FL: Close ‘Em or Suffer

Our team has roughly 30-years of cumulative experience analyzing this beast. Throughout our tenure, what we have not seen is a respectable analysis showing cannibalization factors by FL concept. Well… here you go. We still like the low-hanging fruit here.

Here’s an update on Foot Locker – one of our top bench ideas for 2010. Our team has roughly 30-years of cumulative experience analyzing the beast that has become Foot Locker. Throughout our tenure, what we have not seen is a respectable overlap analysis showing likely cannibalization factors by FL concept. Well… here you go.

The bottom line is that the overlap stats are quite sad, actually.

Here’s the analysis:

There are 111 stores or 5.4% of the domestic FL portfolio that suggest self cannibalization. In other words, 111 units are located within a ½ mile or less of another unit with the exact same nameplate. Think Foot Locker in a mall and another at the other end of the mall or just down the street.

Source: ESRI; InfoUSA; Research Edge. Note: InfoUSA database represents 90% of the total U.S. store base. Data not available for Champs.

The overlapping stores listed above represent the most obvious candidacy for closure. Provided the upfront lease termination fees are justifiable, it seems reasonable to assume a productivity boost would result from closing stores that are in close proximity to other locations carrying the same brand name. As a sidenote, FL’s implied portfolio lease duration is among the lowest in retail. It has not done a whole lot right in its history, but keeping landlords on a short leash has been an area of strength. High lease flexibility is definitely a big positive.

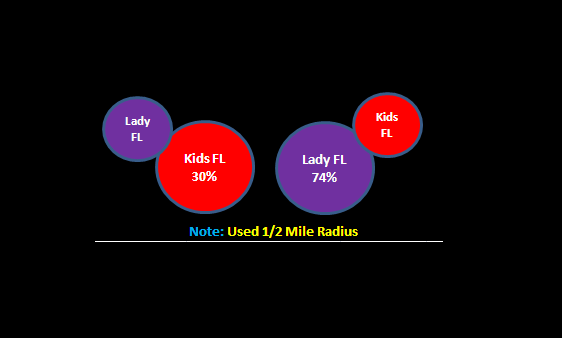

After eliminating some of the more obvious locations, store closures become more strategic. Our analysis suggests that FL’s domestic store portfolio is 81% self-cannibalizing. In other words, 81% of all Foot Locker sub-brands have another sub-brand within a ½ mile. However, we caution not to get overly fixated on this high number. The majority of the concentration comes from Lady Foot Locker and Kids Foot Locker, both of which were clearly positioned with co-location in mind. This brings us to our next step in store closures: Lady Foot Lockers.

Source: ESRI; InfoUSA; Research Edge

Source: ESRI; InfoUSA; Research Edge

Over time, management established Foot Locker stores as a central hub and then added additional locations in the same mall with the opening of Lady Foot Lockers and Kids Foot Lockers. It seemed logical to place Lady Foot Lockers next to or near Kid’s Foot Lockers because they do not compete, but instead complement each other. That makes sense to us at some level, but with 1.7 Lady Foot Lockers for every Kids Foot Locker, the opportunity to right-size the Lady portfolio appears compelling. In fact, we wonder why Lady and Kids need to separately exist? A one stop shop for women and children, while leveraging overhead. After all, ‘kids’ is not a gender. Kids also could care less where their Mom buys their kicks. Stores should cater to the person holding the cash – not the 4-year old that cannot dress himself in the morning.

We’re still awaiting signs of management’s actual intentions, but for now we’ll continue to explore all options and ideas. We continue to believe there is ample low hanging fruit here, and real estate may just be the easiest to pick given a 20 point+ margin delta in profitability between the best and worst performing stores.

Zachary Brown

Eric Levine