the great dependence of Citi on its credit card portfolio when it comes to yield, while more that half of its loan portfolio is generating less than 3% gross yields. Citi is clearly the weaker competitor compared to JPM. And as we noted last week, Citi’s dependence on offshore institutional funding sources gives it a cost of funds almost 2x JPM and other large banks.

The moral of the story with Citi and other large banks is that there is no free lunch, but sadly no one on the FOMC seems to appreciate this subtlety. When the Fed pushes down interest rates and then manipulates credit spreads to achieve some illusory goal in terms of monetary policy, the result is a change in the behavior of investors and lenders that is profound.

The fact that Citi, JPM and GS are now pushing back into the dangerous world of off-balance sheet (OBS) derivatives just illustrates the fact that the large banks cannot survive without cheating customers, creditors and shareholders. And just as retailers cannot compete with AMZN, Citi and GS certainly cannot compete against the monopoly power of the House of Morgan.

In the case both of Citi and JPM, just half of the banks’ operating business comes from lending, while the remainder comes from risk bearing investments and trading. With some $50 trillion in off-balance sheet (OBS) derivatives, which is almost six standard deviations above the $1.8 trillion peer average for large banks, Citi and JPM are now the outliers on Wall Street in terms of derivatives exposure. A move of 30bp in the OBS derivatives book of either bank would wipe out their capital. Chart One below shows the OBS derivatives exposure of Citi, JPM, GS and the other major banks.

Notice that all three of the leading derivatives dealers have been increasing exposures since last year. Note too that the relatively small GS has a notional OBS derivatives book of more than $41 trillion, almost as large as that of Citi and JPM. More alarming, a move of just 7bp in the smaller bank’s OBS derivatives exposures would wipe out the capital of Goldman’s subsidiary bank. This gives GS an effective leverage ratio vs its notional OBS derivatives exposures of 8,800 to 1. And all three banks are clearly outliers compared to the rest of the large US banks, which generally eschew OBS derivatives as the tiny peer average suggests.

So ask not whether President Donald Trump should reappoint Janet Yellen to another term as Fed Chair. Rather, ask yourself why Yellen wants to stick around Washington at all given the accumulation of risk inside the major US banks as a result of the FOMC’s manipulation of credit spreads. The combination of a lack of profitability and a huge derivatives book makes another financial collapse increasingly likely despite the apparent solidity of the US banking system.

As with the S&Ls in the 1980s, Yellen and other regulators have an opportunity to throttle-back risk taking by Citi, JPM and GS now and avoid a calamity. But Buy Side investors would never tolerate such a move by regulators. As we note in "Good Banks, Bad Banks," larger institutions suffer from a fatal lack of profitability that ultimately dooms them to commit fraud and, eventually, suffer a catastrophic systemic risk event. As Fred Feldkamp never tires of reminding us: "The only thing worse than “excessive” leverage is 'excessive off balance sheet' leverage."

EDITOR'S NOTE

This Hedgeye Guest Contributor piece was written by Christopher Whalen, author of the new book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. This piece does not necessarily reflect the opinion of Hedgeye.