|

SUMMARY. This week, tax writers, known around Washington as 'The Big Six' – National Economic Council Director Gary Cohn, Treasury Secretary Steve Mnuchin, Senate Majority Leader Mitch McConnell, Senate Finance Committee Chairman Orrin Hatch, House Speaker Paul Ryan and House Ways and Means Committee Chairman Kevin Brady – will release the contours of their tax reform plan. President Trump plans to announce, as part of that agreement, that he will see reductions of the corporate income tax rate from 35 to 20 percent and the individual rate from 39.6 to 35 percent. The top tax rate for sole proprietorships and other pass-through entities that are the common legal structure for small businesses would be reduced from 39.6 to 25 percent - with conditions. |

This week’s announcement will serve to jump-start negotiations between the various factions in the Republican conferences on both sides of the Hill. The goal is to deliver a tax reform package to the president by Dec. 31, 2017. We doubt they will meet that timeline; Q1 2018 is a more likely target.

LAY OF THE LAND. It is easy to get cynical after the Congress’ botched efforts to do something, anything with the Affordable Care Act. However, it is important to remember that, unlike health care, Congressional Republicans have deep policy expertise on taxes and the role they play in the economy. President Trump, who never really cared much for the minutiae of health care policy, sees tax reform as critical to his agenda.

This week, Republicans will kick-off what is likely to be six months of negotiating and legislating to get a package to the president’s desk. During that time, fiscal hawks and establishment Republicans will play what amounts to a high-stakes game of whack-a-mole with the overarching priorities of stimulating economic growth and limiting tax base erosion without increasing the federal deficit.

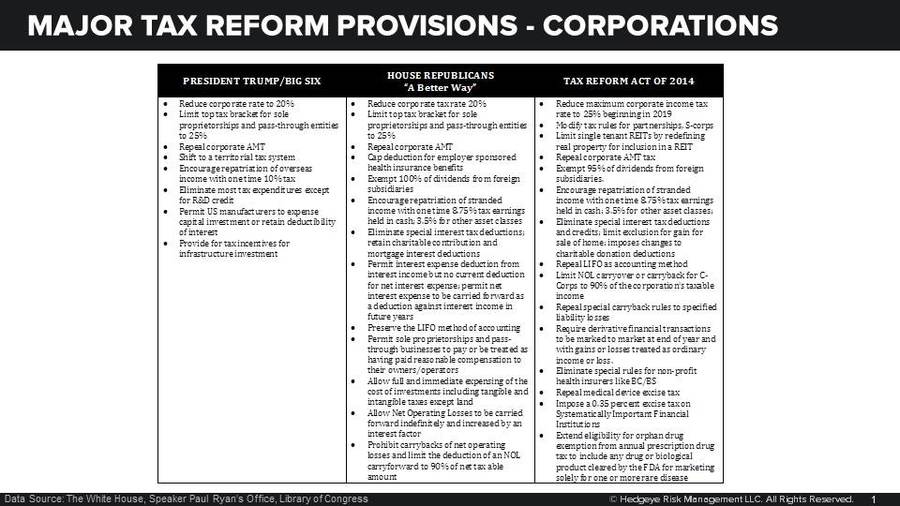

Policy makers will have a Chinese menu of sorts on which they can rely. Retiring Rep. Dave Camp (R-MI) filed the Tax Reform Act of 2014 before leaving Congress and as a way to establish Republican aspirations on the issue. In the summer of 2016, House Republicans produced a policy platform known as “A Better Way” that dedicated substantial column inches to tax reform. Finally, the Big Six – Cohn, Mnuchin, McConnell, Hatch, Ryan and Brady – have articulated some broad goals and are expected to announce their plan this week.

Knowing what the possibilities are is important. Chairman Hatch has insisted that the Big Six’s plan will only serve as an outline (read: don’t tell us what to do.) Since there is nothing new under the sun, tax writers will inevitably reach back to earlier proposals as they develop a legislative package.

The chart below provides side-by-side comparisons of recent proposals whose provisions are likely to be under consideration:

Download .pdf version of both charts here.

In comparing these three vehicles for policy expression, a few themes emerge:

Lower rates. There appears to be broad agreement that tax rates and especially corporate tax rates need to be reduced. The top individual rate would move from 39.6 percent to 35 percent. The corporate tax rate would be reduced from the current level of 35 percent to 20 or 25 percent. President Trump has previously expressed support for 15 percent corporate tax rate and his bias should exert some downward pressure in negotiations.

While the top marginal rate for individuals and corporations will get the most play in the media, we anticipate there will be an effort to make other changes like repeal of the corporate and individual Alternative Minimum Tax.

Simplify the Code. Walking hand-in-hand with reducing the tax rates is an effort to simplify the code by reducing the number of brackets and eliminating a plethora of credits and deductions, we anticipate that the Trump Administration will propose three brackets instead of seven under current law for individual filers. The president’s proposal has the support of Republicans who have advocated for that change for years.

The final rates will be the subject of much negotiation. Trump is expected to propose rates of 10, 25 and 35 percent with a 100 percent increase in the standard deduction to $24,000 (joint filers). Other Republican proposals have advocated for reducing the basic deductions for individuals from five to two. The two surviving deductions – standard and child credit – would be increased.

Also under consideration is elimination of a number, if not most, of the tax credits and deductions that populate the corporate and individual codes. The beauty of eliminating deductions and credits, so-called “tax expenditures,” is that they can serve as off-sets of “pay-fors” for reducing marginal tax rates.

The single largest tax expenditure is for health insurance benefits offered by employers. Repeal of this provision has earned the objection of the U.S. Chamber of Commerce and other business groups. However, we suspect that there is a deal to be had between the corporate tax rate and some cap or other limits on the deductibility of health insurance for employees.

Notwithstanding the alarm bells the housing industry rang earlier in the year, the mortgage interest deduction is probably not under threat. We do see a scenario where this sacred cow of tax expenditures is limited. The Tax Reform Act of 2014, for example, proposed to reduce the limitation of indebtedness from $1 million to $500,000 and eliminate the deductibility of home equity loans.

The top 15 tax expenditures and their value as off-sets are listed in chart below

The Trump Administration and Congressional Republicans also seem keen to retain the Research and Development Tax credit which was made permanent in 2015. Other, more obscure credits and deductions are most assuredly on the endangered list. The Tax Reform Act of 2014 included repeal of a number business credits and deductions and thus serves as a good roadmap for what this Congress might consider. A complete list of deductions and credits targeted for elimination in the Tax Reform Act of 2014 can be found here.

Correct Tax Base Erosion. Simplifying the code would serve to restore the tax base lost to special interest deductions and credits. Republicans also hope to correct the significant corporate tax base erosion created by the high U.S. corporate tax rate. According to the Joint Committee on Taxation, the U.S. has the highest corporate tax rate of any developed nation.

In lowering the corporate tax rate, Trump and Congressional Republicans hope to encourage American companies with significant overseas income to repatriate stranded income. To provide some incentive for the estimated $2.4 trillion to return to U.S. parent companies, Trump and Republicans are set to propose a one-time tax on those foreign assets. Trump, ever the nationalist, hopes to assess a 10 percent tax while Congressional Republican proposals are more constrained – 8.75 percent for cash assets and 3.5 percent for income held in other asset classes. On a go forward basis, Republicans hope to exempt from taxation 100 percent of dividends paid by foreign subsidiaries of U.S. corporations.

There is speculation that as Republican members of the Ways and Means Committee wrap up day two of their retreat with Chairman Brady and Speaker Ryans that the following provisions are under consideration in addition to all the aforementioned:

- Preserve Section 179 on expensing depreciation

- Eliminate state and local tax exemption

- Repeal federal estate tax

- Cap net interest deduction at 30 percent of EBITDA

Furthermore, Sen. Orrin Hatch has let it be known that he plans to include his Corporate Integration Plan into comprehensive tax reform. His yet unreleased plan would call for an end to double taxation of corporate income by establishing a corporate deduction for dividends.

WHAT IS NEXT? We are not optimistic that Congressional Republicans can meet a Dec. 31, 2017 deadline for delivering tax reform to the president’s desk. We believe a more realistic target is Q1 2018.

The legislative vehicle Congressional Republicans plan to use to accomplish tax reform is budget reconciliation. Senate rules governing budget reconciliation mean only a simple majority is required for passage. Before tax reform can be approved via reconciliation, Republicans must pass a budget resolution that contains instructions to the tax-writing committees. The committees then reconcile the current budget with the proposed budget by writing a tax reform package that conforms with those instructions.

Simple enough? Not exactly.

House Republicans, particularly ultraconservative Freedom Caucus members, want to ensure tax reform is fully offset by reductions elsewhere. The House Republican Plan known as “A Better Way” contained an estimated $8 trillion in revenue reductions including the aforementioned rate reductions. About half of that amount can be recovered by eliminating deductions and credits and disallowing the interest deduction. Speaker Ryan and other members of leadership had hoped to close the gap with $1 trillion each generated from a border adjustment tax and repeal of the ACA with the balanced resolved through dynamic scoring.

The White House shot down the border adjustment tax and the ACA has not been repealed. No amount of dynamic scoring can close a $4 trillion gap no matter how creative one gets.

Freedom Caucus members are going to insist that the gap is closed through spending reductions elsewhere. Meanwhile, the White House and more centrist Republicans are willing to ignore the shortfall and cause an increase in the projected federal deficit in the name of an important legislative win. That conflict makes fiscal hawks unwilling to trust leadership will deliver a fully offset tax reform package. So, negotiations drag on over the budget resolutions instructions.

Our best guess for a timeline is:

As we move through the process, we will be analyzing the effect of various proposals on related sectors.

Emily Evans

Managing Director

Health Policy

@HedgeyeEEvans