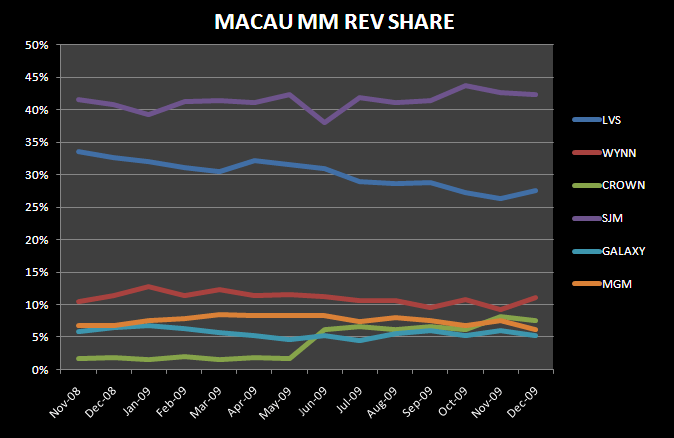

We’ve got the property detail for Macau for the month of the December. The whole market performed well - up 49% - but Wynn Macau blew the doors out.

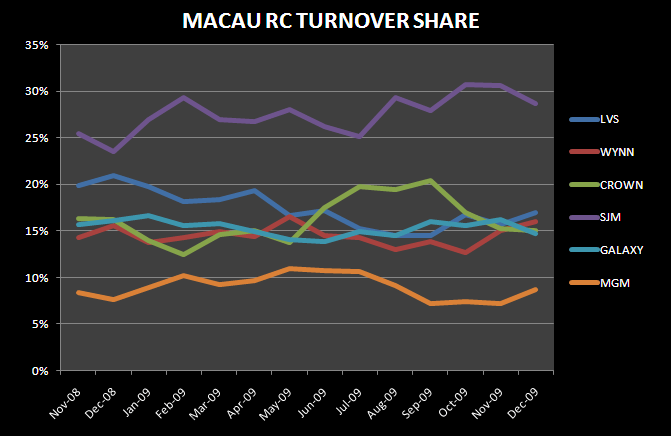

Total table revenue increased 49% in December with VIP up 57% and Mass up 33%. VIP hold percentage was consistent with the average for the year. Wynn Macau expanded its market share driven primarily by a 570 bp sequential improvement in VIP share and a 190 bp improvement in Mass. Crown, Galaxy, and MGM gave up share from November. On a y-o-y basis, Galaxy, MGM, and Wynn were the big winners. Here are the property/company commentary with market share charts below.

Sands Macau

Sands was one of two major properties that experienced a y-o-y decline in table revenues, down 4% in December. The opening of SJM's Oceanus next door in mid December 2009 probably impacted the casino. Sands' market share dropped 50 bps sequentially in December and 390 bps y-o-y. VIP hold % looked normal. We continue to believe analysts may be too aggressive in projecting EBITDA growth at the property next year given the Oceanus presence.

Venetian Macau

Market share increased slightly from November to 12.0% in December, still well below the 16.6% achieved in December 2008. The Venetian did generate 8% y-o-y revenue growth with Mass revenue up 18%. On a relative basis, Venetian’s VIP business remains weak (in part intentional) as revenue increased only 8% despite a high hold percentage.

Wynn Macau

Wow - what a month. Wynn Macau generated a whopping 71% increase in table revenue. Hold was a little above normal but VIP rolling chip still increased 71%. Market share climbed 450 bps to 16.5%, and even better than the 14.4% experienced in December 2008. As discussed above, market share gains came in both VIP and Mass. Most of the y-o-y gain was derived in the VIP segment, but a 29% increase in the high margin Mass business is not too shabby.

MPEL

The good news is that Crown’s market share increased slightly y-o-y in December. The bad news is that it was the lowest share since City of Dreams opened in June. While 50 bps off the November record, CoD’s Mass market share was the second highest of its short history. CoD did hold below normal in the VIP segment. Altira had another tough month with total table revenue down 37% and hold percentage was also below normal.

MGM

MGM grew revenues 81%, primarily by more than doubling VIP revenues. The comparison was very easy. Indeed, December market share of 6.4% actually declined from 9.3% in November and was the property’s lowest share since February. Mass share declined 140 bps to 6.2%.

SJM

Despite the opening of Oceanus mid-month, SJM experienced a sequential decline in market share of 120 bps to 31.9%. Oceanus, a Mass oriented property, didn’t impact SJM’s Mass share which stayed relatively flat. On a y-o-y basis, however, SJM continues to garner a higher share as evidenced by the company’s 58% total table revenue growth versus the market at 49%.

Galaxy

December was a nice month for the Galaxy properties as market share continues to accelerate in recent months. In total, Galaxy generated an 83% increase in table revenues, almost exclusively from VIP. The Galaxy properties benefited from higher-than-normal table hold percentage in December. VIP chips were still up 62%.