After a melt-up day on Monday the S&P 500 finished up 0.31% in fairly light trading on Tuesday. There was no dominating theme running thru the market yesterday. From a MACRO view the market has seemed to discount the heightened global economic recovery theme that fueled Monday’s rally.

Tuesday’s MACRO data points were not as convincing as Monday’s and in some cases were downright bearish. After rising for 10 consecutive months, pending home sales declined 16% month-to-month in November vs. expectations for a 2% decline. While the number was explained away as an anomaly as the early November extension of the first-time homebuyer tax credit was not in place to provide any meaningful support.

Also on the MACRO calendar, factory orders rose 1.1% in November, above consensus estimates for a 0.5% increase. While durable orders were unrevised at up 0.2%, core capital goods orders were revised up to 3.6% from 2.9% in the advance report. In addition, core capital goods shipments were revised up to 1.1% from 0.8%; orders for non-durable goods rose 1.8% in November, the fourth consecutive increase. Inventories rose 0.2% in November following a 0.6% gain in October.

After the close the ABC consumer confidence reading came in at -41 versus last week’s reading of -44. The index has not seen a reading of better that -41 in nearly two years.

While the MACRO calendar was mixed, the sectors levered to the RECOVERY trade were the outperformers. Defensive sectors were among the worst performers, with the Utilities being the worst performing sector for the second day in a row. The underperformance of the Utilities is consistent with our “Rate Run-up” theme for 1Q10.

Yesterday, the Financials was the best performing sector on the day. Life insurers and Bank stocks were another bright spot with the BKX +2.24% and now up 4.51% over the past two days. Within the XLF, COF was up +3.9% (A Research Edge top pick) and C +3.8%, BAC +3.3% and WFC +2.8% also outperformed. MS is now up 8.09% in the first two trading day of the year.

After underperforming on Monday, Consumer Discretionary was the third best performing sector yesterday. Consensus is building that December same-store sales are going to be stronger than expected and some key sell-side upgrades helped the retailers outperform.

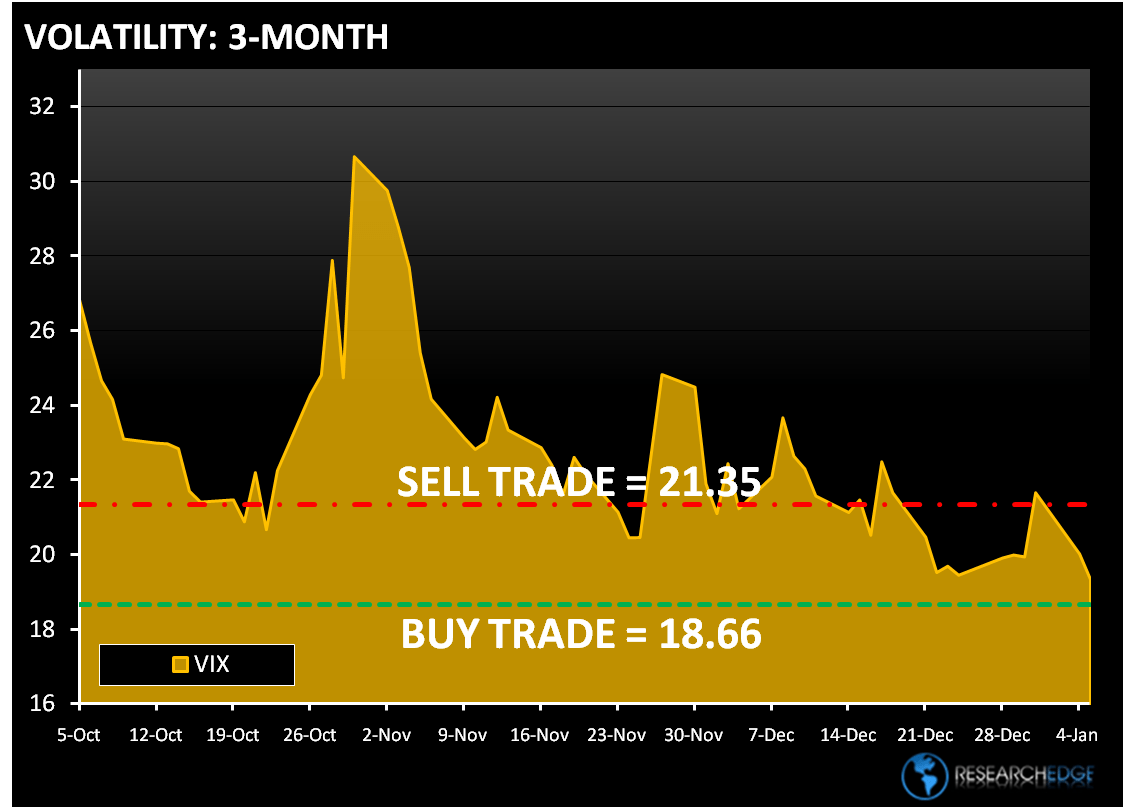

The range for the S&P 500 is 12 points or 0.25% upside to 1,385 and 1.0% downside to 1,125. At the time of writing the major market futures are trading lower on the day.

Copper rose O.22% yesterday and is trading up 1.77% in early trading today. Copper is trading higher for the fifth straight day on speculation that demand will improve as the U.S. economy continues to show strength. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.31) and Sell Trade (3.47).

GOLD trade up yesterday by 0.33%, but the dip mentality prevails. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,084) and Sell Trade (1,137).

Crude oil traded up 0.32% yesterday to 81.77 - a 14-month high – as cold weather in the U.S. and signs of economic recovery are helping demand. The Research Edge Quant models have the following levels for OIL – buy Trade (78.74) and Sell Trade (83.04).

Howard Penney

Managing Director