Our proprietary December property data indicate very strong results for Wynn Macau. Numbers should go higher.

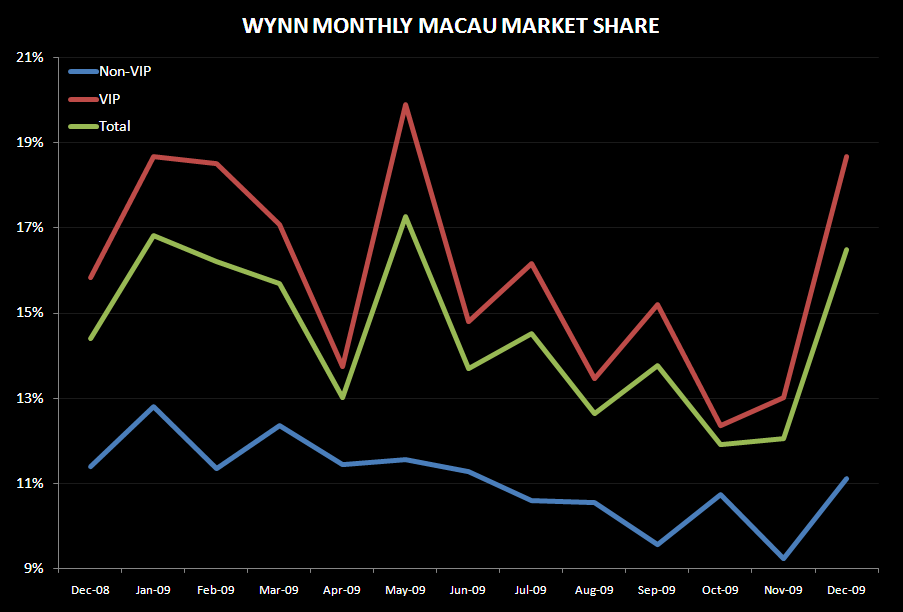

Total Macau table gaming revenue increased 44%, 63%, and 49% in the Q4 months of October, November, and December, respectively. As we wrote about yesterday, Wynn Macau was a clear standout in December, more than reversing year-over-year market share declines in previous months. Market share was up in both VIP and Mass and it wasn’t significantly impacted by hold percentage. One month a trend does not make but this is encouraging. The following chart shows Wynn’s monthly market share in Macau.

On a year-over-year basis, Wynn Macau generated a 71% increase in table revenue, up 85% and 29% in the VIP and Mass segments, respectively. For Q4, table revenues at the property climbed 34%, much better than we had projected. The following chart details the monthly y-o-y change in Wynn Macau’s VIP, Mass, and total table revenues.

So what does this do to our numbers? Not surprisingly, they go up! We are now projecting company EBITDA of $197 million versus the Street at $183 million. For Wynn Macau, we estimate EBITDA of $145 million ($117 million after corporate allocations and royalty fees).

I’m still bullish on Macau over the near-term but I’m growing more cautious particularly since our macro and international guru, Keith McCullough, is getting negative on the sequential China economic trends. Those trends matter when it comes to the VIP business, which may be in a bubble. The supply situation must be also monitored given the 20%+ Mass table game supply increases for much of this year. It’s tough to call a top on the Macau names so incorporating a momentum and catalyst driven approach on these stocks is probably appropriate. Valuation seems to matter less.